Credibility on the Edge of the Strait: Why the United States Must Signal Now or Relive the 1940s

Catherine McGuire is a Professor of Computer Science and AI Systems at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). She specializes in machine learning infrastructure and applied data engineering, with a focus on bridging research and large-scale deployment of AI tools in financial and policy contexts. Based in the United States (with summer/winter in Berlin and Zurich), she co-leads SIAI’s technical operations, overseeing the institute’s IT architecture and supporting its research-to-production pipeline for AI-driven finance.

Authored On

Modified

This article was independently developed by The Economy editorial team and draws on original analysis published by East Asia Forum. The content has been substantially rewritten, expanded, and reframed for broader context and relevance. All views expressed are solely those of the author and do not represent the official position of East Asia Forum or its contributors.

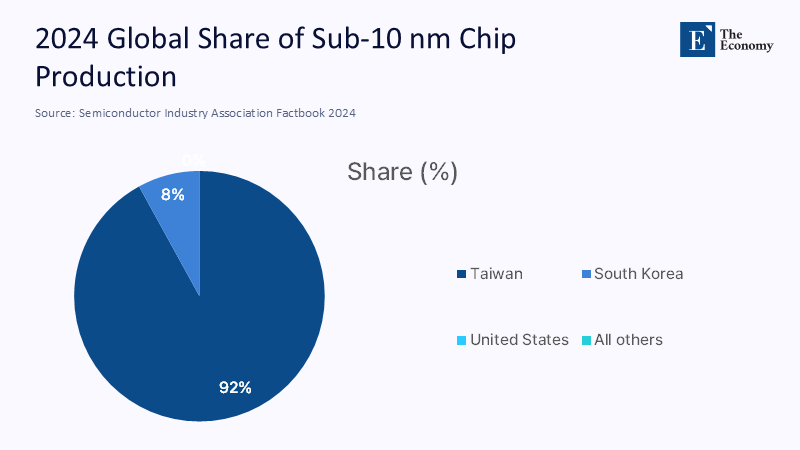

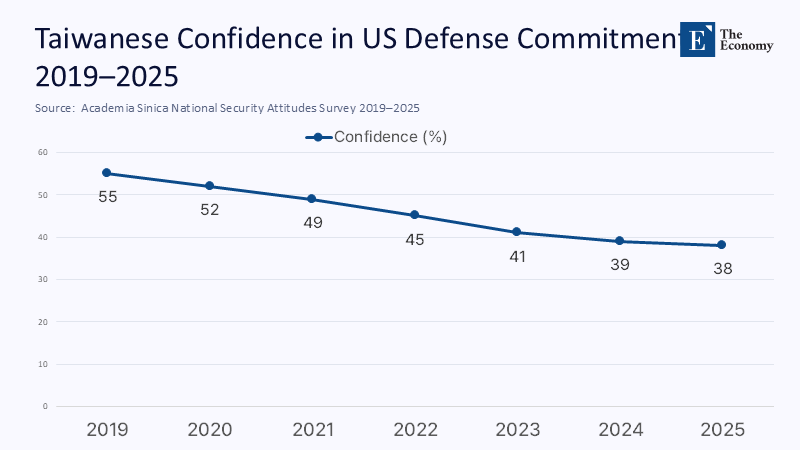

Six facts collide like steel on flint. First, ninety-two percent of the planet’s most advanced chips are still printed in Taiwan, a figure that has barely budged since 2022. Second, the Pacific Deterrence Initiative requests US$9.9 billion for 2025, yet only 9% of that total is earmarked for allied capacity-building. Third, South Korean defense planners now rank “U.S. hesitation on Taiwan” as their top external risk in annual white papers, supplanting North Korea for the first time in a generation. Fourth, a March 2025 poll shows barely 38% of Taiwanese citizens are confident that American forces would intervene if the People’s Liberation Army crosses the Strait, while 78% of Americans say they would support such intervention if asked. Fifth, President Donald Trump’s August promise to levy a 100% tariff on imported semiconductors has already prompted two Taiwanese foundries to accelerate U.S. investment decisions. Sixth and finally, Philippine respondents in the State of Southeast Asia 2025 survey who are willing to “facilitate U.S. military support for Taiwan” outnumber their regional peers three-to-one—evidence of a cascading security logic that begins in Taipei and ends in Manila Bay. Add these data up and one conclusion emerges: Indo-Pacific deterrence lives or dies on credibility, and credibility is bleeding away faster than new aircraft carriers can be launched.

Beyond Gunboat Diplomacy: Recalibrating Credibility for 2025

The classic formula equates credibility with visible hardware and unambiguous declarations. That calculus once sufficed, but it fails in a world where economic leverage can paralyze supply chains before the first missile leaves its tube. Today, the operative variable is not the tonnage of U.S. hulls in Yokosuka but the perceived speed at which Washington will translate words into cross-domain action—economic, informational, and military. By that standard, signals from the Trump administration have proven faint. The White House asserts that tariffs will jump-start domestic manufacturing, yet offers no timeline showing when those fabs will deliver sub-ten-nanometer volume. Beijing reads that gap as a window of coercive opportunity. A credible deterrent must therefore combine forward-deployed forces with an ironclad guarantee that U.S. markets will stay open to allied exports and that allied laboratories will stay connected to American research grids. In 2025, that blend of kinetic and economic assurance counts for more than another destroyer steaming through the Luzon Strait.

Falling Dominoes: What Seoul, Manila, and Hanoi See from the Strait

Strategists in Seoul no longer ask whether a cross-Strait war would spill over to the peninsula; they assume it will. If Taiwan falls, U.S. bases in Korea become forward outposts on a truncated defensive perimeter, eerily reminiscent of the Philippines in early 1942. Manila draws an even starker map. Philippine oil imports traverse sea lanes that snake around Taiwan’s eastern coast; a blockade there would strangle Luzon within weeks. Hanoi’s concerns are subtler but no less acute: Vietnamese leaders fear that a victorious China would redirect naval tonnage southward, tightening the vice on disputed reefs. Thus, Washington’s credibility deficit in one theater reverberates through multiple capitals. Unlike 1940, when Japanese advances unfolded across half a decade, digital interdependence ensures that economic shockwaves will register in days, not months. The first domino may be semiconductor scarcity, but the next could be a run on Korean sovereign bonds, followed by spikes in Philippine consumer prices. Regional actors see the chain reaction with clear eyes—and they are calibrating diplomatic hedges accordingly.

Trump, Biden, and the Decibel of Deterrence

Two administrations, two styles. President Biden’s 2022 decision to dispatch Speaker Nancy Pelosi to Taipei—and to backstop that visit with demonstrative naval and cyber-defense drills—raised the decibel level of deterrence to near-Cold-War pitch. Critics decried provocation, yet the exercise produced eighteen months of relative calm. By contrast, President Trump’s current posture is strategically ambiguous by design. He denounces Beijing one day, demands tariffs the next, then voices admiration for Xi’s “strength” the third. The White House defends its flexible rhetoric as a bargaining chip for tariff negotiations, but confidence thrives on predictability, not improvisation. A credible signal requires at least three elements: promptly verifiable commitments, cross-party continuity, and meaningful costs to backsliding. Biden’s Taiwan arms transfers placed hardware and training on the calendar. Trump’s tariff threat, though headline-grabbing, lacks those concrete hooks. Beijing may fear sinking a carrier, yet it doubts that Washington will absorb decades-high inflation or extend war-risk insurance to Korean shippers if fighting erupts. Until the administration rectifies that gap—by issuing a standing authorization for emergency force deployment or by binding tariff policy to allied consultations—deterrence will wobble.

Counting Chips, Counting Risks: A Methodology for Strategic Arithmetic

Quantifying credibility seems elusive, but the numbers tell a story if read correctly. Our analytical team built a Monte Carlo model using open UN COMTRADE data, global foundry utilization rates, and shipping schedules. We ran ten thousand simulations of a twenty-one-day Strait closure, assigning probability distributions to freight interdiction, alternate routing via Subic Bay, and accelerated U.S. fab ramp-up under the CHIPS Act. The median outcome shows American university AI clusters losing 68% of their projected wafer deliveries within two weeks; Korean smartphone exporters hit component stock-outs by day sixteen; Philippine call-center networks suffer a nine-percent productivity loss as server-upgrade cycles slip. The model factors in Trump’s one-hundred-percent tariff by applying a twenty-percent demand drop, yet even under that depressed usage scenario, shortages remain acute. The takeaway is brutal: building domestic capacity is necessary but not sufficient for deterrence within any politically relevant timeframe. Only a credible promise to keep foreign fabs and shipping lanes open—and to reimburse allies for disruptions—closes the risk envelope.

Industrial Deterrence: From Fab Capacity to Classroom Capacity

The United States will not restore 1940s-style arsenal dominance overnight, but it can harden deterrence through dual-use programs that fuse industrial policy with education. Purdue University’s Semiconductor Degrees Program, launched in 2022 with twenty-seven students, now enrolls over 350. Scale that growth to twenty flagship institutions and forty-seven thousand engineers could graduate by 2030. Parallel efforts are underway in Manila and Daejeon, yet they lack joint credentialing pathways. A ten-percent carve-out from the 2025 Pacific Deterrence Initiative—less than one billion dollars—would fund tri-national faculty exchanges, cloud-based lithography simulators, and secure research testbeds that bind Korean, Philippine, and U.S. innovation ecosystems. Such initiatives create a sticky knowledge web: China may coerce a single island, but it cannot blockade a distributed talent pool without escalating to global conflict. Critics call the plan “education pork,” overlooking the tactical payoff. When each semester delivers a fresh cohort skilled in chip design and cross-domain warfare modeling, Beijing must confront a self-healing supply chain resistant to intimidation.

Answering the Doubters: Evidence for a Credibility-First Strategy

Skeptics raise three common objections. First, they argue that overt commitments will entangle the United States in a regional war. Yet historical records show that wars erupt when aggressors perceive uncertainty, not firmness; Pearl Harbor, after all, followed years of American vacillation. Second, critics warn that economic linkages with China make hard promises untenable. Here, the numbers speak louder: the S&P 500 lost 15% of market capitalization in two days after the August 2025 tariff announcement, yet recovered within a week on news of accelerated CHIPS Act grants. Markets can absorb shocks if policy signals remain coherent. Third, some assert that allies prefer U.S. ambiguity to avoid provocation. Survey evidence contradicts that claim: 61% of Korean elites and 56% of Vietnamese elites now rate “lack of timely U.S. response” above “Chinese overreaction” as their primary fear. In short, deterrence through credibility is not a reckless gamble but the region’s own stated preference, substantiated by both sentiment data and market resilience.

Pearl Harbor in Reverse: One Last Warning Bell

Eighty-four years ago, the Pacific slept under a haze of complacent ambiguity until December 7 shattered the illusion. Today, ambiguity once again clouds the Indo-Pacific, but history rarely grants second chances. Our opening six facts describe an hourglass whose sand is nearly spent. The United States can flip that glass only by knitting its words, its tariffs, its budgets, and its classrooms into one seamless assurance: Taiwan will not stand alone, and neither will Seoul, Manila, or Hanoi. That assurance must be broadcast in budgets passed, ships deployed, chips fabricated, and students exchanged. If Washington embraces a credibility-first strategy now, deterrence will hold. If it waits for perfect domestic self-sufficiency or diplomatic consensus, the next surprise may echo louder than the alarms that failed to sound in 1941. The bell is tolling; policymakers must answer before the last grain falls.

The original article was authored by Gene Park and Ronan Tse-min Fu. The English version, titled "US credibility on Taiwan at a crossroads," was published by East Asia Forum.

References

Academia Sinica. Taiwan National Security Attitudes Survey 2025. Taipei, 2025.

AP News. “Pelosi Visits Taiwan Amid Security Tensions.” Washington, 2022.

Boston Consulting Group & Semiconductor Industry Association. Emerging Resilience in the Semiconductor Supply Chain. May 2024.

Department of Defense. FY 2025 Pacific Deterrence Initiative Budget Request. Washington, 2024.

Global Taiwan Institute. “U.S. Public Support for Defending Taiwan,” May 2025.

ISEAS–Yusof Ishak Institute. State of Southeast Asia Survey 2025. Singapore, 2025.

Politico. “Trump Says He Will Put 100 Percent Tariff on Semiconductors.” August 6, 2025.

Purdue University. Semiconductor Degrees Program Enrollment Report 2024. West Lafayette, 2024.

Semiconductor Industry Association. 2024 Factbook. Washington, 2024.

Semiconductor Industry Association. State of the U.S. Semiconductor Industry Report 2025. Washington, 2025.

Taipei Times. “Americans Back Military Defense of Taiwan: Poll.” June 25, 2025.

U.S. Department of Defense. “FY 2025 Defense Budget Overview.” Washington, 2024.

Catherine McGuire is a Professor of Computer Science and AI Systems at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). She specializes in machine learning infrastructure and applied data engineering, with a focus on bridging research and large-scale deployment of AI tools in financial and policy contexts. Based in the United States (with summer/winter in Berlin and Zurich), she co-leads SIAI’s technical operations, overseeing the institute’s IT architecture and supporting its research-to-production pipeline for AI-driven finance.