A Policy Architecture for a Democratic Compute Coalition: Domestic Reform and Allied Coordination for AI Infrastructure

Published

The Economy Research Editorial*

*The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

As competition in artificial intelligence grows, so too does competition over the physical infrastructure required to train, deploy and govern it. This article outlines a policy architecture for a democratic compute coalition, based on the premise that democracies should compete with one another while coordinating. It argues that no single democratic power independently possesses the electricity, capital, semiconductor capacity, critical minerals, technical expertise and regulatory capabilities to secure the full AI infrastructure value chain. Domestically, the article advocates expedited permitting, transmission and interconnection reform, flexible load management and responsible behind-the-meter generation to accelerate commercial operation while protecting the environment, public health and democratic legitimacy. Internationally, it recommends pooled infrastructure finance, disciplined technology investment, coordinated investment in critical-mineral and semiconductor capabilities, compatible cybersecurity and safety standards and negotiated export arrangements for trusted partners. These measures could combine U.S. capital and chip-design expertise, Asian manufacturing capacity and transmission-system experience, European regulatory capabilities and allied energy resources within a more resilient democratic supply chain. The article emphasizes that domestic policy and international coordination are complementary: domestic policy influences the pace of infrastructure development, while coalition governance shapes the geographical distribution of that capacity and the safeguards giverning its use.

1. Introduction — Why the United States Cannot Build the AI Infrastructure Stack Alone

While conversations regarding the AI revolution are often about algorithmic breakthroughs or endpoint productivity improvements, there is a massive global energy and compute infrastructure behind every generative model or autonomous system. In 2024, data centers consumed approximately 415 TWh of electricity worldwide or around 1.5% of global demand, with AI expected to drive much of the projected increase to 2030.[1] These figures are a reminder that AI's current transformation is also an infrastructure transition. Current evidence points to a convergence of pressures - overburdened power grids, limited availability of advanced chips, geopolitical rivalries - that would require a very different policy framing than just regulating the algorithms. The future trajectory of AI will depend partly on the kilowatt-hours and raw minerals that go into training its models.[2]

This reframing clarifies why no single state - not even the United States - can create the entire AI value chain by itself.[3] While America is currently home to three-quarters of the world’s most advanced AI chip clusters, that advantage remains vulnerable.[4] Local barriers-which include overextended grids, slow permitting and growing community resistance-already delay projects and raise costs.[5] Abroad, China is mobilizing through state-led integration of clean electricity and digital infrastructure; Gulf states are offering low-cost carbon-intensive energy and faster permitting to lure hyperscale projects. This contest isn’t a zero-sum game; it’s a competition over where AI is regulated, the values it embodies and who can harness its capabilities. As the Carnegie Endowment explains, democracies must compete at home while collaborating abroad-and they must act quickly if they want to keep the AI value chain in a democratic world.[6]

Quite simply, the global AI build-out is a joint endeavor. It requires complementary national capabilities in geography, capital, energy, technical expertise and ciritical-mineral supply chains. A recent financial calibration of AI data-center economics revealed that time-to-power, the velocity of translating a project from plan to state-of-the-art operation, can outweigh marginal differences in operating costs.[7] From a policy perspective, the directive is clear: remove regulatory and infrastructure bottlenecks, modernize the grid and utilize available electricity efficiently. As America eliminates its own roadblocks, it must coordinate with allied democracies on what and where the AI supply chain will grow, including top talent, so that compute, semiconductors, critical minerals and other key resources remain concentrated in democratic jurisdictions. The article argues that the best way forward is a democratic compute coalition. It lays out recommendations for domestic policy to spark AI infrastructure construction, summarizes proposed international coordination tools that ensure that modernization remains rooted in democracies and ties the two sections together to propose a coherent policy architecture for 2026-2030.

The strategic stakes are substantial: if democracies succeed, democratic states can strengthen their position in advanced computing and guide AI development under democratic safeguards; if they fail, they risk ceding strategic advantage to authoritarian competitors operating under different incentives and weaker oversight. This article argues that this infrastructure dimension remains underdeveloped in the standard AI narrative, which contextualizes the debate primarily around computing as a software-driven productivity tool and does not sufficiently incorporate or address. However, viewing AI as a techno-economic ecosystem intrinsically connected to the physical infrastructure and resource constraints reveals important second-order effects: evolving regional labor markets, increased inequality (electricity "abundant" regions drawing talented people and investments away from "energy-scarce" counterparts) and shifting geopolitics. In light of these consequences, simple, purely domestic or laissez-faire policies seem dangerously partial. The article advances a positive strategy: democracies can simultaneously strive to shrink time-to-power individually and sustain international partnerships to create common momentum. The article concludes with concrete policy recommendations from scaled-up, accelerated permitting reform to focused allied investment policies that logically follow from the premises that infrastructure of supply is a location of strategic competition and that coalition-based rather than purely national strategies are necessary.

2. Domestic Reform — Shortening Time-to-Power While Preserving Democratic Legitimacy

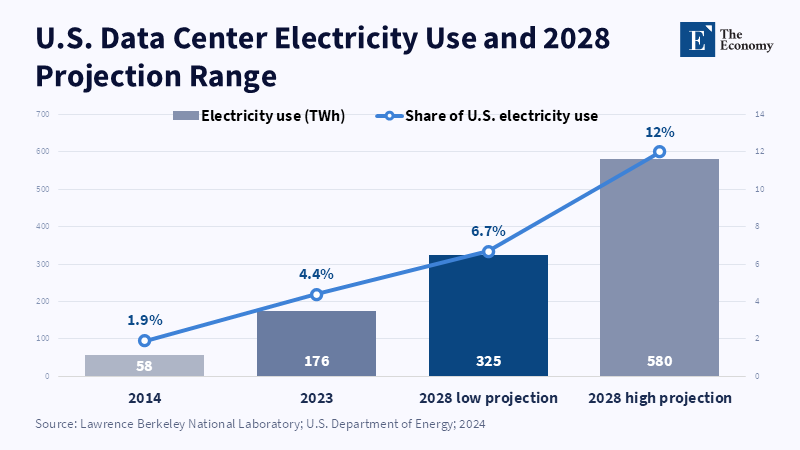

To sustain U.S. leadership in advanced AI, the United States must address self-imposed infrastructure constraints by reforming local regulations. Project experience increasingly shows that by the time an AI facility begins construction, its requisite power infrastructure and permissions will be five years behind schedule. Similar delays could derail other high-profile projects In California and Virginia, two hyperscale data centers requiring roughly one hundred MW remain unoccupied due to the utilities' inability to supply sufficient electricity. This risk is already visible in existing forecasts. While America's electrical generation sits essentially stagnant (Goldman Sachs foresees a further slowdown), AI-related electricity demand is rising rapidly.[8] The demand for data centers is expanding to the extent that the binding constraint is shifting from chip supply to power availability.[9] In a recent analysis, Goldman Sachs characterized the United States power generation effectively.[10] Despite this statistic, data-center demand could account for between 6.7% and 12% of U.S. electricity consumption by 2028.[11] Should the growth trend of this data hold, then this percentage could grow to 12% or greater by 2035. In that scenario, waiting a single year to get to operation would incur the costs of hundreds of billions of dollars and the $500 million (inflation-adjusted) difference (roughly) between a year's worth of production and a year's worth of delay would be equivalent to 5 % of the entire project revenue stream.

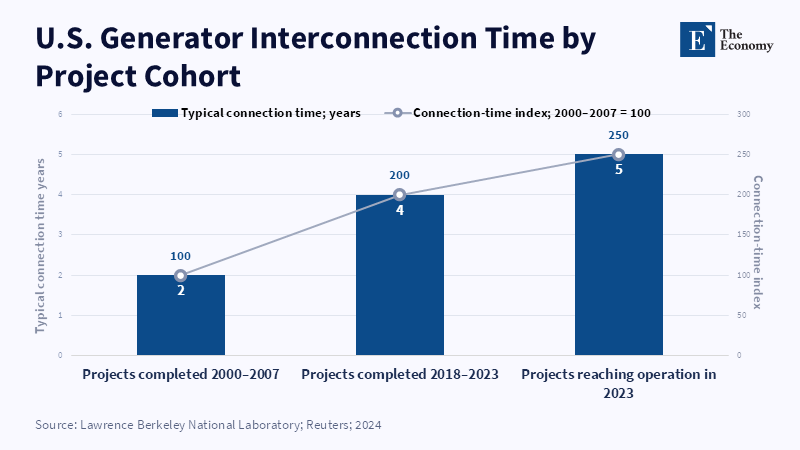

Recognition of the problem has prompted some action, but slow progress, contrary to the industry’s normal pacing. While the Trump administration has succeeded in making infrastructure reform an explicit priority, even claiming certain on-elevation grid projects to be critical to national security, it has used its emergency authorities on NEPA regulations. Yet new transmission lines and substations can still take years to approve and construct- the fact is that utilities in the United States have an average 5-7 year wait just to get a new power station hooked up to the grid, while a grid like Texas's ERCOT often employs a low-cost "connect-and-manage" doctrine to bring waiting down to two or three years.[12] These delays reveal structural weaknesses in the U.S. grid: Lawrence Berkeley Lab calculates that, by 2028, the consumption of data centers will go from 4.4 % of U.S. electricity consumption to approximately 12.0%. Together, these constraints risk eroding U.S. competitiveness relative to China’s infrastructure expansion and the Gulf’s faster project-delivery model.

What reforms can materially shorten time-to-power? Several drivers are evidence-based: first, permitting and appeals must be expedited.[13] Instead of protracted jurisdictional disputes between federal, state and local authorities, States ought to establish firm, short-term limits (perhaps a matter of weeks) on final decisions on data-center and other energy projects. One specific policy that utilities, developing data-center firms and local communities should push is a time-limited, criteria-based permitting pathway: when data-center developers agree to reach certain, high-value behind-the-meter (BTM) or grid transmission goals, then regulators should place their application at the head of the line instead of subjecting it to avoidable delay. For example, developers in cities who identify community value in finding markets for BTM energy investments or sponsoring transmission upgrades might receive priority review. Some U.S. states and federal agencies are already considering related reforms, while business and technology leaders have called for lower administrative barriers to accelerate data-centre development: some US states and the US government are already considering them and other national, financial and technology leaders have called for lower "red tape" to allow their firms (or any firm) to reach business more quickly and new data-center projects to be completed early in America's long future.

Second, the electric grid itself will have to become more adaptable and more extensive. Hyperscale computation behaves quite differently from traditional industrial loads, which draw large, continuous electricity loads.[14] The existing grid was not optimized for that. It is dependent on aging transmission infrastructure and constrained substations. Even during times of abundant, cheap renewables, the transmission grid has grown only modestly, as AI and renewables are battling for a limited pipeline capacity. In order to adapt, regulators should promote innovative grid models. A promising approach is to mandate changes to interconnection queues, for example, replacing the "invest-and-connect" model of sending entire transmission upgrades before the first megawatt is received with a connect-and-manage approach[15] of plugging into the grid immediately and handling overload through dynamic response. Texas's ERCOT is one case study of this more innovative approach, simultaneously planning long-term grid upgrades and connecting large projects significantly faster than comparables. Additional reforms include accelerating the development of enormous "spine" lines and establishing that temporarily turning off unviable loads is legal.[16] On the demand side, data centers can operate more flexibly: shifting a small share of flexible workloads could materially reduce peak demand and release effective system capacity in the United States and the European Union.[17] By incentivizing granular load flexibility through flexible interconnection commitments, data centers will have a strong incentive to discover how to effectively utilize temporal and geographical options.

Third, governments should promote behind-the-meter (BTM) power as a transition step. Where transmission upgrades will take years, many data-center operators are opting to deploy on-site generation paired with local renewables.[18] As of 2025, a growing share of U.S. data centers rely on some type of on-site power solution. Microgrids, gas-powered fuel cells, wind and solar-these can often be installed more quickly than new transmission lines once regulatory roadblocks are cleared. For example, even a patchwork U.S. transmission system takes 10-15 years to fully implement, whereas a custom “permit fast lanes" scheme could be used for launch-ready BTM efforts that operate with limited grid dependence until network capacity expands. Recent deployment trends reinforce this option: in 2024, 40 GW of solar capacity was installed in the United States[19] and about 60 GW in Europe,[20] all of which can immediately be used on-site at data campuses. AI colocation data-centre operators are already pouring money into co-located solar and battery farms, along with AI infrastructures. Governments can also encourage accelerating these developments through targeted incentives (tax breaks or R&D subsidies) as well as pre-supervising green projects in prospective data sites. In particular, priority should be given to deploying clean fuel cells that operate on hydrogen, as they can enable deployment rapidly and may reduce local emissions and act as a hedge against seasonal grid gaps, compared to typical diesel gen sets. Overall, behind-the-meter power represents a democratic approach in democracies to bridging the "time-to-power" shift without relying on high-carbon backup generation indefinitely. Such systems can also improve resilience during extreme weather or grid outages, particularly where they support local backup services.

These domestic reforms address different stages of the project timeline: fast-track permitting, grid modernization, flexible demand management and the creation of BTM. The goals are related and the consequences are large: Even doubling US electricity prices in the world's most efficient data center increased valuation less than a year's delay did in the Carnegie financial model. Moderation in tariffs, or small tax reforms, could easily be dwarfed by a year's lag. Conversely, domestic policy reforms, at the right speed, can have substantial returns: if India or Germany can shave a year off their average data-center project timeline, their AI infrastructure competitive rankings would improve their relative competitiveness. In the logic of economists, domestic officials should not see fast approvals and grid outlays as distorting the market, but as game-changing:If a state or country can establish and operate a data center 12 months earlier than another state or country, they reclaim the related jobs, taxes and spillovers.

No single reform is sufficient. Changes to utility rules or zoning may seem bureaucratic, but taken together, those moves decide whether an economy will have top-tier computing capacity or choose to have it elsewhere. This is not a private technology-sector concern: as AI deployment accelerates, workers and firms in the winning regions will enjoy productivity gains, while those outside will stagnate and go into a downturn. Energy-scarce regions will also be denied the new digital manufacturing jobs, deepening the gulf between energy-intensive and less energy-intensive economies. To shorten time-to-power, extending compute benefits more broadly, this won't be a specialized industry subsidy; it's a default labor-market and development challenge.

At the same time, officials must weigh speed against social license, or public acceptance. Over the years, communities have often responded negatively to big industrial projects as overly intrusive or unsustainable. Fast processing can't become a free ticket to sideline local or other environmental concerns. Instead, governments should pair facilitating processes with explicit, agreed-upon measures (for example, new data centers must show valid grid benefits such as feeder upgrades or community investments).[21] Legitimacy in democratic systems derives from process as much as transaction. Conversely, authoritarian regimes eschew such discussions, but democracies must garner public support. The less desirable alternative is for project delays to drive construction abroad, along with the associated economic value.

Overall, America's prospects as a data-center powerhouse hinge on how well policymakers perform. Congress and regulators should redouble efforts on reforming permitting, accelerating grid build-out and accelerating interconnection processes. Bipartisan signals already suggest that they intend to do so (through the 2023 BUILDER Act amendments and proposals for upcoming DOE rules), but the processes must be expedited. Private industry too has a part to play: cloud providers can provide credible demand forecasts by collaborating with utilities to coordinate planning, while strengthening local workforce development can increase support at the community level. Should the US manage to shave months off project economics, it will unlock a substantial share of the investment required for immense high-end compute growth. Importantly, though, domestic pressure alone will not be sufficient. Even with US permitting overhauls, chip shortages or a critical minerals crunch occurring in other regions might impede the build-out. The following section explains why, to sustain leadership in advanced computing, the US must adopt the very same globalizing playing field that fostered the triumph of Silicon Valley: an international, cross-border approach to cooperation.

3. International Coordination — Designing a Democratic Compute Coalition

In essence, setting up AI infrastructure throughout democracies is akin to setting up a pipeline that crosses an entire continent, pooling capital, expertise and security capacity across countries. No single jurisdiction possesses all the required inputs to achieve it alone, but with their combined resources, democracies can shift substantial processing power, where raw materials become large ML models. The fundamental point: while democracies must competitively draw projects locally, they should, out of strategic necessity, operate in a way that keeps the volume of processing (from raw elements to large models) within a sustainable and open ecosystem. Both of these goals require:

A first institutional priority is using the United States’ time-tested partnerships in energy and energy infrastructure. There should be no uncertainty on where to build the next nuclear plants or HV (high voltage) lines; allies with decades of experience can be enough to solve any infrastructure-design challenges. For instance, South Korea is the global leader in electrical engineering and grid management. South Korean firms such as Daehan Cable and KEPCO are already entering the United States through large transmission projects (e.g., a $74mn turnkey project in Southern California).[22] On the other hand, South Korea relies on U.S. liquefied natural gas and advanced reactors to supply its energy needs.[23] This mutual energy dependence deepens bilateral energy cooperation between the Korean and American grids, reaffirming their cooperation.[24] Those two old economic ties can be reinforced by establishing a strategic alliance. U.S. agencies and their Korean counterparts could jointly identify the intersection between new digital hubs and carbon emissions goals, allowing for large-scale grid upgrading, such as transmission lines feeding not only digital factories, but also data centers, so they can attain economies of scale. This strategic plan could also see the U.S. imports of Korean submarine cables and grid management programs or even joint ventures to install EV chargers and modular nuclear plants across the digital factories. Put differently, their alliance could evolve by converting giant LNG and energy agreements into next-generation computational ones.

Japan and other East Asian allies contribute vital technology and investment. Japan already is specializes in automation, robotics and semiconductor equipment, which complements U.S. expertise in chip design.[25] Under the U.S.-Japan chip accord and the CHIPS Act, Tokyo has aligned elements of its high-technology supply chain with U.S industrial policy; there is much potential to build on that by encouraging Japanese investment in fabrication plants and even data-center construction by American firms.[26] Japanese companies have an important role too in hardening the grid, such as Hitachi and Toshiba in the manufacturing of transformers and Sumitomo in financing renewable energy projects. In return, Japan will enjoy assured markets in the U.S. for its technology exports and there is no need to single-source digital products from Chinese cloud services, which would be integral to any last-mile AI architecture among democratic powers. Although a U.S.-Japan AI infrastructure plan is nascent, it potentially could address various items such as joint research on the next generation of fault-tolerant chips and the use of a joint "intelligent grid 2.0" standard to align evolving AI-enabled datacenters.

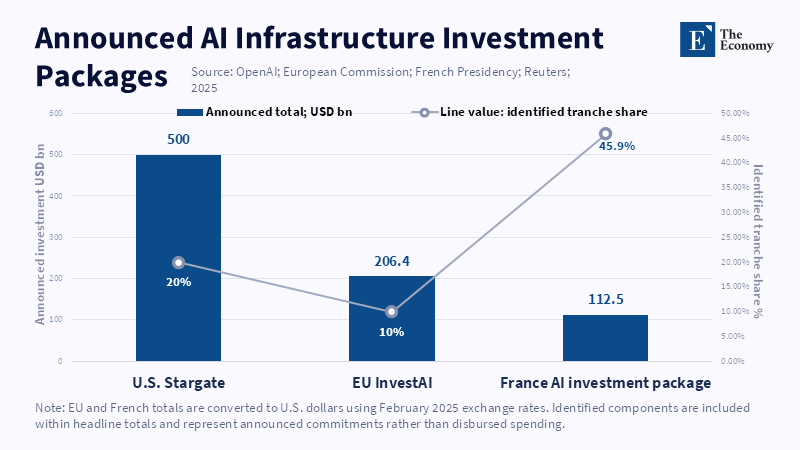

Europe brings substantial renewable power and well-established regulation to the table.[27] It has established ambitious renewable targets - such as 100 GW of solar and wind projects in the 2030s- and taken the lead in offshore wind. There, alone, Europe connected an additional 60 GW of solar capacity in 2024. These sources could support future data centers with near-zero carbon electricity and limit the pressure on American baseload generators. Europe must also expand its own compute capacity. When looking across the Atlantic, the EU27 have not announced more than a handful of AI giga-projects to come online by 2025, commanding only a few percent of the world’s compute. To lead, democracies need to deploy a staggering amount of capital. The EU27 should coordinate state efforts via measures such as the proposed AI Gigafactory program and joint EU AI research, development and infrastructure funding.[28] Similarly, North American trading partners such as Canada and Australia should be integrated. Australia has not established any significant AI hardware giga-factories yet, but could create specific industrial zones or express-passes to supply data center campuses and benefit from cheaper land and its hydrogen and other low-carbon technologies.

Of course, these infrastructure policies have security implications as well. Allies simply cannot afford to liberalize cross-border investment without appropriate safeguards, sending billions of dollars to pour into AI data-centre projects, without guardrails. That's why one of the most promising ideas is allied fast-track investment screening. Effective coordination requires mutual confidence in allied screening systems. It cannot allow one administration to use concealment or expropriation to undercut another, but, at the same time, current foreign investment review mechanisms, such as U.S. CFIUS,[29] EU FDI screening[30] and the Australian FIRB[31] can cause delays or blockages on transnational AI projects. To overcome this problem, democracies might arrange a common acceptance or fast-track system for each other's AI-related deals. For instance, in the event that a U.S. Technology firm wants to establish a data center in Canada, Canadian and U.S. authorities could apply compatible risk criteria and secure information-sharing rather than duplicate equivalent reviews and repeat the same exercise in U.S. Likewise, a pan-democratic AI Alliance Screening Forum could examine potentially sensitive investments and share relevant findings across participating countries,[32] with the inherent advantage of reducing uncertainty and discouraging opportunism. The objective is not to abandon due diligence, but to rationalize standards so that capital moves freely through trusted channels rather than clogging up high-tech projects with duplicative review procedures across jurisdictions.

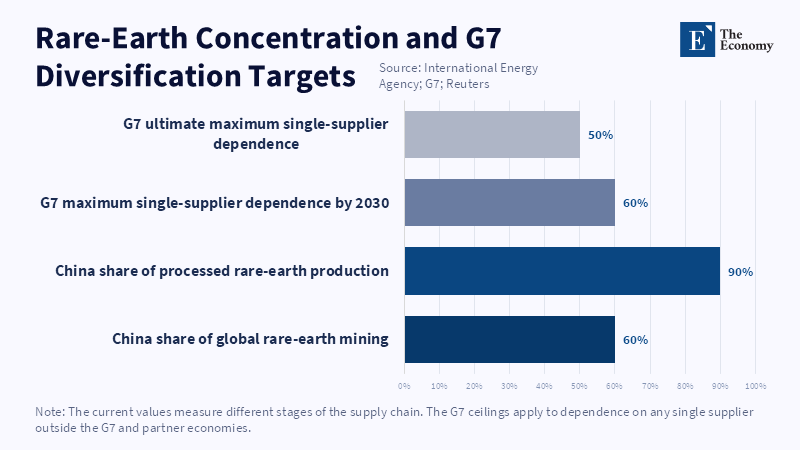

Critical minerals are another coordinated choke point. Chips and servers all depend on inputs such as cobalt, lithium and nickel that are geographically concentrated outside many democratic jurisdictions.[33] One solution would be a jointly-staffed strategic reserve or financing institution for critical minerals. Democracies-the United States, Australia, Japan and EU member states could bring together funds to back new mines in resource-rich, yet capital-poor African or Latin American nations, if environmental standards are respected. The nascent US-Australia Critical Minerals Partnership, announced in 2023, provides a foundation but requires greater scale.[34] Democracies could also co-finance domestic processing plants to avoid single-country bottlenecks or economic coercion.[35] Conversely, leaving mineral procurement purely to uncoordinated markets risks rivals shutting mines or raising prices during war or crisis. The recently convened OECD forum on critical minerals revealed that common supply-chain resilience is now essential both to energy and to tech security, making multilateral agreements on specialty metals critical.

Beyond physical infrastructure, democracies can focus on aligning safety and standards on AI use.[36] A fragmented approach to regulation pushes those building data centers to rely on regulators offering "light touch." Instead, democracies-perhaps starting with allies such as the US, Japan, the UK, Israel, South Korea, Canada and Australia-could find consensus on shared safety standards-for instance, standards for protecting data centers from hacking, or testing protocols for different types of AI models-that make compliance straightforward.[37] For instance, the Biden administration proposed an AI Diffusion Rule based on tiered access to advanced chips.[38] However, the rule was rescinded before taking effect.[39] A broader-based consensus, co-developed by a coalition such as the G7, might guarantee that advanced chips and AI tools are more readily available to democracies that satisfy those standards. For example, any AI chip maker that imports or exports chips outside the US would do so only with partners undertaking a reciprocal certification arrangement.[40] Such limits on exports could spur investment in and supply of the free world: a country might access next-gen data centers that adhere to coalition standards in exchange for agreeing to security and non-diversion commitments.

Finally, coordinated financial instruments could also deepen the coalition. Democracies could mobilize joint infrastructure bonds or investment funds for allied AI buildouts; Compute Fund, financed by the US, EU, Japan and others, could provide inexpensive loans toward greenfield projects of host institutions in Europe or India for fostering a faster buildout without subsidizing any one pocket.[41] Simultaneously, proportionate enforcement mechanisms (e.g., suspension of defense contracts or trade benefits) could be levied against states that sabotage, in bad faith, the disrupted supply chains of an aligned network. While they represent less direct incentives, these instruments may be needed if AI is to support durable shared prosperity.

In sum, democracies should continue competing on these various grounds domestically; faster time to market and cheaper costs are still the biggest draw for global tech capital, just not at the cost of forgoing international solidarity. Sharing the effort does not make each country worse off; it makes everyone better off by "spreading the risk." Consider this: U.S. states, rather than the U.S. Federal government, working together to meet in Africa the stricter European standards for data-center operation, help more than just those states get access to European cloud consumers; South Korea, working with other nations, to sell its best grid technology, is not just good business for Korean manufacturers, it funds global grid reliability that drives AI to serve residents of California or Texas. Similarly, with jointly financed research centers for quantum technology or battery storage at the University of Washington or Imperial College in London, respectively, both countries get much more in innovation gains than they could alone.

Ultimately, computing is a new kind of geopolitical stake. Those who acquire plentiful and reliable AI hardware and infrastructure will have the means of enforcing regulations and managing disruptions. A compute coalition, if established, would unify democracies around mutual self-interest and mutual competence in that AI power acceleration. It would help ensure that when next-generation models come to market, they are delivered on grids compatible with democratic standards, as well as open methodologies, incident-reporting and human oversight embedded in the system.

4. Conclusion — Compete Domestically, Coordinate Internationally

The scale and geographical dispersion of AI infrastructure require an international dimension, as a national approach is simply insufficient. The US and its democratic allies need to improve the domestic investment climate for AI. The competition should take place within a collaborative approach that reinforces, rather than constrains, the greater supply chain. Accelerating permitting processes, increasing transmission capacity, enabling more dynamic interconnection and responsible behind-the-meter generation can shorten time-to-power. Such activities need to be carried out in a manner that is mindful of grid reliability, affordability, environmental safeguards and robust local consultation.

International coordination is equally necessary. No liberal democracy independently possesses sufficient capital, energy, semiconductor capacity, critical minerals, hardware and technical know-how to dominate the whole AI chip-to-cognition value chain. A democratic compute coalition should therefore coordinate investment screening, pool infrastructure finance, integrate mineral and semiconductor supply chains, establish common security and safety measures and develop predictable export systems for trusted partners. This preferential treatment should be tied to meeting shared cybersecurity requirements, transparency, incident reporting and responsible infrastructure management.

The policy principle is therefore clear: democracies compete at home, coordinate abroad. Domestic reform defines how fast infrastructure will be erected, while international architecture defines whether the capacity that is built is resilient, distributed, and democratically governed. Together, they create the strongest conditions for broad AI adoption through secure, resilient and democratically governed infrastructure, while avoiding reliance on authoritarian or strategically unreliable suppliers and a narrow group of infrastructure providers.

References

[1] International Energy Agency (2025) Energy and AI. Paris: International Energy Agency.

[2] The Economy (n.d.) ‘The Energy Shock Behind Artificial Intelligence’. The Economy.

[3, 6, 7] Phillips-Robins, A., Tawil, T. and Winter-Levy, S. (2026) The Compute Coalition: How to Build the Future of AI in the Free World. Washington, DC: Carnegie Endowment for International Peace.

[4] Pilz, K.F., Sanders, J., Rahman, R. and Heim, L. (2025) ‘Trends in AI Supercomputers’, arXiv.

[5] The Economy (n.d.) ‘Power Failure: America’s AI Energy Bottleneck and the Coming Productivity Divide’. The Economy.

[8] The Economy (n.d.) ‘Surging Power Bills Squeeze U.S. Consumers: Data Center Expansion and Aging Grids Fuel Electricity Inflation’. The Economy.

[9] The Economy (n.d.) ‘U.S. Power Crunch vs. China’s Pipeline Push—AI Infrastructure Balance Falters’. The Economy.

[10] Goldman Sachs Research (2024) ‘AI Is Poised to Drive a 160% Increase in Data Center Power Demand’. New York: Goldman Sachs.

[11] Shehabi, A., Newkirk, A., Smith, S.J., Hubbard, A. and Lei, N. (2024) 2024 United States Data Center Energy Usage Report. Berkeley, CA: Lawrence Berkeley National Laboratory.

[12] Brookings Institution (n.d.) ‘The Closing Window of Opportunity for U.S. Global Technology Leadership’. Washington, DC: Brookings Institution.

[13] U.S. Congress (2023) Fiscal Responsibility Act of 2023. Public Law 118-5. Washington, DC: U.S. Government Publishing Office.

[14, 17] Electric Power Research Institute (2024) Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption. Palo Alto, CA: Electric Power Research Institute.

[15] Federal Energy Regulatory Commission (2023) Improvements to Generator Interconnection Procedures and Agreements: Order No. 2023. Washington, DC: Federal Energy Regulatory Commission.

[16] Federal Energy Regulatory Commission (2024) Building for the Future Through Electric Regional Transmission Planning and Cost Allocation: Order No. 1920. Washington, DC: Federal Energy Regulatory Commission.

[18] U.S. Department of Energy (2023) Pathways to Commercial Liftoff: Virtual Power Plants. Washington, DC: U.S. Department of Energy.

[19] Solar Energy Industries Association and Wood Mackenzie (2025) U.S. Solar Market Insight: 2024 Year in Review. Washington, DC: Solar Energy Industries Association.

[20] SolarPower Europe (2024) EU Market Outlook for Solar Power 2024–2028. Brussels: SolarPower Europe.

[21] Joint Legislative Audit and Review Commission (2024) Data Centers in Virginia. Richmond, VA: Commonwealth of Virginia.

[22] The Korea Herald (n.d.) ‘Korea’s AI Ambitions Run into Power Problem’. The Korea Herald.

[23] The Economy (n.d.) ‘U.S. Power Grid Overhaul Accelerates as Korean Firms Step Up Market Push Following $74 Million Daehan Cable Order’. The Economy.

[24] Baker Institute for Public Policy (n.d.) ‘Profit and Power: Opportunities in the U.S.–South Korea Energy Sector’. Houston, TX: Rice University.

[25] Ministry of Economy, Trade and Industry (2024) Strategy for Semiconductors and the Digital Industry. Tokyo: Government of Japan.

[26] The White House (2024) United States–Japan Joint Leaders’ Statement. Washington, DC: Executive Office of the President.

[27] Ember (2025) European Electricity Review 2025. London: Ember.

[28] European Commission (2025) InvestAI: An EU Initiative to Mobilise €200 Billion of Investment in Artificial Intelligence. Brussels: European Commission.

[29] U.S. Department of the Treasury (2024) Committee on Foreign Investment in the United States: Annual Report to Congress, Calendar Year 2023. Washington, DC: U.S. Department of the Treasury.

[30] European Commission (2024) Fourth Annual Report on the Screening of Foreign Direct Investments into the Union. Brussels: European Commission.

[31] Australian Treasury (2024) Australia’s Foreign Investment Policy. Canberra: Commonwealth of Australia.

[32] OECD (2024) Investment Policy Developments in 61 Economies between 16 October 2023 and 15 March 2024. Paris: OECD Publishing.

[33] International Energy Agency (2025) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

[34] Australian Government, Department of Industry, Science and Resources (2023) Critical Minerals Strategy 2023–2030. Canberra: Commonwealth of Australia.

[35] European Parliament and Council of the European Union (2024) ‘Regulation (EU) 2024/1252 Establishing a Framework for Ensuring a Secure and Sustainable Supply of Critical Raw Materials’, Official Journal of the European Union.

[36] Group of Seven (2023) Hiroshima Process International Code of Conduct for Organizations Developing Advanced AI Systems. G7.

[37] National Institute of Standards and Technology (2023) Artificial Intelligence Risk Management Framework: AI RMF 1.0. Gaithersburg, MD: National Institute of Standards and Technology.

[38] U.S. Department of Commerce, Bureau of Industry and Security (2025) ‘Framework for Artificial Intelligence Diffusion’, Federal Register, 90.

[39] Reuters (2025) ‘Trump Administration to Rescind Biden-Era Global AI Chip Export Curbs’, 7 May. Reuters.

[40] U.S. Department of Commerce, Bureau of Industry and Security (2022) ‘Implementation of Additional Export Controls: Certain Advanced Computing and Semiconductor Manufacturing Items; Supercomputer and Semiconductor End Use; Entity List Modification’, Federal Register, 87(197), pp. 62186–62215.

[41] Group of Seven (2024) Apulia G7 Leaders’ Communiqué. G7.