Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

Where you can plug in an electric car is now the biggest governor of how fast and fairly we can decarbonize road transport. Battery chemists and line workers have done their part: average pack prices sank below $140 per kWh last year, and the cheapest long-range hatchbacks routinely undercut the price of diesel saloons. Yet socket geography, not cell chemistry, still decides whether the next million motorists will drive mostly on electrons or slide back to petrol. The latest Global EV Outlook counts just under four million public charge points worldwide in 2023 – a 40% jump in only twelve months – but fully 70% of all charging sessions still happen behind private doors in owner-occupied garages. This imbalance threatens to recycle the housing-tenure divide into the climate transition: if you can afford a driveway, you get cheap, predictable refueling; if you cannot, you circle the block hunting for a live socket, or you keep your combustion car a little longer. This column argues that the policy reflex to subsidize wall boxes first and worry about curbside plugs later delivers diminishing environmental returns and widening inequity. A richer, mixed strategy that saturates public space with visible, data-rich high-speed chargers while valuing home convenience can cut carbon faster, cost governments less, and avoid turning the energy transition into a postcode lottery. The urgency of this shift cannot be overstated.

Socket Geography Is Destiny

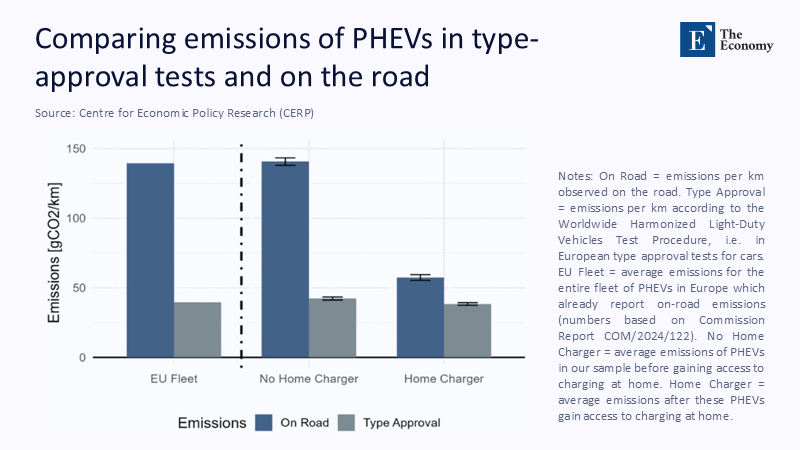

Infrastructure is not a neutral backdrop; it scripts behavior. Large-scale telemetry from European fleets shows that plug-in-hybrid drivers with a driveway socket cover roughly 55% of their annual kilometers in electric mode. In contrast, renters who rely on sporadic public access barely hit fifteen. The European Commission’s first real-world CO₂ monitoring report confirms the macro pattern. Across the whole EU plug-in-hybrid (PHEV) fleet, on-road emissions average 139 gCO₂ per kilometer – more than three times the type-approval rating – but households that have gained a dedicated home charger slice that figure to just 59 gCO₂/km. The insight is visualized in Figure 1 below. The left-hand cluster depicts the whole EU PHEV fleet; the center group isolates vehicles before they obtain domestic charging; the right-hand bars show emissions once those very same cars could refuel at home. The behavioral dividend of reliable charging is unambiguous. This data underscores the importance of transparency in driving informed decision-making in the electric vehicle industry.

However, private sockets alone cannot do the job because they only serve a slice of motorists. Roughly half the urban population in Western Europe parks on the street, while new apartment permits now outnumber single-family home permits by two to one. Therefore, a decarbonization script that assumes universal driveways is a demographic mirage. In geographic terms, socket density is destiny: streets with plentiful curbside or retail-car-park chargers convert hybrids into de facto electric commuters and tip undecided buyers toward full battery cars; neighborhoods without them lock residents into fossil kilometers, whatever the official vehicle mix says.

Counting Kilowatts, Counting Coins

For policymakers, the decisive question is where the next public euro (or dollar) of subsidy does the most climate work. A Level-2 wall box, fully installed, now averages about € 1,800 across the EU, with documented invoices ranging from €900 in benign wiring situations to well over € 3,000 where fuse boards and trenching need upgrades. Spread that median price across Europe’s 75 million detached and semi-detached homes, and the bill will approach €135 billion before a single additional kilometer is driven by battery power. By contrast, a 150 kW public fast charger, including transformer and civil works, still costs comfortably under € 100,000, and each of those high-speed units can deliver half a megawatt-hour of energy on a heavy Saturday, serving dozens of vehicles that do not own driveways. Therefore, a quick rule of thumb holds: shifting even 10% of the planned wall-box budget toward shared infrastructure would add roughly thirteen thousand motorway-grade chargers, multiplying the socially accessible kilowatt-hours per euro of capital outlay several-fold.

Economics alone, however, does not persuade drivers; information completes the loop. A recent NBER study tracking six US interstate corridors demonstrated that publishing real-time availability data for existing DC chargers could raise regional electric vehicle (EV) sales by up to 26% – an effect indistinguishable from a € 3,000 purchase rebate in uptake models. Drivers are not irrational; they treat time as a price. Every minute spent queuing at a charger or detouring to find one inflates the perceived cost of electric motoring. When a phone app can confirm, in real time, that a functional plug awaits three kilometers ahead, the risk premium collapses, and adoption accelerates. Hardware and software thus form a single policy lever; neglect either, and behavior reverts to petrol.

Revisiting the Hybrid Contract

The CEPR column that sparked this debate correctly warned that plug-in hybrids could be climate impostors if owners rarely plug them in. Yet Figure 1 already hints at a corollary: hybrids become genuine abatement machines when sockets are ubiquitous. Norway supplies a natural experiment. By the end of 2024, the country had one public charger for roughly every 150 EVs on the road, and almost 90% of all new passenger cars sold were battery-electric despite Arctic winters that sap range. That charger density allows even PHEVs to run on electrons for the lion’s share of daily travel, with combustion only for the trans-fjord holiday or the mountain-cabin weekend. Public infrastructure turns hybrids into range-extended EVs while the supply chain scales cobalt-light chemistries for future pure battery models. This success story should inspire hope and optimism for the potential of public infrastructure to drive positive change in the electric vehicle industry.

The Hidden Costs of a Wall-Box Monoculture

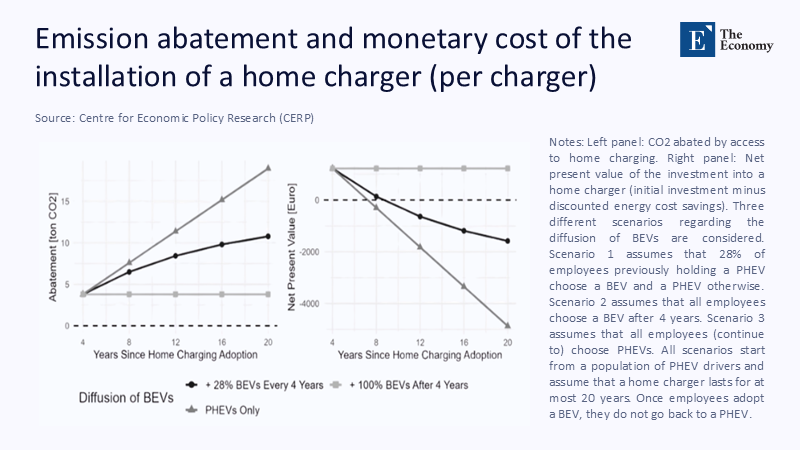

Advocates of a driveway-first strategy often cite convenience and cheap off-peak tariffs as decisive. Both points stand, but they disguise three externalities. First, grid reinforcement costs rise faster in cul-de-sacs than along trunk routes. A subdivision in which 80% of houses install simultaneous 11 kW chargers can overload a feeder built in the 1990s for night-time lighting load; upgrading that buried copper costs municipalities real money. Second, a private-socket monoculture exacerbates social inequity: higher-income households capture the lion’s share of purchase subsidies, fuel savings, and low-emissions-zone exemptions, while renters pay higher per-kilometer costs at scarce rapid chargers. Third, the strategy risks technological lock-in. Figure 2 – drawn from a new cost-benefit analysis – models the net present value of installing a home charger under three scenarios of battery-electric-vehicle diffusion. If BEVs reach 100% of staff car choices within four years, the investment barely breaks even in carbon terms and sinks deep into negative financial value for the household; only under a counter-factual “hybrids forever” world does the private wall-box keep delivering avoidable emissions.

That finding is intuitive: a fixed wall-bowl box emits most CO₂ during its early years, when its owner still drives a PHEV that would otherwise burn fuel on every cold start. Once that same motorist buys a full BEV – which—requires daily charging – the —final abatement from having a private socket rather than a reliable public one collapses.

According to the model, after roughly eight years, the cumulative cost of hardware and sunk capital swamps the discounted energy savings for all but the highest-mileage drivers. From a public finance viewpoint, continuing to underwrite wall boxes when public infrastructure can achieve the same system-level CO₂ cut for a fraction of the cost verges on misallocation.

Information Infrastructure: The Cheapest Charger Is the One That Already Exists

If real-time data moves purchase decisions as effectively as subsidies, open-data obligations should sit at the heart of infrastructure policy. Europe’s Alternative Fuels Infrastructure Regulation (AFIR) has mandated at least one 150 kW charger every sixty kilometers along the Trans-European Transport Network by 2025. But AFIR’s headline spacing metric says nothing about live status feeds, roaming-fee transparency, or queue-length disclosure. Those digital attributes are cheap – the cost of a SIM card and a server subscription – yet yield adoption dividends on a par with hardware. Norway’s statewide fast-charging map is updated every sixty seconds and includes fault codes; California’s Cal-ITP portal even logs average dwell time per location. The behavioral result is fewer failed trips, higher charger utilization, and a self-reinforcing loop of consumer confidence that hardware subsidies alone cannot buy.

Smart Tariffs, Bi-Directional Cars, and Grid Resilience

A perennial worry is that mass public charging will overload distribution grids. According to a recent IEEE modeling study, dynamic tariffs and scheduled charging can shift over 40% of urban demand into solar-rich midday or off-peak night windows without penalizing motorists. Public chargers at supermarkets and park-and-ride lots naturally capture those midday renewables, while office-car-park plugs soak up afternoon wind. Add bidirectional vehicle-to-grid capability, and Europe’s projected fleet could supply 20 GW of dispatchable flexibility by 2030 – rivaling a quarter of the continent’s pumped-hydro capacity for a fraction of the capital cost, provided cars are plugged in often and predictably. Shared infrastructure, again, raises the probability that an idle battery is physically connected when the system operator needs it.

A Five-Point Compact for Balanced Infrastructure

So, what practical policy architecture aligns with the evidence? First, make public subsidies conditional on open APIs: operators that do not stream live status and price data lose access to capital grants. Second, hard-wire equity can be achieved by channeling at least 30% of infrastructure funds to postal codes in the lowest income quintile, ensuring curb-side lamppost chargers reach the renters who need them most. Third, AFIR’s 60-kilometre fast-charger spacing should be maintained. Still, a density target of one public AC socket per ten battery-electric vehicles in circulation should be overlayed to avoid urban deserts. Fourth, tie company-car and purchase-tax incentives for PHEVs to real-world plug-in rates – an onboard telematics certificate showing at least 60% electric kilometers to retain rebates. Fifth, redirect a slice of current wall-box subsidies into a revolving fund for 350 kW “megawatt hubs” along freight corridors because electrifying light vans and rigid trucks are the next carbon frontier.

These five levers deliberately blur the stale binary of “home versus public” by favoring shared, visible, digital, and flexible infrastructure. A driveway plug is undeniably convenient, but its public value tails off sharply after early adopters are served. Conversely, each additional public charger benefits hundreds of potential users, reduces range anxiety well beyond its immediate neighborhood, contributes ancillary grid services, and unlocks genuine emissions cuts from hybrids that would otherwise burn petrol. In microeconomic terms, the societal marginal benefit curve for public chargers still slopes steeply upward; the curve for private wall boxes is already flattening out.

Build Where the Cars Already Go

The twenty-first-century refueling map will not mimic the petrol station network we grew up with. Instead of a thousand fenced forecourts, it will comprise thousands of curb-side posts, retail-park canopies, and motorway “energy hubs” that generate, store, and dispense electrons in one place. A policy that remains stuck in the driveway risks stranding capital, widening inequality, and slowing the sales curve right when the climate clock tells us to accelerate. The figures reproduced here – the stark fall in PHEV emissions once charging is habitual, the waning cost-effectiveness of domestic wall-boxes after the BEV wave breaks – make the trade-offs visible. Build chargers where the cars already go, not just where the affluent sleep, and the decarbonization dividend will arrive sooner, cheaper, and fairer.

The original article was authored by Johannes Gessner, a PhD candidate at the University of Mannheim, along with two co-authors. The English version of the article, titled "Home charging and plug-in hybrid electric vehicles: A strategy for real-world emissions reductions," was published by CEPR on VoxEU.

References

European Commission (2024). First Report on Real-World CO₂ Emissions from Passenger Cars (COM/2024/122).

European Council (2023). Alternative Fuels Infrastructure Regulation: New Law for Recharging and Refuelling across Europe.

International Energy Agency (2024). Global EV Outlook 2024: Outlook for Electric-Vehicle Charging Infrastructure.

International Energy Agency (2024). Global EV Outlook 2024 (PDF), Table 6: Public Charger Growth.

Lectrium (2023). How Much Does an EV Charger Installation Cost?

National Bureau of Economic Research (2024). Real-Time Charging Data and Electric Vehicle Adoption (Working Paper 33342).

National Bureau of Economic Research (2025). Digest: Real-Time Charging Data Could Accelerate EV Adoption.

Norwegian Ministry of Transport statistics quoted in Washington Post (30 May 2025).

Express Electrical Services (2023). Home EV Charger Installation Cost Guide.

European External Action Service (2023). Deploying Sufficient Alternative Fuels Infrastructure under the Green Deal.