China’s Standardized, Low-Cost Nuclear Power Push Signals Potential Upheaval in the Global Market as It Nears World’s Largest Nuclear Fleet

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Authored On

Modified

China accelerates expansion of nuclear generating capacity under a state-led strategy Standardization strengthens infrastructure capabilities while delivering significant cost advantages Rapidly expanding nuclear market could reshape the standing of traditional leaders including the United States, France, and Switzerland

Analysts project that China could become the world’s largest nuclear power producer within the next several years. A state-driven capacity expansion strategy, standardized reactor construction systems, and strong cost efficiency are increasingly viewed as key factors underpinning Beijing’s growing market position. As traditional nuclear leaders such as the United States struggle with supply-chain disruptions and soaring costs, China’s advance is expected to emerge as a pivotal force reshaping the broader nuclear industry.

Rapid Expansion of China’s Nuclear Ecosystem

According to a report published on June 9 by the South China Morning Post (SCMP), citing the latest energy security report from global macroeconomic and technology research firm Gavekal Dragonomics, the clean-energy landscape in both the United States and China is expected to undergo dramatic changes within the next five years. Damien Ma, Managing Director and Head of New Energy Research at Gavekal Dragonomics, stated in the report that “China currently accounts for nearly half of all new reactors under construction worldwide,” adding that “by 2035, China will possess the world’s most dynamic and powerful nuclear industry value chain.”

The forecast is widely attributed to the Chinese government’s strong commitment to expanding nuclear power. Beijing has designated nuclear energy as a top solution for meeting rapidly rising industrial electricity demand while building a stable low-carbon energy network. A notable example was the inclusion of nuclear technology in the “Made in China 2025” initiative, under which localization and export promotion across reactor design, construction, and operation were elevated to national priorities. Following the 2011 Fukushima nuclear disaster in Japan, approvals for new nuclear projects were temporarily suspended amid heightened safety concerns. However, construction activity accelerated again after regulatory reforms were completed in 2019.

Nuclear power also features prominently in China’s long-term national planning framework. The 15th Five-Year Plan covering 2026–2030 identifies nuclear energy as a core power source for achieving energy security and carbon-neutrality objectives. Beijing has pledged to expand nuclear generation in a safe and orderly manner while positioning it, alongside wind, solar, and hydropower, as a central pillar of a low-carbon electricity system. The government has also designated next-generation reactor technologies, nuclear fuel-cycle development, and fusion research as strategic priorities, while targeting 110 gigawatts (GW) of installed nuclear capacity by 2030.

Dominance in Construction Speed, Scale, and Efficiency

China’s practical competitiveness in the nuclear sector continues to strengthen. The country has pursued a strategy of simplifying and standardizing reactor designs around models such as Hualong One, CAP1000, and CAP1400. Among them, Hualong One is a pressurized water reactor developed as part of China’s effort to secure a leading position in the global Generation III nuclear market and is widely regarded as one of the most extensively deployed Generation III reactor designs in the world. According to China General Nuclear Power Group (CGN), each Hualong One reactor generates approximately 1,209 megawatts (MW) of electricity annually, while more than 88% of its components and systems have been localized, from design through critical equipment manufacturing. More than 40 Hualong One reactors are currently operating, under construction, or approved for construction worldwide.

CGN’s Taipingling Nuclear Power Project also employs Hualong One technology. The project is a large-scale development involving six Hualong One reactors across three phases, with total investment approaching $16.7 billion. Upon completion, the facility is expected to generate more than 55 billion kilowatt-hours (kWh) of electricity annually. The environmental benefits are also substantial. CGN estimates that the project will save 16.65 million metric tons of standard coal each year and reduce carbon dioxide emissions by roughly 50.82 million metric tons. Such gains are expected to reinforce the cost competitiveness of Chinese manufacturing amid increasingly stringent global environmental regulations.

The standardization framework has enhanced not only construction scale but also cost competitiveness. China is building advanced Generation III reactors, including Hualong One units, at costs of roughly $2 to $3 per watt, a fraction of the approximately $15 per watt required for the latest nuclear projects in the United States. Significant disparities also exist in construction timelines. China typically completes new nuclear facilities in about six years, while the United States’ newest Vogtle reactors required more than a decade to finish due to regulatory bottlenecks and construction delays.

Signs of a Shift in the Global Nuclear Landscape

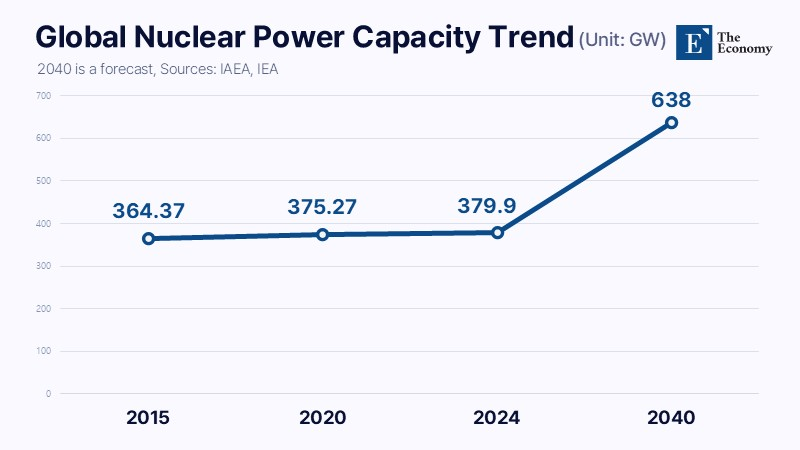

Leveraging these capabilities, China appears well positioned to secure a meaningful share of the rapidly expanding global nuclear market. In November of last year, the International Energy Agency (IEA) projected that worldwide installed nuclear capacity would reach 638 GW by 2040, a notable upward revision from the 586 GW forecast issued a year earlier. The International Atomic Energy Agency (IAEA) likewise raised its 2040 outlook for global nuclear capacity from 491–694 GW to 519–710 GW.

The United States is widely viewed as China’s principal competitor in the nuclear sector. In May of last year, U.S. President Donald Trump signed four executive orders and declared a “nuclear renaissance,” outlining a plan to expand the nation’s nuclear generating capacity from roughly 100 GW today to 400 GW by 2050. However, experts remain skeptical about whether Washington can achieve those ambitions. One industry specialist noted that “decades of limited new reactor construction have significantly weakened America’s nuclear supply chain and manufacturing base, while aging infrastructure and a shortage of skilled labor continue to pose challenges,” adding that “meaningful capacity expansion will require the reconstruction of manufacturing, fuel, and workforce ecosystems in addition to regulatory reform.”

France, the world’s most nuclear-dependent major economy with roughly 70% of its electricity generated from nuclear power, is also pursuing expansion plans that include six new EPR2 reactors and consideration of an additional eight units. Yet declining execution capabilities have become increasingly apparent, as exemplified by the Flamanville 3 project, which suffered delays exceeding a decade and costs that ballooned to several times initial estimates. State-owned utility EDF has likewise struggled with enormous investment burdens, supply-chain constraints, and labor shortages. Switzerland has also begun exploring a policy shift by considering the removal of its ban on new nuclear power plants amid rising electricity demand and energy security concerns. However, formidable obstacles remain, including high construction costs, radioactive waste disposal challenges, and a deeply divided public opinion landscape.

As one of the youngest members of the team, Tyler Hansbrough is a rising star in financial journalism. His fresh perspective and analytical approach bring a modern edge to business reporting. Whether he’s covering stock market trends or dissecting corporate earnings, his sharp insights resonate with the new generation of investors.

Similar Post