[EU vs. China] The Green-Digital Dependency Trap: China, Batteries, Photovoltaics and Europe’s Industrial Autonomy

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

Europe’s green and digital transitions are increasingly reliant on supply chains in which the end product has a final destination inside the Union but critical technologies, inputs, machinery, component supply chains and process expertise are located elsewhere. This paper examines this paradox through, in relation to lithium-ion batteries, solar PV and strategic electronics, suggesting that producing at home does not claim to be industrially autonomous: resilience is about having operational control over upstream inputs, process know-how and production technology, supplier base, private ownership and the ability to operate in times of crisis. The entrenched scale and technological depth of Chinese producers have helped reduce costs and speed up deployment in Europe, but have also arguably increased the dependence on certain linkages along the supply chain. In this context, to de-risk is not the same as to decouple: it calls for a nuanced policy of selective de-risking in the use and supply of critical products, rather than a wholesale decoupling of production facilities. European procurement and investment policies, industrial policy and competition rules should prioritise European control and resilience, technological learning and supplier diversification.

1. Introduction - From Geographic Localization to Effective Industrial Control

European discussions of strategic autonomy continue to shift between two less-than-satisfactory extremes. One continues to see import reliance as enough to indicate vulnerability. The other assumes resilience exists once production is physically shifted into the European Union. Both views are inadequate for the sectors that now form the centerpiece of Europe’s decarbonization and digitalization drive. In batteries, solar photovoltaics and a variety of electronic and high-end components, the critical difference is not just where production occurs in a geographic sense. It is whether that production is something Europe can control: whether it is output that is underpinned by diversified access to components and process know-how, intellectual property, machinery, skilled labor and upstream materials, as well as institutions that can preserve activity under duress. In that light, the key challenge is less how difficult it is to see the final imports of a product than how opaque control and sustainment remain inside supposedly local supply chains. A battery pack assembled domestically may still be reliant on Chinese cathode chemistry, Asian cell manufacturing, Chinese process equipment or a foreign firm’s decision about where margin, innovation and next-generation capacity will be located. A solar module installed on a European rooftop may cut gas imports but leave the continent unable to duplicate critical upstream stages at scale.

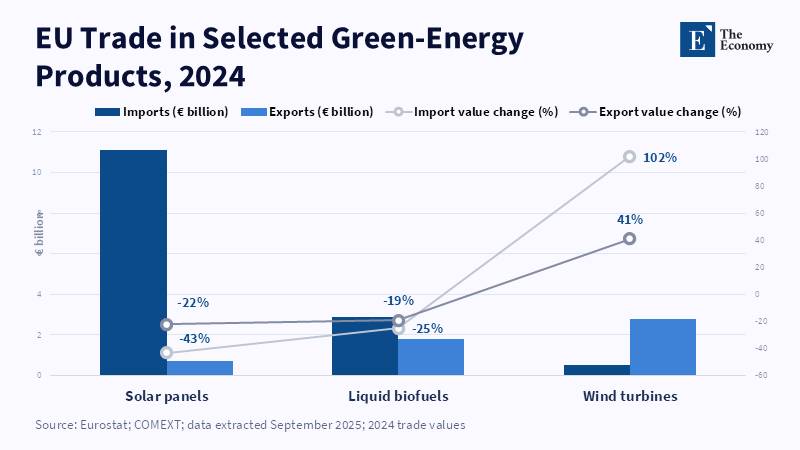

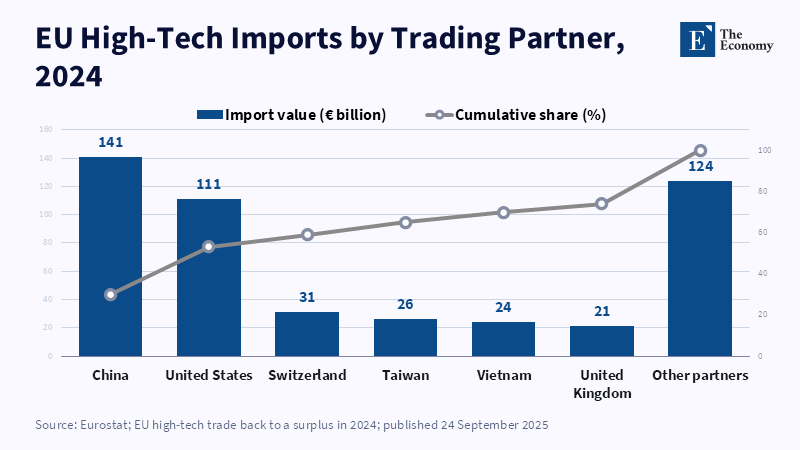

The pressing nature of this question intensified markedly between 2023 and 2026. Solar deployment continued to rise while EU panel imports remained heavily concentrated in China. Eurostat reports that 98 percent of those solar panels, which represented €11.1 billion of the 2024 total EU import of solar panels, came from China.[1] In the broader digital economy, Eurostat reports that in 2024, China was by far the leading source of the EU's high-tech imports (€141 billion of the €478 billion of total imported goods into the EU, or 30 percent),[2] even while the EU suffered a worsening goods trade deficit with China through 2026. EU exports to China declined.[3] These changes are significant not merely because they expand bilateral surpluses and deficits but because the green and the digital transitions are now intricately interwoven-electric vehicles, stationary storage, solar installations, electrified industry and much of the data-processing hardware used throughout the economy rely increasingly upon one another. Another recent analysis by the Carnegie Endowment measures the sectoral pattern with exceptional precision. On 2024 product-level trade data, it finds that China represented 52.8 percent of EU imports of lithium-ion cells, 54.5 percent of computers, 40.7 percent of smartphones and 63.7 percent of photovoltaic cells, even as intra-EU trade also commanded meaningful shares in all of those same products.[4] This point is of analytical relevance.

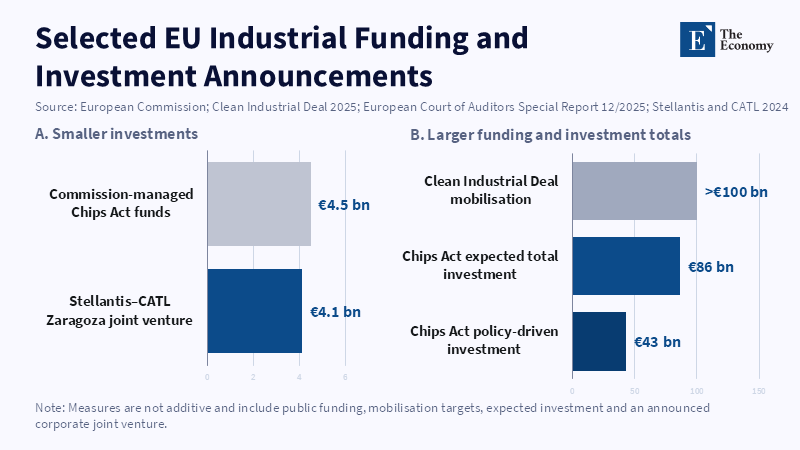

Substantial intra-EU trade may not refute a country's dependence but may instead witness Chinese-connected products, stakeholders and supplies coursing along the European supply chains. According to Carnegie, lithium-ion batteries alone may have furnished approximately $47.6 billion of the EU's 2024 high-risk imports, nearly 37 percent of the category value.[5] While not constituting conclusive evidence of strategic weakness, these figures constitute convincing proof that the raw material trade hinges heavily upon finely grounded categories featuring slow transition horizons, high qualification prerequisites and large-scale industrial lock-in. Evolutions of the policy environment are occurring just as swiftly. Brussels has been moving, too. The Net-Zero Industry Act builds resilience and other non-price conditions into specific parts of the public procurement and renewable-energy bidding process.[6] The Clean Industrial Deal will mobilize more than €100 billion to support clean manufacturing.[7] The Innovation Fund has announced dedicated support to battery-cell factories,[8] and the European Commission has already imposed definitive countervailing duties on Chinese-made battery electric vehicles after determining unfair subsidy practices.[9] Conversely, ongoing EU-China trade negotiations that are still planned for 2026 imply that Brussels and Beijing both will have reason to prevent these disputes from hardening into a broader economic standoff.

In other words, a full-fledged EU-China trade war is still only a possibility, not yet a certainty. Nonetheless, limited trade frictions have already entered the industrial fabric and any serious planning towards green-digital sovereignty needs to account for a future where access terms, prices and political agendas are in constant flux. The essence of the argument advanced here is that the EU can indeed achieve genuine green-digital autonomy, but only if autonomy is defined more carefully and pursued more selectively than much of today's discourse suggests. In these sectors, resilience does not mean self-sufficiency in the entire continent and it certainly does not mean reflexively excluding all Chinese capital or technology. Rather, it means having controlling access to a sufficient number of strategic chokepoints to enable deployable capacity in the face of a disruption; diversified cell manufacturing pathways for batteries, a credible upstream photovoltaic manufacturing base distinct from the module assembly stage, greater leverage elsewhere in power electronics and industrial equipment, policy instruments capable of teasing apart good and bad localization, not just in Europe but in the industrial world as a whole. The question, then, is not about having local production in the abstract: it is about avoiding a vision of Europe's green-tech and digital industrialization as an assembly layer on a value chain whose most competitive technologies, incentives and vulnerabilities remain elsewhere.

2. Lithium-Ion Batteries: Europe’s Flagship Dependency

Lithium-ion batteries provide perhaps the clearest example of whether Europe is gaining independence from the rest of the world – or merely shifting the map of dependence over time. Their significance is hard to overstate. They are central to electric vehicles, wearable electronic appliances and grid-scale storage and are at the crux of decarbonization policy, automotive industry policy and digital manufacturing. According to a 2026 report by the Carnegie Endowment, batteries alone represented roughly $47.6 billion, or nearly 37 percent of the value of EU high-risk imports in 2024.[10] This is not just an arbitrary number that derives from import volume. It demonstrates that the combination of substitution difficulty, broad industrial constituency and the way battery supply chains connect upstream minerals and chemicals to downstream manufacturing ecosystems. When a product has these three dimensions, the exposure begins to matter in a way that exceeds normal trade dependence. The global battery value chain structure explains why. As the International Energy Agency has repeatedly demonstrated, the battery market is not organized around cells alone, but around a tightly integrated set of operations from refining and precursor manufacturing to cathode and anode manufacturing and cell production, pack assembly and recycling.[11]

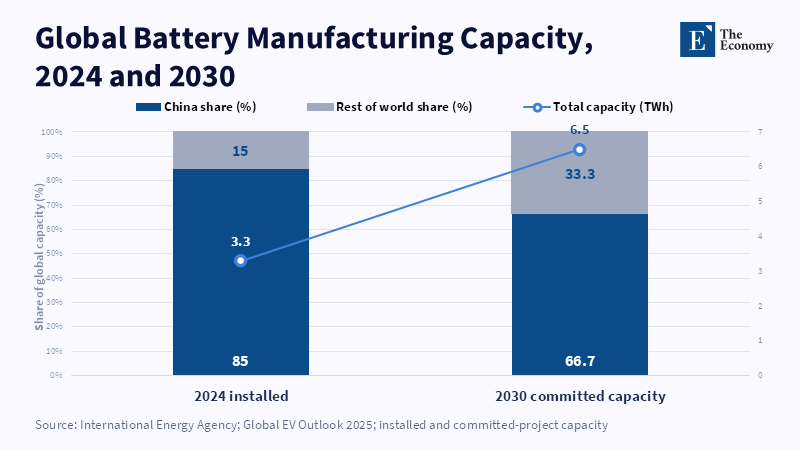

According to the International Energy Agency, while the manufacturers' capacity to produce battery cells stood in 2024 at over 3 terawatt-hours, nearly 85 percent remained in China; more than 75 percent belonged to Chinese producers.[12] The same estimates reveal that the Chinese industrial structure encompasses far more than the cells: The Chinese producer's ecosystem involves the various stages of the cathodes, anodes and materials processing that are the determinants of cost, quality and economies of scale, even if Europe manages to put together large numbers of electric vehicles. Moreover, according to the European Parliament's Research Service, relying on International Energy Agency supply-chain figures, China accounts for over 80 percent of global capacity to produce battery cells, close to 90 percent of capacity to produce cathode-active material and over 97 percent of capacity to produce anode-active material.[13] In short, what Europe is relying upon is not simply imported finished batteries, but a structure of production layers whose combination produces the same battery with far higher costs for all. That there is still a structural dependence is not simply because the Europeans have learned to build factories. EU battery-cell manufacturing capacity increased by 10 percent in 2024, although China still held about 85 percent of global capacity. [14]

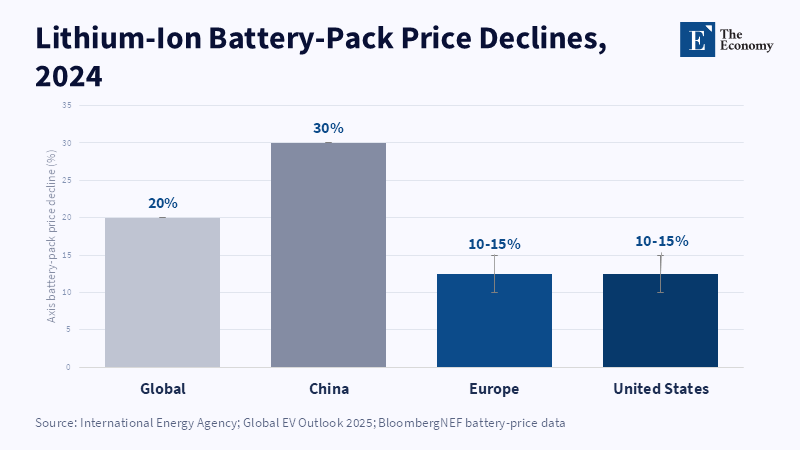

This represented progress, but the EV supply chain remained highly concentrated in raw materials and processing. What really makes the difference between a factory and an ecosystem is autonomy. In the absence of control over process learning or technology pathways, where those remain outside of Europe, an increased local scale of assembly or even battery manufacturing will not fully hedge against strategic risk. Cost remains a sizable portion of the explanation. In battery manufacturing, industrial independence cannot be maintained if local production remains persistently and substantially uncompetitive. According to a report of the European Parliamentary Research Service, Li-ion battery-pack prices fell by 10-15 percent in Europe in 2024, compared with nearly 30 percent in China.[15] The International Energy Agency outlook for 2025 shows that China's battery-pack prices remained roughly 35 percent lower than those in Europe, with the regional premium even larger than in 2022. Such a difference cannot be broken down to one policy distortion. The report of the Organization for Economic Co-operation and Development unveiled that systemic below-market borrowings constituted an especially significant type of subsidy support to China-based manufacturing companies and Chinese companies might have had variations in their subsidy regimes compared to their international counterparts.[16] The International Monetary Fund (IMF) also was of the same view and in its 2025 Article IV consultation stated that China's export expansion has been underpinned partly by the depreciation of the real exchange rate due to lower inflation than trading partners, while also sounding a warning that state-dominated industrial support had partly caused oversupply in some tradable industries.[17]

Europe’s battery challenge cannot be explained by exchange rates or subsidies alone. China’s advantage also reflects scale, industrial clustering, chemistry expertise, supplier density and financing conditions. Attributing Europe’s disadvantage to any single factor, the logic is far too oversimplified for good policies. The trend in chemistry toward lithium iron phosphate merely highlights the issue. The International Energy Agency reports that Korean firms, which have long been the largest single source of foreign investment in the continent's battery industry, lost a significant share of their EU market from nearly 80 percent in 2022 to 60 percent in 2024 due to the growing popularity of LFP chemistry,[18] in which Chinese companies have attained a very strong position. And this is relevant because the center of gravity of battery production is shifting. If Europe develops capacity based on chemistries, processes, or supply chains that are on the wane in terms of cost or performance, the gross capacity could grow, but strategic vulnerability would deepen. A plant based on imported knowledge in a chemistry that is mostly monopolized elsewhere is not independent insofar as it is physically within the EU. It may instead link Europe to the next round of growth by externally imposed parameters.

But even so, it would be wrong to write off overseas engagement in the industry as automatically inimical to European sovereignty. The IEA agency in the very same report stated that Chinese battery ventures in Europe could be an avenue of technology transfer, could provide the know-how necessary to ramp up manufacturing and could bring costs down for European car manufacturers at a crucial time.[19] This is a serious counterargument. Manufacturing on the ground by well-established Asian firms could trim logistics, create jobs, boost quality and start European workers and suppliers on better production methods. In a field of rapid learning curves and enormous sums of money, ruling out such investment on general principles might merely weaken the continent. But their argument is contingent on conditions that cannot be taken for granted. The same IEA analysis estimates that with committed projects, the market share in the EU by Chinese-owned manufacturers could rise from less than 10 percent in 2024 to over 30 percent by 2030, while EU-based companies held about 5 percent of capacity at the end of 2024,[20] and that figure is compromised by the ability of a handful of projects to fall into deep uncertainty.

If the ownership, technology decisions and know-how all remain concentrated under Chinese control and existing EU incumbents are frozen in place, a new EU battery industry could certainly end up producing a lot of local jobs and output without emerging as a truly free-standing, autonomous industrial ecosystem. Europe could end up with a green battery sector owned by corporations headquartered elsewhere and that is still valuable. It just can't be assumed to be equivalent to autonomous EU ownership. Formal presence and actual influence are two different things. Recent events are making this distinction harder to maintain. Northvolt, long billed as the standard-bearer of an indigenous European champion of the European battery industry, filed for bankruptcy in Sweden in March 2025,[21] having been unable to raise the funding to operate at its then-existing scale. The company attributed this to rising costs of capital, supply chain disruptions, shifting demand patterns and internal ramp-up issues.[22] As a consequence, battery expansion plans across Europe have become more conditional. Automotive Cells Company paused its German and Italian projects in 2024 and confirmed in February 2026 that both had been shelved, leaving its French plant as its only operating gigafactory.[23]

These three pieces of news may not prove that it is infeasible for Europe to supply a competitive battery industry. They can, however, be read to demonstrate that capacity announced, projects announced and resilient operating capacity are very different things and that infrastructure-driven industrial remains weaker than political stories would have you believe. The outcome is thus a dual reliance that exceeds the general literature on China-related risk. Europe relies on Chinese materials or components, or both, whenever it cannot produce them itself, whenever it cannot produce them without Chinese links (strong chemistry and process know-how based on externally controlled technology) and whenever it cannot produce them without weakly capitalized non-European investors. When does this strategically matter? When supplier-switching costs are high, as they are in the battery-cell (and most other) supply contracts. When the upstream line-up in high-grade graphite and lithium, cathodes and anodes, refined materials, constrains substitution despite pre-equipped cell plants in Europe. When the project pipeline suggests resilience, but the truly serious investment in the capabilities necessary for continuously low-cost production remains fragile. Any of those: localization, alone, is no battery sovereignty and no strategic autonomy.

3. Solar Photovoltaics: Deployment Strength, Manufacturing Weakness

The solar case is different from batteries, but equally instructive. Europe's reliance on Chinese solar fabrication is more evident in some respects, yet the strategic consequences are more complicated because the product characteristics, storage attributes and deployment economics are different. Eurostat reports that in 2024, the EU imported €11.1 billion worth of solar panels from non-EU sources and China made up 98 percent of those imports.[24] Solar has also been one of the drivers of Europe's decarbonization: as per the European Commission's solar energy page, the estimated EU solar capacity stood at 406 gigawatts in 2025, up from 338 gigawatts in 2024.[25] Cheap Chinese equipment has therefore helped facilitate a large chunk of the EU's energy transition while at the same time exacerbating industrial reliance. It is for this reason that sharp dichotomies, either calling for complete openness or blanket protection, are unpersuasive. The same source of imports that causes acute industrial fragility also facilitates quick decarbonization at scale. The roots of this dependency stem from a longer history of industrial transition. The International Energy Agency’s special report on solar photovoltaic supply chains determined that the size of global manufacturing capacity shifted from Europe, Japan and the US to China and that China additionally invested more than $50 billion in new photovoltaic supply capacity-ten times as much as Europe-for hundreds of thousands of manufacturing jobs over the decade leading up to the early 2020s.

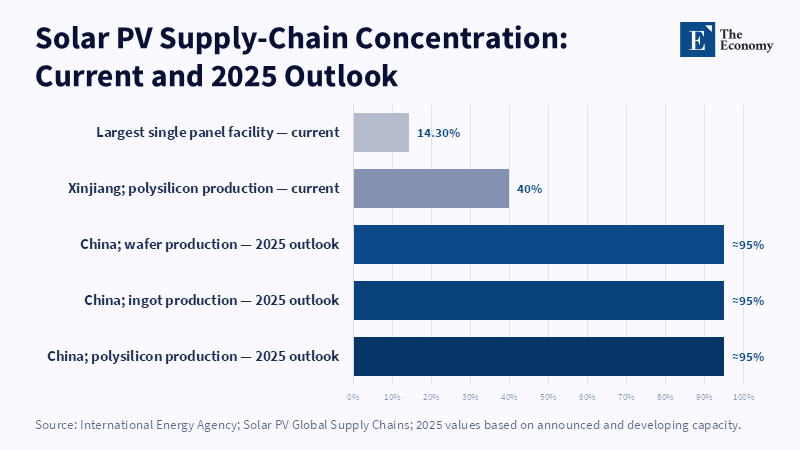

At that point, China’s share in all the major manufacturing segments-including polysilicon and ingots, wafers, cells and modules- accounted for more than 80 percent and the country housed 10 of the world’s biggest suppliers of solar manufacturing equipment.[26] Such a transition was driven by more than low wages or subsidies; it was characterized by integrated stepping across the entire supply chain, lower capital and energy costs, fast equipment learning, deep supplier networks and a large domestic market that could sustain multiple iterations of process-scale optimization. Europe's challenge in solar, then, is not merely that it imports finished products, but rather that most of the industrial capabilities that would be needed to re-establish the chain are embedded in a manufacturing system that is extremely difficult to reproduce or transplant in pieces. The European discussion regularly centers on modules because they are the items that are installed, traded and legislated upon. However, the real pinch points exist further up the supply chain. According to the 2024 Energy Technology Perspectives from the IEA, the EU's domestic production of solar modules only just exceeded 15 percent of demand in 2023.[27] Far more instructive are the current capacity distributions within Europe.

According to the IEA Photovoltaic Power Systems Program, the 2026 profile of the European Union reports about 12 GW of photovoltaic-module manufacturing capacity within the EU, about 2 GW of cell capacity, at least 25 GW of polysilicon and less than 1 GW of ingot and wafer capacity.[28] On the other hand, inverter manufacturing seems to be holding at least a significant share of the market at more than 121 GW AC. Whether, of course, inverter manufacturing can maintain this share in the face of increasingly serious competitive pressure remains to be seen. This composition is revealing. It indicates that while Europe holds isolated technically competent regions of the solar value chain, namely inverters, engineering and other higher-value processes. Also, it has a serious deficiency in the stages that would allow for the replication of module manufacturing at scale without reliance on inputs from outside the EU. A region with module lines but little cell or wafer capacity would be predominantly downstream. Therefore, the 98 percent import figure does not necessarily reflect the actual PV exposure. Moreover, even if Europe responds by boosting domestic module production, the resilience would still be limited if more advanced wafers, cells and production infrastructure remained heavily reliant on external trade.

It is precisely this challenge which the Commission's European Solar Charter acknowledges, observing a high degree of dependence on few sources, China accounting for most of PV module import and stating that decreasing import prices risks European competitiveness while threatening planned investments; the Charter's conclusion is on the mark: the whole industrial-mineral threat is not driven by a one-year high import concentration, but by the ongoing degradation of domestic manufacturing options.[29] Once firms are packed up and shipped elsewhere, competitors' line equipment moves within the industry, workers exit and bankable order books are empty, the cost of rebuilding capacity is much higher. Strategic risk is not a matter of cheap imports creating a price shock, but of cheap imports whose price falls so low that they are the mechanism through which the domestic dream of a final collapse becomes reality. That does not mean that every issue of photovoltaic dependence should be securitized. Solar modules are not similar to rare-earth magnets or critical medicines. They can be stockpiled more easily than other elements and do not necessarily prevent the market introduction of all existing capacity at once. Still, Chinese manufacturing dominance has also allowed the emergence of a considerable welfare gain for Europe, thanks to lower module prices and thus enhanced renewable accelerations.

A policy that substantially raises module prices everywhere would transfer costs to households, project developers, public budgets, electrification commitments and the investment and operating decisions of national energy systems. To all evidence, concentrated trade may be efficient rather than strategically dangerous in the short run. The trick is to identify where efficiency ends and the risk of industry lock-ins begins. This threshold is crossed when three factors come together. One is the concentration of technology across a number of upstream steps rather than just in the end product. The second is the weakening of domestic learning and project finance to the extent that Europe is unable to do a credible re-entry in a timeframe relevant to the transition. And the third is the increasing centrality of the imported technology to the problem of system planning, whereby industrial bargaining power impacts the pace and nature of the transition. By these tests, photovoltaics are now a practical question of material industrial sovereignty-though not a basis for unselective disengagement-by forming a deeply entrenched production ecosystem in China. Its expansion in Europe is thereby built on a production ecosystem and by raising the scale of deployment, can perversely deepen that production ecosystem.

It would therefore be a selective, less maximalist, form of autonomy. Europe need not produce all solar components here, nor exclude all Chinese participation in the future. But it would need to avoid the policy equilibrium whereby each additional MW built deepens the deficiency in Europe's cell and wafer capacity. Still-present European lead on inverter design and parts of the broader engineering ecosystem is politically and industrially useful; it indicates the policy focus should not be on accomplishing the entire chain at once, but achieving enough upstream and enabling capacity to make Europe's deployment less dependent on one dominant foreign system. That is a narrower, more pragmatic sense of autonomy than self-sufficiency, but a compelling one, more robust than the market share that installations normally entail.

4. Electronics and Digital Infrastructure: Dependence Beyond Final Assembly

The broader electronics sector makes the analysis more varied and intricate. In this case, the pattern of dependence on China is dense, but not all of it is centered on China in the same manner. Eurostat indicates that for 2024, the European Union imported high-tech products to the tune of €478 billion from non-bloc countries, of which €141 billion was imported from China.[30] China was the European Union's leading partner in high-tech imports and the most important partner for electronics-telecommunications, computers, office machinery and electrical machinery products. Eurostat also states that the EU's high-tech trade deficit with China stood at €92 billion in 2024[31] and that high technology products witnessed an especially high trade deficit with China in the case of computers, office machinery and electronics-telecommunications. Such figures show a large and persisting external dependence on technologically sophisticated goods. However, these bare numbers do not, by themselves, tell us the nature of strategic risk they represent-this requires a turn away from total trade figures in broad categories to the underlying production and substitution architecture. Carnegie's 2026 analysis is therefore just as useful precisely because it turns that corner. Within the top ten high-dependence imports of the EU as a whole, it singles out computers, smartphones, data-storage equipment, microprocessors, network-control hardware, photovoltaic cells and lithium-ion batteries.

For the indicators most relevant here, the analysis estimates that in 2024, 54.5 percent of EU computer imports and 40.7 percent of EU smartphone imports came from China.[32] But the same analysis also calculates large intra-EU shares for those sectors, implying that some Chinese-connected products and inputs may already be counted somewhere in European trade flows. This makes direct import share the opposite of measured dependency; the simplest definition of the latter-any shipment crossing a customs border is, from a dependency perspective, a candidate of origin-will tend to undercount, not overcount, dependency. A gadget recorded as European may, like a vehicle declared in the final minute to be "European," still be heavily dependent on Chinese-origin parts and subassemblies, contract manufacturing, or supplier ecosystems. The relevant industrial unit is not the final entry at customs; it is the chain of suppliers, tooling, software and intermediate parts that go into the finished product. The European Commission's 2024 economic brief on EU-China exposure supports this observation. The brief contends that many of the EU's strategic dependencies on China are, in fact, also global single points of failure, making this point with 13 examples, including photovoltaic cells, laptops and smartphones and demonstrates it with trade-in-value-added data on China's intermediate inputs within EU manufacturing, shown to be particularly significant for electronics and electrical equipment.[33] This differentiation is significant for industrial policy.

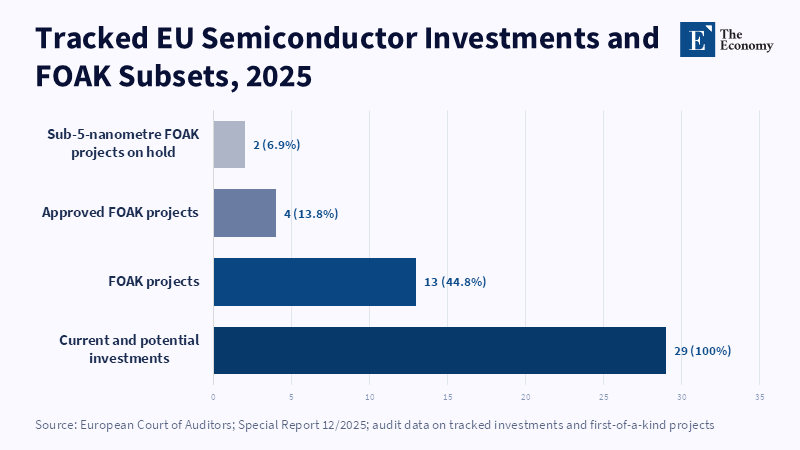

Admittedly, at the same time, the electronics chapter cannot be broadly put as a China-centered problem. Semiconductors are the best example: the European Court of Auditors found in 2025 that the European Chips Act was a very unlikely candidate to attain its headline target of a 20 percent share of world cutting-edge and sustainable production by 2030: in fact, the EU's share was expected to be only 11.7 percent.[34] The same audit reflects that in 2020, the only firms producing at 5 nanometres were situated in Taiwan and South Korea, while the EU had no fabrication at or below 22 nanometres.[35] Semiconductor vulnerability, therefore, has a different geographical profile from reliance on laptops and cellphones. China matters in downstream assembly, mature-node capability and some materials and packaging tiers, but at least the frontier semiconductor weakness is a Taiwan-Korea-United States issue as well as a China-centered issue. That is analytically significant because it constrains what can be fixed through an exclusively China-focused de-risking agenda. However, this wider geography does not diminish the relevance of China to Europe's digital infrastructure. It alters the mechanism. In consumer electronics, telecom equipment and many other consumer electronics categories, China's position is about the density of its manufacturing ecosystems, about the number of its assembly and component networks, about the speed of its lead firms' sourcing, their redesign and their launching into mass production.

Europe's reliance on computers and smartphones, therefore, is not simply a question of import values. It is rooted in ecosystem effects: clustering of components, logistics costs, tooling, testing, repair, independent sourcing of replacements with short wait times. When those capabilities are highly concentrated, the geography of assembly can be used for leverage even if the other inputs are globally diverse. All of which matters more than traditional trade data have indicated because the emerging digital and green offsets are converging on hardware electronics more and more. Power electronics, data processing units, sensors, control systems and specialized communications equipment are embedded in EVs, battery-management systems, industrial automation, grid hardware and renewables. The Commission's China trade page cues further escalation of Chinese export controls on key raw materials and some technologies and links them to European supply chain pressures.[36] Its industrial logic is obvious. Even if Europe needs nothing from China in every cutting-edge component and piece of equipment, the widening of China-related hardware and input exposure throughout many industries means an electronics bottleneck could emerge in one corner of the supply chain, bringing knock-on effects in the net-zero economy's manufacturing base elsewhere. The predicament, therefore, cannot be kept in consumer goods terms.

But here too, a strong counter-argument must be given. The Commission's economic brief finds that services and software are far less exposed to China than manufacturing hardware, with only a few exceptions.[37] Europe also still has significant expertise in semiconductor equipment, analog and power electronics, industrial automation and in some engineering-driven specializations. The problem, therefore, is not that Europe has no relevant digital capabilities, but rather that the global supply chains that connect these to broad-based hardware manufacturing are overly dependent on outside factors. If policies approach high-end innovation as synonymous with system resilience, the core problem will be missed. Digital sovereignty is only impractical if Europe is distinct from any advanced digital industry, but too few of Europe's digital capabilities are anchored or aggregated within accessible, scalable ecosystems in Europe.

5. The Domestic-Capacity Illusion

"Domestic capacity" conceals more than it reveals unless the nature of power that creates it is clarified. On the current terrain, the domestic capacity illusion has four faces: ownership, technological sovereignty, upstream control and implementation credibility. Each has a field of evidence; the strongest potential for producing the illusion, however, is in the simultaneous projection of all four into a single political frame of the success of reshoring. A battery or solar plant may be located in Europe, employing European workers, with European public subsidies, without changing the foreign chemistries on which it depends, the intermediate inputs it imports, the production tooling it adopts offshore, or the decisions it takes elsewhere. In that instance, Europe may gain local activity without gaining resilience. The greatest overt discrepancy is ownership. Battery production ownership is unquestionably dominated by Korean producers, who held an estimated 85 percent of the EU market in 2024,[38] according to the International Energy Agency. This share could further decrease as Chinese investment grows (to the largest estimated producer, South Korea) and large EU-based firms emerge (to around 20 percent). Again, even with the full achievement of announced plans, ownership would remain apolitical.

There is no need to cast aspersions on non-European ownership; knowledge-intensive manufacturing alone can generate employment, cost savings, supplier adjacencies and market fluctuations. But at the policy level, a plant owned, say, by a non-European producer conveys markedly different signals from one owned by a European controlling firm with Europe-based R&D, procurement and production systems. Technological upgrades, new model generations, offsetting profit sharing, or the tending-to-oversight of crisis all involve politicized geographic decisions. Industrial location alone provides an insufficient indication of strategic oversight. The second gap is technological competence. The International Energy Agency is explicit on this point, stating that Chinese investment can provide a channel for technology sharing with Europe.[39] This is by no means assured. But even in principle, technology transfer, even when agreed or formally supported, is not the same thing as automatic, complete or politically neutral. The real issue is not merely machinery crossing a border. The issue is whether Europe penetrates the tacit knowledge of production, process engineering know-how, key supplier relationships and the design authority that would enable autonomous reproduction and upgrading. The December 2024 Stellantis-CATL case provides an instructive example. The announced Zaragoza joint venture would add up to 50GWh of annual LFP capacity, on the basis of CATL's LFP batteries using CATL technology. [40]

Likewise, in January 2025, the Commission approved €48 million euros of French state aid for the Envision AESC France battery plant in Douai.[41] Both cases are ultimately successful with policy, but both expand European production in the knowledge and firm control of its foreign partners. Without tight conditions to foster skills transfer, supplier engagement and innovation anchoring, such investment may raise European output and leave open its technological independence. A third gap concerns upstream inputs. Solar manufacturing represents the clearest example. Europe is capable of providing modules and even some inverter capacity, yet for wafers and cells it still has no significant domestic manufacturing capacity. The 2026 report from the International Energy Agency Photovoltaic Power Systems Program on the European Union reveals only modest upstream capacity in ingots, wafers, cells and polysilicon.[42] And while offering equal promise for cell and pack manufacturing, an advanced chemistry cell manufacturing within Europe would nonetheless fail to relocate upstream manufacturing chokepoints if cathode active material, anode active material, separators, electrolytes and refined commodities stayed remanufactured outside the EU. Transnational factories, in these conditions, do in fact make a difference in just a small way by reducing the fragility of the supply chain, but do little to cross the fundamental boundaries of scarcity.

Implementation credibility is the fourth gap and what the recent past can teach us about why it exists. Announced gigafactories, projections of gigawatt-hours and pre-electrification political agreements have long been used to describe the region's pipeline of batteries. However, announced capacity does not equate with bankable, operational and cost-competitive production. Northvolt's filing for bankruptcy in March 2025 highlights how even sophisticated indigenous projects can fail[43] under the pressures of good financing, execution and demand. The suspension of construction of cell plants by Automotive Cells Company in Germany and Italy, followed by the de facto cancellation of these projects,[44] provides a second cautionary tale: plans for local capacity are extremely sensitive to changes in vehicle demand, chemistry economics and capital discipline. The European Court of Auditors has also made a similar statement regarding the raw materials sphere, arguing that EU efforts to diversify have often failed to translate into practical results because progress was not measured consistently and several schemes did not result in reliable supplies.[45] A similar phenomenon is likely to be at play in the broader industrial context: a measure of autonomy based on press releases will consistently exaggerate the region's true resilience.

There is no reason to retreat to autarkic reflexes, however. There is a real risk in taking the argument too far. Foreign investment can often generate learning opportunities that a Europe short on capital would be otherwise unable to generate. It can expand the tax base, help an embedded supplier network and give Union firms access to market segments-such as the low-cost LFP batteries-in which Europe has been relatively weak. And it may prove to be the fastest route into scaling the kind of productive experience that is critical to many of the industries for which strategic relevance is so important. A European policy that simply denies Chinese or broader Asian entry-one that limits the industrial scale Europe can have-is fairly sure to slow deployments, increase costs and weaken Europe's industrial base at a crucial juncture. The domestic-capacity illusion should thus not be interpreted as being opposed to localization or to foreign investment. It is a call for accuracy. EU production enhances resilience only insofar as it increases one or more of the following: who has the process know-how, where key inputs are made and bought, which firms learn how to run the process, how fast the continent can switch suppliers, how safe investments are when markets undergo stress. If those variables do not change, running more of the production process in Europe may be technically true, but it does not constitute green-digital independence. The issue is not whether Europe produces more. The issue is whether more manufacturing would make Europe less vulnerable when the supply chain is put to the test.

6. Policy Options: From Localization to Operational Control

A robust European reply will need to be selective, operationally targeted and explicitly control-focused. The first prerequisite is improved transparency on dependencies below the threshold of gross imports. The European Court of Auditors has criticized the Commission for a lack of granular trade data and for ignoring the implications of funding on supply security for critical raw materials technologies.[46] The Commission has already taken some steps in the right direction with respect to net-zero technologies: by issuing a 2025 guidance paper on trade flows and strategic dependencies for technologies used in parts of batteries, photovoltaics and electronics. Battery regulation is now moving to promote traceability and transparency at the product level: through carbon-footprint transparency, supply chain compliance standards and a battery passport.[47] These tools should now be integrated within a sector-by-sector monitoring toolkit for batteries, photovoltaics and semiconductors/electronics. Besides import share, what should also be monitored is ownership, use, licensing, production status, qualification constraints and upstream concentrations (e.g., in cathodes, anodes, wafers and inverters). The objective is not to generate another socio-economic vulnerability index, but rather to deliver to the industrial ministers, the European Commission and firms a lingua franca to pinpoint the residual external nodes on which appears to still depend most of the European capacity.

The second condition is conditionality. Public support should meet stricter conditions. The Clean Industrial Deal offers over €100 billion to reach the EU's very-high-efficiency manufacturing. In December 2024, the Innovation Fund opened a €1 billion call to support electric-vehicle battery-cell manufacturing.[48] The Commission green-lighted targeted state aid, such as the 48 million French package for Envision AESC. All that support is not flawed in itself. The issue is whether it signals or subsidizes activity but not control. To be effective, public funding must be released in phases and made conditional on results that are beneficial to resilience: localizing key intermediate inputs where feasible, training and retaining European process engineers, publishing transparent supplier development plans, reaching specific thresholds of R&D or pilot-line activity within the Union, developing credible contingency plans to ensure emergency supply. For projects in which imported technology plays a crucial role, conditionalities should include concrete plans for upskilling and supplier localization, rather than unsupported assumptions that spillovers happen spontaneously. Such conditions do not have to correspond to the Chinese localization requirements or to masked protectionism. They can take the form of performance conditions associated with subsidizing industries, which is expensive precisely because Europe aims to establish public resilience, rather than business resilience.

Third, Europe should utilize demand-side measures more intelligently than it has so far. The aforementioned Net Zero Industry Act now calls for the inclusion of resilience and other non-price criteria when awarding public procurement contracts or conducting auctions for renewable-energy sources. Such criteria are a requirement for at least 30 percent of the volume that is auctioned off annually in each member state or 6 GW, whichever is lower and where a net-zero technology is heavily reliant on a single third country.[49] This is a major step change. If meticulously implemented, it could help the EU create order book confidence for strategic areas without uniform import bans, which would be excessively costly both fiscally and for consumers. The trick will be in exercising selectivity. Demand-side preference should not be arbitrarily extended to every tile in a solar panel portfolio, every battery that is bought, or every category of electronics, owing to the high fiscal and consumer costs in general and to the industrial sector in particular; it should rather be targeted toward segments where Europe can reasonably expect to scale up its own production and where one further industrial flight would be especially painful: the active electrode material of batteries, batteries cells for strategic segments, photovoltaic cells and wafers and specific kinds of electronics and grid infrastructure. Resilience criteria should also contemplate diversified allied sourcing, not just island economies of steel and computer chips. Strategic independence in this sense does not imply striving for institutional territorial self-sufficiency.

Fourth, the battery and solar agendas require a more coherent strengthening of the raw materials policy, but without overplaying what raw materials diplomacy can deliver today. The Critical Raw Materials Act set a 2030 target; the Commission identified 47 strategic projects across the EU in March 2025 and 13 outside the EU in June 2025.[50] Nonetheless, the European Court of Auditors ascertained in 2026 that import diversification efforts had yet to bear fruit, the Commission had "not demonstrated that it is effectively following up on the supply-side impact of strategic partnerships," and "domestic developments are still hamstrung by financial, legal and administrative bottlenecks". This should slow the expectations down. Partnerships with Canada, Australia, Chile, Morocco, or other trusted suppliers are no substitute for domestic industrial policy and bilateral memoranda of understanding are no guarantee of secured supply. The logical course is to move from a diplomacy-driven to a projects-driven approach, signing offtake agreements, offering offtakers public guarantees, jointly financing refining and processing infrastructure and explicit backing for recycling in Europe to lessen future import dependency. On inputs for batteries especially, that means leveraging fewer projects into robust operational supply chains, with whose offtakers are situated in Europe and how much processing capacity.

Fifth, policy should give more emphasis to the enabling layers, where Europe still has comparative advantages and where the largest sectoral spillovers are to be found. In solar, Europe still has advantages in inverters, engineering and certain machinery. In semiconductors, it has a historical basis in equipment and selected industrial niches more than in leading-edge fabrication. In batteries, there is greater scope for recycling, process engineering, materials science and some industrial machinery than for trying to emulate the entire East Asian ecosystem of manufacture immediately. The Clean Industrial Deal and the European Solar Charter already reflect the importance of research, innovation and manufacturing support. What has not yet emerged is sufficient coherence between these comparative advantages and policies for procurement, financing and scale-up. Europe should promote pilot lines, manufacturers of production machinery and certification infrastructure as enthusiastically as it supports final-product assembly. Keeping control over enabling process machines and know-how is better leverage for bargaining over foreign investment and to effectively reconfigure supply if circumstances deteriorate. Losing those layers leaves the continent dependent even if final assembly remains domestic.

Sixth, trade defense should still be available but should be disciplined by industrial purpose, not by symbolism. The 2024 commission battery-electric-vehicle case set a precedent that where unfair subsidization is proven, the Union is willing to deploy countervailing duties and that is right. Trade defense is a limited tool; it can hinder surges of imports and it might give the Union extra negotiating leverage. But, by itself, it cannot establish a competitive European supply chain. Overuse can also increase input prices for European suppliers, hinder climate deployment and provoke reprisals, none of which would address capability deficiencies. In the sectors surveyed here, the appropriate employment of trade instruments therefore is conditional, reversible, targeted to proven distortions, coordinated with subsidy and procurement policies and periodically analyzed with regard to industrial results. Europe must avoid the trap of general protectionism and stagnant notions of autonomy in favor of strategically targeted trade action. This does not imply total decoupling, but instead the beginning of an industrially driven selective de-risking strategy.

Lastly, Europe needs to restrain its own rhetoric. It is not helpful to offer strategic autonomy for areas where avoiding pain requires risk management for a decade or more. Nor is it advisable to warn of every Chinese-linked supply chain as an imminent coercive threat. While the Commission's trade page is correct in warning of distortive industries and a hit to EU supply chains from export controls, the likelihood, nature and timing of any disruption differ from sector to sector. Policy credibility can only be enhanced by the Union stating explicitly what it is aiming to protect in each field: a self-maintaining industry for cells and active materials in batteries; upstream capacity to avert total lock-in for solar; improved capabilities to see Chinese inputs in electronics and developed hardware to leverage European capabilities. Once those objectives are concrete, policy tools will be assessed by whether they eliminate specific chokepoints instead of relying on (mere) assertions of sovereignty.

7. Conclusion - Building Capacity Europe Can Sustain

The real distinction is not at the stage of production in Europe, but in exercising the power to shape the conditions under which Europe has the capacity to sustain production. In batteries, photovoltaics and strategic electronics, the EU has gone beyond merely being subject to external influences and begun to construct policy instruments, factories and financing mechanisms. However, much of this risk acceleration will still be subject to a simple methodological mistake: conflating geographic source with strategic independence. The evidence suggests that this would be a far more rigorous conclusion: self-determination in the green-digital economy depends on having full command of upstream inputs, process technology, upstream manufacturing stages and a credible operational capacity to endure stress. Where those are not in the hands of the EU, domestic capacity can be valuable, but it is not resilient. This is not a justification for sweeping decoupling. Chinese imports and investments have also brought down costs, hastened deployment and, in some cases, enabled Europe to scale up faster. The policy dilemma involves selective de-risking not the opposite extreme. Public finance should secure the outcomes needed for control, procurement incentives should favor resilience where concentrations are most crucial and international partnerships should align on actual supply rather than formal declarations. Without those lines of distinction, Europe will continue to industrialize under someone else's conditions, whereas with them spelled out and implemented, there is still a credible and disciplined industrial strategy for green-digital autonomy.

References

[1, 24] Eurostat (2025a) International Trade in Products Related to Green Energy. Eurostat News. Luxembourg: Eurostat.

[2, 30, 31] Eurostat (2025b) EU High-Tech Trade Back to a Surplus in 2024. Eurostat News. Luxembourg: Eurostat.

[3] Eurostat (2026) EU Trade with China—Latest Developments. Statistics Explained. Luxembourg: Eurostat.

[4, 5, 10, 32] Ülgen, S. (2026) From Trade Dependence to Geopolitical Leverage: The EU in an Era of Weaponized Interdependence. Washington, DC: Carnegie Endowment for International Peace.

[6, 49] European Parliament and Council of the European Union (2024a) Regulation (EU) 2024/1735 of 13 June 2024 on Establishing a Framework of Measures for Strengthening Europe’s Net-Zero Technology Manufacturing Ecosystem and Amending Regulation (EU) 2018/1724. Official Journal of the European Union.

[7] European Commission (2025a) The Clean Industrial Deal: A Joint Roadmap for Competitiveness and Decarbonisation. COM(2025) 85 final. Brussels: European Commission.

[8, 48] European Commission (2024a) Commission Launches €4.6 Billion of Innovation Fund Calls to Boost Deployment of Net-Zero Technologies, Electric-Vehicle Battery Manufacturing and Renewable Hydrogen. Brussels: European Commission.

[9] European Commission (2024b) Commission Implementing Regulation (EU) 2024/2754 of 29 October 2024 Imposing a Definitive Countervailing Duty on Imports of New Battery Electric Vehicles Designed for the Transport of Persons Originating in the People’s Republic of China. Official Journal of the European Union.

[11, 12, 13, 14, 15, 18, 19, 20, 38, 39] International Energy Agency (2025) Global EV Outlook 2025: Expanding Sales in Diverse Markets. Paris: International Energy Agency.

[16] Organisation for Economic Co-operation and Development (2026) Manufacturing Groups and Industrial Corporations (MAGIC) Database. Paris: OECD.

[17] International Monetary Fund (2025) People’s Republic of China: Staff Concluding Statement of the 2025 Article IV Mission. Washington, DC: International Monetary Fund.

[21, 22, 43] Northvolt (2025) Northvolt Files for Bankruptcy in Sweden. 12 March. Stockholm: Northvolt.

[23, 44] Reuters (2026a) Stellantis-Backed ACC Drops Plans for Italian and German Gigafactories, Union Says. 7 February. Reuters.

[25] European Commission (2026a) Solar Energy. Directorate-General for Energy. Brussels: European Commission.

[26] International Energy Agency (2022) Solar PV Global Supply Chains: An IEA Special Report. Paris: International Energy Agency.

[27] International Energy Agency (2024) Energy Technology Perspectives 2024. Paris: International Energy Agency.

[28, 42] International Energy Agency Photovoltaic Power Systems Programme (2025) Trends in Photovoltaic Applications 2025. Paris: IEA PVPS.

[29] European Commission (2024c) European Solar Charter. Directorate-General for Energy. Brussels: European Commission.

[33, 37] Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An Enhanced Methodology to Monitor the EU’s Strategic Dependencies and Vulnerabilities. Brussels: European Commission.

[34, 35] European Court of Auditors (2025) The EU’s Strategy for Microchips: Reasonable Progress in Its Implementation, but the Chips Act Is Very Unlikely to Be Sufficient to Reach the Overly Ambitious Digital Decade Target. Special Report 12/2025. Luxembourg: European Court of Auditors.

[36] European Commission (2026b) China: EU Trade Relations with China—Facts, Figures and Latest Developments. Directorate-General for Trade and Economic Security. Brussels: European Commission.

[40] Stellantis and CATL (2024) Stellantis and CATL to Invest Up to €4.1 Billion in Joint Venture for Large-Scale LFP Battery Plant in Spain. 10 December. Amsterdam: Stellantis.

[41] European Commission (2025b) State Aid: Commission Approves €48 Million French Measure to Support Envision AESC France’s Battery Plant in Douai. Brussels: European Commission.

[45, 46] Reuters (2026b) EU Efforts to Diversify Critical Raw-Material Imports Fail So Far, Auditors Say. 2 February. Reuters.

[47] European Parliament and Council of the European Union (2023) Regulation (EU) 2023/1542 of 12 July 2023 Concerning Batteries and Waste Batteries, Amending Directive 2008/98/EC and Regulation (EU) 2019/1020 and Repealing Directive 2006/66/EC. Official Journal of the European Union.

[50] European Commission (2025c) Commission Selects Strategic Projects to Secure and Diversify Access to Critical Raw Materials in the European Union and Third Countries. Brussels: European Commission.