Markets Bet on Rate Hikes While Trump Pushes for Cuts, Warsh Faces First FOMC Test

Authored On

Modified

Growing hawkish sentiment within the Fed following strong employment data, with rate hikes now entering the discussion Trump insists that economic growth does not automatically translate into inflation and continues to advocate rate cuts Warsh focuses on trimmed-mean inflation measures, raising questions over potential groundwork for future easing

Federal Reserve Chair Kevin Warsh has found himself facing his first major interest-rate decision test just two weeks after taking office. Only a few months ago, market attention was focused on when the Federal Reserve would begin cutting rates. That narrative has shifted dramatically following employment data that proved far stronger than anticipated. On Wall Street, a growing number of analysts argue that the Fed’s rate-cutting cycle has effectively come to an end, while some investment banks have begun discussing the possibility of rate hikes before year-end. At the same time, President Donald Trump continues to call for lower rates, deepening the policy dilemma facing Warsh.

Trump Pressures Fed Again: “Why Raise Rates When the Economy Is Strong?”

On June 7, Trump said during an interview with NBC’s Meet the Press that “interest rates should not be raised to the detriment of the country” and that “there is absolutely no reason to raise rates.” He added, “We have grown the economy in a low-rate environment, and raising rates is no different from undermining that success,” arguing that rates should instead be lowered given the economy’s strong performance.

The remarks drew particular attention because they came immediately before Warsh was set to chair his first Federal Open Market Committee (FOMC) meeting. Referring to the new Fed chair, Trump said, “Kevin is a terrific person, and I want him to make his own judgment. I do not want to exert excessive influence on him.” Nevertheless, he reiterated that “the economy should not be penalized through rate hikes when it is performing well” and stressed that monetary policy should support growth. Trump also reaffirmed his longstanding position that lower interest rates would reduce government borrowing costs and provide greater fiscal flexibility. “The United States has enormous debt and many challenges that must be addressed,” he said. “I would like to invest more in national defense.”

This was far from the first time Trump had called on the Fed to cut rates. He has repeatedly suggested that his instincts are superior to the Fed’s judgment and, since returning to office, has increasingly sought to influence monetary policy through personnel decisions and public statements. The appointment of Warsh has widely been viewed as part of that broader strategy. Trump frequently criticized former Fed Chair Jerome Powell for being reluctant to cut rates and openly signaled his expectations for monetary easing following Warsh’s nomination. As a result, some observers speculated that tensions between the White House and the Federal Reserve could persist even under the Warsh era. CNN reported that Trump even joked earlier this year that he would sue Warsh if he failed to cut rates.

Iran War Inflation Risks Rise as Wall Street Bets on Rate Hikes

On June 7, Trump said during an interview with NBC’s Meet the Press that “interest rates should not be raised to the detriment of the country” and that “there is absolutely no reason to raise rates.” He added, “We have grown the economy in a low-rate environment, and raising rates is no different from undermining that success,” arguing that rates should instead be lowered given the economy’s strong performance.

The remarks drew particular attention because they came immediately before Warsh was set to chair his first Federal Open Market Committee (FOMC) meeting. Referring to the new Fed chair, Trump said, “Kevin is a terrific person, and I want him to make his own judgment. I do not want to exert excessive influence on him.” Nevertheless, he reiterated that “the economy should not be penalized through rate hikes when it is performing well” and stressed that monetary policy should support growth. Trump also reaffirmed his longstanding position that lower interest rates would reduce government borrowing costs and provide greater fiscal flexibilityYet surging inflation concerns stemming from the Iran conflict, combined with employment data that significantly exceeded expectations, have made immediate rate cuts difficult despite Trump’s demands. Earlier this year, markets expected the Fed to lower rates roughly three times before year-end. Rising unemployment and signs of slowing hiring activity had fueled expectations that the central bank would pursue further easing to shield the economy from weakness. Indeed, concerns over labor-market cooling were a major factor behind the Fed’s three rate cuts last year.

Conditions have shifted dramatically since March. Job growth has rebounded, while consumer spending remains stronger than expected. In particular, expanding investment in artificial intelligence (AI) has emerged as a new engine of growth for the U.S. economy, driving renewed labor demand. Competition among major technology firms to build data centers has sharply increased demand for electricity and raw materials, generating employment growth across related industries. The Fed is paying close attention to this development because it reflects demand-driven expansion rather than economic deceleration. Meanwhile, rising energy prices linked to prolonged tensions in the Middle East have added another layer of inflationary pressure. Over recent months, Fed officials have debated whether labor-market weakness or resurgent inflation posed the greater risk. Following the latest employment report, however, momentum appears to be shifting back toward inflation concerns.

The mood within the Federal Reserve is also changing. Cleveland Fed President Beth Hammack stated on June 5 that “maintaining current interest rates is appropriate for now,” adding that “if recent trends continue, it may soon become appropriate to take action.” While the statement ostensibly supported keeping rates unchanged, markets interpreted it as a signal that rate hikes were becoming a possibility. Hammack is regarded as one of the Fed’s more hawkish officials and was among those who argued during the April FOMC meeting that language implying the next policy move would likely be a rate cut should be removed. Dallas Fed President Lorie Logan has likewise indicated that she could support a rate increase later this year if current economic conditions persist. Only a few months ago, Fed discussions centered on the timing and magnitude of rate cuts. Now, the possibility of rate hikes is being openly discussed.. “The United States has enormous debt and many challenges that must be addressed,” he said. “I would like to invest more in national defense.”

This was far from the first time Trump had called on the Fed to cut rates. He has repeatedly suggested that his instincts are superior to the Fed’s judgment and, since returning to office, has increasingly sought to influence monetary policy through personnel decisions and public statements. The appointment of Warsh has widely been viewed as part of that broader strategy. Trump frequently criticized former Fed Chair Jerome Powell for being reluctant to cut rates and openly signaled his expectations for monetary easing following Warsh’s nomination. As a result, some observers speculated that tensions between the White House and the Federal Reserve could persist even under the Warsh era. CNN reported that Trump even joked earlier this year that he would sue Warsh if he failed to cut rates.

Wall Street has also revised its outlook. Morgan Stanley wrote in a report that “labor demand is accelerating beyond expectations,” adding that concerns about downside labor-market risks are easing while policy focus is shifting toward inflation. The bank expects the Fed to formally abandon its easing bias at the upcoming June FOMC meeting. Goldman Sachs expressed a similar view, arguing that strong employment growth increases the likelihood that the Fed will remove its easing bias in June and that a September rate hike can no longer be ruled out. BNP Paribas became the first major global investment bank to formally incorporate a rate-hike scenario into its one-year forecast. The bank expects the Fed to gradually reverse the three quarter-point rate cuts implemented last year beginning in December.

Warsh Signals Preference for Trimmed Mean Over Core PCE

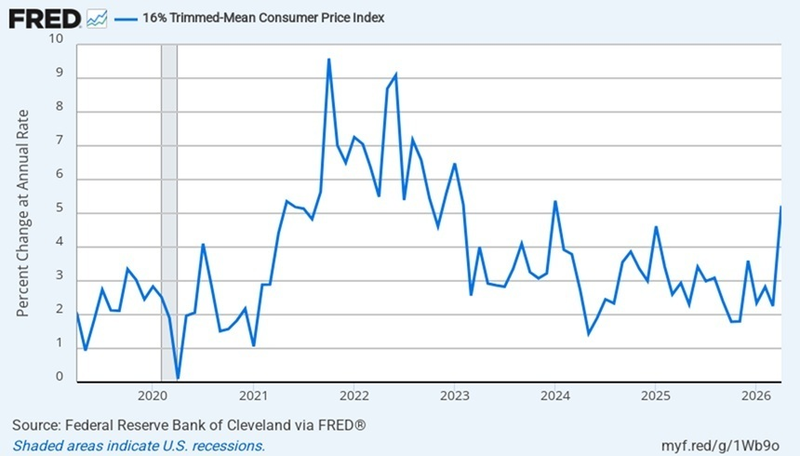

Contrary to market expectations, however, Warsh has adopted a stance viewed as more favorable toward future rate cuts, signaling that he intends to place greater emphasis on trimmed-mean inflation measures. The approach seeks to identify what he considers “true inflation” by statistically excluding the most volatile price components. The trimmed-mean inflation gauge is a version of the Personal Consumption Expenditures (PCE) index that emphasizes more persistent categories. Each month, PCE components are ranked by their rate of price change, with the lowest 24% and highest 31% removed before the remaining categories are weighted and averaged. By contrast, the core PCE index—the Fed’s traditional preferred inflation gauge—simply excludes food and energy prices, which are highly susceptible to supply shocks beyond the central bank’s control.

Analysts believe Warsh’s focus on trimmed-mean inflation reflects an effort to create conditions that could justify future rate cuts. According to the Federal Reserve Bank of Dallas, trimmed-mean PCE stood at 2.0% as of the end of February, precisely matching the Fed’s inflation target. The measure has been declining steadily since 2022. Viewed through that lens, the inflation environment could support lower interest rates.

Core PCE and headline PCE, however, continue to trend higher. On a six-month annualized basis, both measures stood at 3.4% at the end of February. Core PCE rose from 2.7% in November last year to 2.8% in December and 3.1% in January. Based solely on core PCE, rate cuts remain difficult to justify. One macroeconomic expert noted that “it is excessive to interpret every policy judgment by Chair Warsh through the lens of President Trump’s preferences,” adding, “Warsh has already served both as a Federal Reserve governor and as a private-sector financial executive, making it more likely that he will base monetary policy decisions on his own inflation framework.”

Warsh has also indicated that he may seek to eliminate the Fed’s forward guidance framework. His concern is that excessive noise surrounding future rate paths is being injected into financial markets. During his confirmation hearing on May 21, Warsh stated, “Unlike many of my colleagues, I do not believe in forward guidance,” adding, “I do not think future decisions need to be preannounced.” He continued, “Too many Federal Reserve officials are publicly expressing views about where interest rates should be at the next meeting, next quarter, or next year,” arguing that it is not particularly helpful when Federal Reserve governors or regional Fed presidents repeatedly communicate their personal policy preferences through speeches and media appearances. Whether he can overcome resistance from existing committee members and abolish forward guidance remains uncertain. Critics warn that such a move could inject significant uncertainty into financial markets, where countless participants rely on Fed guidance to forecast future interest rates and construct investment portfolios.

Similar Post