[EU vs. China] When Supply Chains Become Statecraft: China and the Geopolitics of EU Strategic Autonomy

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

Debates about dependence on China often rely on headline trade values, yet strategic vulnerability is by definition less broad, based around a tighter group of system enablers. To help rationalize the policy choice between decoupling and dependence, the paper develops an analytical framework for distinguishing economic exposure, disruptive capacity, coercive use and political intent and applies it to Chinese positions in critical materials, processing of rare-earth, permanent magnets and certain industrial intermediates. It contends that supply chains have become statecraft instruments when material production is strongly concentrated, downstream substitution lags and licensing or export controls can transfer minor upstream disruptions to large European manufacturing industries. Defining a zone of dependence where supply-chain importance overlaps with political distance, the paper juxtaposes China-linked industrial vulnerability to Europe's accelerating energy dependence on the United States. The best policy is neither autarky nor large-scale decoupling but a nuanced approach of de-risking through detailed monitoring, economically viable alternative providers, strategic stockpiling, crisis simulation and coordinated trade and investment actions. Strategic independence depends on diminishing concentrated leverage without losing the advantages of economic dynamism.

1. Introduction - From Trade Exposure to Geopolitical Leverage

The European debate about dependency on China tends to focus on the wrong level of abstraction, shifting between headline trade values and excessive strategic alarmism and between the language of openness and the assumption that interdependence must be stabilizing. Neither of those shifts makes sense. Simply talking about a high value of imports does not automatically define a strategic problem; many big flows are merely economically significant but not politically dangerous. Simply asking "How can ordinary trade relationships threaten European decision-making?" is more analytically demanding. But it has not been possible to ignore that question from about 2023 to 2026 precisely because several strategically significant chokepoints became more visible just as the EU started shifting from abstract anxiety about “strategic dependencies” toward a new and flesh-and-blood economic security machinery. The key thesis articulated here is that the EU's China problem is not generalized vulnerability through reliance on imports per se but selective exposure to system-enabling inputs whose degree of strategic significance is greater than their customs value.

A supply chain is statecraft when four factors align: production or processing is concentrated in a single supplier or jurisdiction; the input is functionally critical to downstream ecosystems essential to growth, energy transition, digital architecture or defence; substitution takes years, since certification, tooling, chemistry or process knowledge cannot be rearranged without delay; and political relations are distant enough that the risk of coercive use, if not a certainty, must factor into policy decision-making. China is not exceptional because its shares are so big; China is distinctive because magnitude, processing dominance, policy capacity and strategic competition increasingly coincide along a handful of key rare earths, magnets, high-value downstream components and industrial intermediates. This concentrated exposure appears neither hypothetical nor expansive, but sectorally selective, temporally flexible and geopolitically contingent. That is what makes the actual policy challenge not autarky, broad decoupling or rhetoric-laden “strategic autonomy”, but targeted de-risking focused on the concrete dynamics through which leverage could be wielded. This argument has become more important because the surrounding policy conditions have changed rapidly. The EU's economic security strategy, published in 2023 and subsequently developed through measures adopted in 2024 and 2026, explicitly frames the weaponization of dependencies as a policy risk, as a practical rather than merely theoretical risk.[1] China has, in 2023 and between late 2023 and 2025, respectively, introduced or tightened controls on exports of gallium and germanium; graphite; antimony; and rare earth elements, with associated technology controls in 2025. China also continues to be the EU's single most important supplier of imports.[2,3]

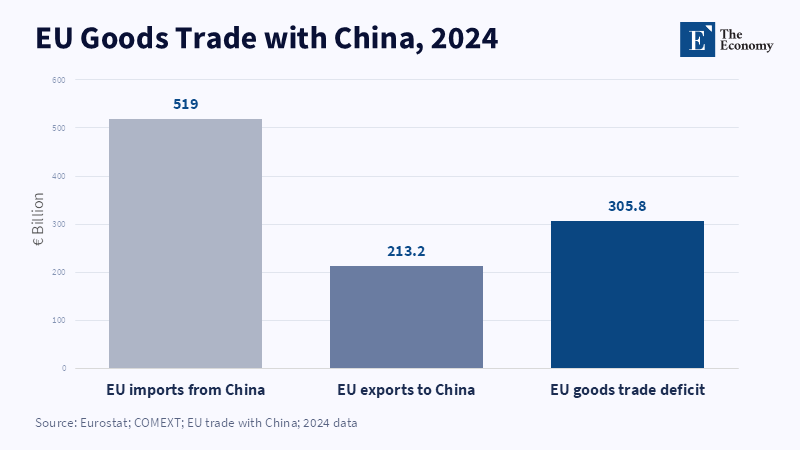

In 2024, the EU imported approximately € 519.0 billion of goods from China and exported €213.2 billion, producing a goods trade deficit of about €305.8 billion. Those numbers do not establish leverage. They are, however, an indicator of the scope of the relationship in which the more precise choke points operate. The strategic importance does not rest in the headline bilateral deficit, but in the prospect that a narrow set of hard-to-substitute upstream inputs can transmit disruption into far broader downstream industries during periods of political tension.[4] Another analytical distinction is necessary. Economic exposure, the capability for disruption, demonstrated coercion and political intent are distinct. Exposure is a structural reality of trade and production. Capability is the supplier’s capacity to impose shortages, delays or adjustment costs. Coercion takes the form of an effort to force political or regulatory change. Intent is the likelihood that a given willingness would be translated into a pressure attempt in given circumstances. Confusing these four stages leads to either serious misperceptions of the threat, exaggerated alarmism or complacent confidence that trade will defuse political conflict, or both. For the EU, the critical question is to determine in which areas China has a plausible capacity to undermine system-critical supply chains, in which domains it behaves and shows patterns of political alignment in a way that makes it less of a pure hypothetical and in which domains the costs of relieving exposure, now, would be less than the future costs of ignoring it and the resulting potential leverage. The rest of the argument is built on that narrower and more policy-relevant foundation.

2. Capability: Chinese-Controlled Bottlenecks and Downstream EU Disruption

Strategic vulnerability starts neither with imports as such nor with bilateral deficits.[5] It starts with bottlenecks. Those can be upstream goods that are small in monetary value, invisible in any public discussion of economic security and tiny in the final product, yet inescapable in production. Recent research by the European Central Bank on foreign critical inputs is illuminating. It defines inputs that European firms cannot readily produce in-house and that are critical where substitution is hard, where they are high-tech, or where they are involved in the transition to green energy as “foreign critical inputs”. Its measure indicates that in 2022, 17 percent of extra-EU imports were foreign critical inputs and China alone supplied roughly one-third of the EU's extra-EU critical input imports. A model of a 50 percent short-term disruption of supplies from China-linked economies showed manufacturing value-added losses of about 2 to 3 percent across five euro-area economies and more precise sectoral effects for electronic equipment, chemicals, basic metals, electronics and machinery. This result does not suggest that every Chinese input is strategically perilous. It suggests that EU vulnerability is greatest where foreign inputs are hard to substitute in the short term and they form part of a production system that has little cushion.

What renders an input system enabling is not simply its rareness, still less geopolitical drama. It is the way wider production networks turn upstream scarcity into downstream interruption. Rare earths are a case in point. Their direct cost component in a significant share of industrial products is low, but their role in permanent magnet materials and also in electric vehicles, wind turbines, industrial motors, data centers, aerospace and defense production, is significant.[6] This is an important corrective to simplistic import share politics. The degree of strategic peril in a European-imported product is not necessarily closely related to the headline import share of that product.

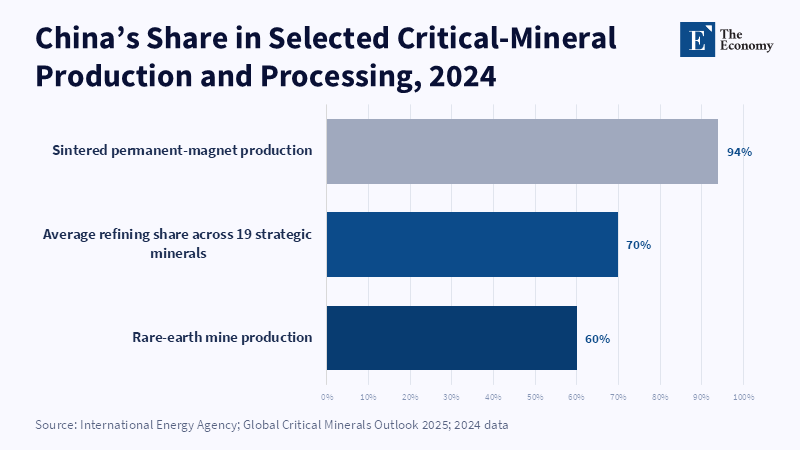

Its peril lies in one or more of the following conditions: concentration at a heavily processed supply-chain stage, heavy dependence upon the single surviving European producer, or greater economy-wide vulnerability to redesign around that import source over operational-cycle time horizons. By 2025 and 2026, several clear indicators showed exactly this kind of focused capacity. The International Energy Agency has indicated that China was the largest refiner in 19 of 20 strategically important raw materials, with an average market share of about 70 percent.[7] In 2024, China accounted for approximately 60 percent of global rare-earth mine production and about 94 percent[8] of sintered permanent-magnet production. Those market shares create substantial, though not unlimited, leverage. But operational licensing problems, technical expertise, administrative regulations, technology transfer limitations, or an export review procedure can have a far greater impact than the product market. This is extremely relevant for the EU because, especially, downstream production and system integration manufacturing are structurally stronger in the European Union than in upstream mineral extraction and midstream processing. The essential problem is thus no longer the import volume; it is the interruption of the flow. The same logic also applies to other critical raw materials.

A report published by the Organization for Economic Co-operation and Development shows that the share of export restrictions on critical raw materials reached a new high in 2024, with cobalt, manganese, graphite and rare earths as the most exposed; 16 percent of the trade of OECD-monitored critical raw materials was under at least one export restriction in 2024. China's importance in these markets is not the same for all minerals but is concentrated at similar processing stages, particularly in processing, where switching is markedly slower than it is in mining activities. Also, the OECD report is illuminating in explaining why trade security should not be detached from industrial organization: concentrated supply chains amplify the effects of export restrictions because of the inability of downstream companies to requalify alternative materials, redesign input recipes and find reliable suppliers within the standard production schedules.[9] The history of Chinese controls since 2023 illustrates how this system functions in reality. In July 2023, the commerce ministry introduced export controls on gallium and germanium products, supposedly for reasons of national security, pointing out that simply controlling exports is not the same as forbidding exports.[10] In late 2023, China required a permit for some graphite products.[11]

In August 2024, it implemented export controls on antimony products, yet again emphasizing dual-use controls rather than country-specific sanctions.[12] The legal wording matters because it reveals the machinery: here, not necessarily a blanket embargo, but an administrative licensing regime under which approvals, conditions, wait times and scope can be altered on a case-by-case basis.[13] By legal form, that secures plausible deniability and nimbleness; by economic impact, the potential for uncertainty, precautionary stockpiling and reduced output among foreign manufacturers. The events of 2025 shifted the analysis from a potential latent concentration mechanism to a more tangible one of operational leverage. As reported by the International Energy Agency, China's controls over seven heavy rare earths, as well as its related compounds, metals and magnets, implemented in April 2025, in combination with controls over related products, components and technologies, implemented in October 2025, caused a rapid fall in China-linked exports, pressure on European and other international vehicle manufacturers and a rise in European prices of several heavy-rare-earth products. European prices for selected rare earths reportedly rose to as much as six times Chinese levels. China-linked controls were used through licensing restrictions in order to delay or limit scope expansion in the face of growing demand for products that rely on heavy rare earths and China-linked processes.

China-linked controls in 2025 also illustrate how leverage exposes actors across borders even in disputes that tangentially involve a third-party actor (here, the US). The EU’s risk of exposure is determined in part by the brewing US–China tensions and in part by China's systemic position in global value chains in key sectors. Capability, however, is not unlimited. The same ECB analysis points out pragmatic and strategic boundaries on rigid embargoes. Severe restrictions can harm Chinese exporters, accelerate import substitution, attract reprisals and sacrifice longer-term market share for immediate short-term market power. The 2010 Chinese rare-earth confrontation with Japan and the licensing shocks of the 2020s hint that substitution, recycling, frugality and process innovation are likely to accelerate in the face of sustained pressure.[14] The lesson is not that concentration is benign, but that the most plausible coercive scenario is partial and temporary interruption of supply in order to generate strategic bargaining power and that the time horizon is weeks, not decades. Where Europe can weather the initial adjustment period through stocks, accredited second suppliers, return flows, or short-term demand regulation, capability is effectively reduced.[15] Where it cannot, capability is transformed into power even in the absence of a formal embargo by the seller.

3. Intent: From Structural Capacity to Economic Coercion

Capability does not speak for itself as a categorical basis for a geopolitical response. States usually possess capabilities that they never exercise. The real challenge, therefore, is to assess intent without slipping into the fallacy of determinism. China has consistently maintained that the recent mine-to-metal controls were designed not as instruments of punishment, but to secure national security and non-proliferation goals.[16] This justification also appears in the sale restrictions on gallium, germanium and antimony issued by the Ministry of Commerce.[17] Such justifications should not be summarily swept aside; export restrictions truly can be motivated by security considerations and China's choice of statutory form is a microcosm of the global spread of dual-use controls. But such declarations cannot establish intention; whether these controls are security-driven must be deduced from their context, logic, sequence and object selection. This is a matter of probability, not certainty. The most straightforward EU-relevant evidence of coercive purpose is the Lithuania episode. The EU's WTO action against China alleged that from December 2021, China directed discrimination and coercion at Lithuanian exports and at EU products with Lithuanian content, including rejections at customs, restrictions on multinationals using Lithuanian inputs and a reduction in Chinese exports to Lithuania.[18] China rejected the EU account and the WTO complaint was dropped when trade recommenced; in other words, the episode cannot be regarded as a judicially conclusive ruling on illegality.[19]

But whether legally definitive or not, it is politically important. China displayed a readiness to employ informal or quasi-formal trade pressure not only against one EU member state but also against third-party firms with Lithuanian inputs. This matters more than whether Lithuania's trade with China ultimately exceeds that of Thailand or South Korea; what matters much more is China’s demonstrated willingness to leverage the systemic integration of European supply chains with a view to impacting political decision-making. The problem is not that China always weaponizes trade. It is that the bar for taking this option seriously has dropped. In evaluating intent, a helpful progression exists between a general rivalry and targeted inducement. China may not want at this point to spark a comprehensive breakdown of its relationship with the EU, given its huge European market and the key importance of European demand, technological imports and capital goods. Interdependence still moderates escalation. But targeted coercion need not be part of a widespread trade war. A limited slowdown in licensing of certain key magnet materials, an anti-subsidy case brought with the strategic interests of a key sector in mind, or pressure on certain companies relying on countries with cut-off supply as sources of supply can all induce enough stress to impact the behavior of companies and governments without ending wider economic engagement.

This is why concerns about intentionality should focus on possible case-specific coercive pressure, not full-scale economic conflict. Political distance assists in fine-tuning this risk calculation, but only as a proxy. Annual ideal-point estimates based on voting at the General Assembly of the United Nations serve as one of the currently most robust cross-national measures of medium-term global alignments of preferences across countries and have formed the basis of research at the International Monetary Fund, the European Central Bank and the Bank for International Settlements.[20] They are, however, also subject to many limitations. Annualized ideal-points data are available through 2024, while another UN voting summary exists through the end of the substantive part of the 80th General Assembly session in December 2025.[21] This means one can examine votes in 2025, but some distance proxy measures are still provisional. And more deeply, recent academic research suggests that UN General Assembly votes better reflect broad foreign-policy alignment than change during crisis; tightening or loosening of sanctions, public signals, or internal administrative acts frequently differ significantly from the Member State’s common preferences.[22] It is a useful but incomplete proxy for political alignment. It should therefore be interpreted as an indicator of broad geopolitical affinity rather than direct evidence of coercive intent. Its construction must specify the EU reference position, the resolutions covered between 2020 and 2025 and the treatment of abstentions and absences. Even with those caveats, the directional message for EU policy is clear.

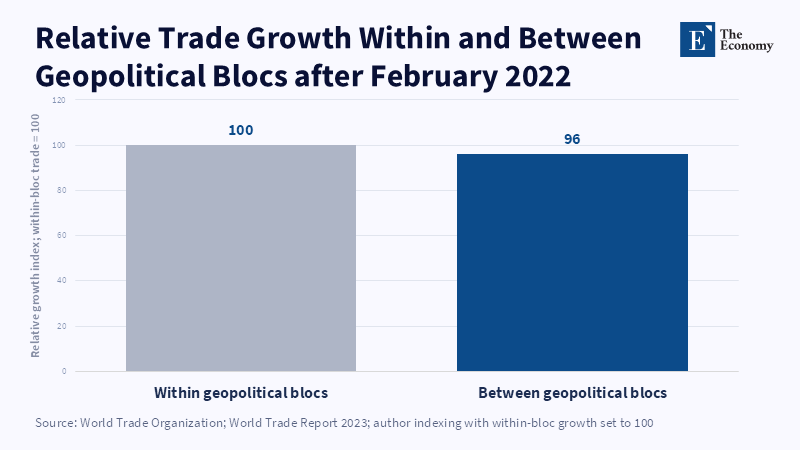

China is not part of a European strategic center consisting of treaty allies and other naturally sympathetic partners whose domestic regimes, security obligations and tension-driven diplomacy make political restraint more plausible.[23] BIS has demonstrated that trade between geopolitically distant partners grew significantly more slowly than trade between aligned partners between 2017 and 2023; the spread was more pronounced after Russia's invasion of Ukraine.[24] That finding should not be overinterpreted as evidence that distance causes coercion in any specific dyad. It does, however, tell us that geopolitically distant trading relations are economically consequential; they structure and steer trade in tangible ways. When a political gap aligns with focused supply capacity in sensitive sectors, the EU would be wise not to merely consider whether China can generate costs, but whether the marginal benefit of attempting to do so has increased given current circumstances. Equally, though, it is self-defeating to assume intent where the evidence against it is weak. Most of the EU’s vulnerabilities to China are due to the need to react against the consequences (commercial concentration, large-scale economies of scale, historical offshoring decisions, the slow development of parallel supply networks) rather than any attempt by China directly to coerce Europe.

The occasional signs of WTO incompatibilities and trade frictions, similarly, are not necessarily down to a predetermined Chinese geopolitical script-they may also be caused by idiosyncratic factors or, most often, by structural economic conditions rather than deliberate coercive intent. The 2025 Chinese export strength identified in the IMF's recent (2025) Article IV consultation was in part supported by a weaker real effective exchange rate, caused by inflation that was lower than that of the country’s trading partners, alongside weak domestic demand-hardly the evidence of one country deliberately attempting to reduce its real effective exchange rate to spark trade conflict.[25] And the examined OECD data on domestic subsidies illustrate the fact that they extend a country’s global market share without close correlation with productivity, which, of course, strengthens the argument that subsidies distort even in the absence of any stated intention to coerce Third Parties.[26] More accurately, EU–China tensions today are best viewed as an interaction among industrial subsidies, macroeconomic imbalances, geopolitical security necessities, technological pressures and political weaponization of trade, both internationally and downward to the individual consumer. This means any causal inference has to be case-specific rather than based on values or structural asymmetries.

4. The “Zone of Dependence”: Political Distance and Critical Supply

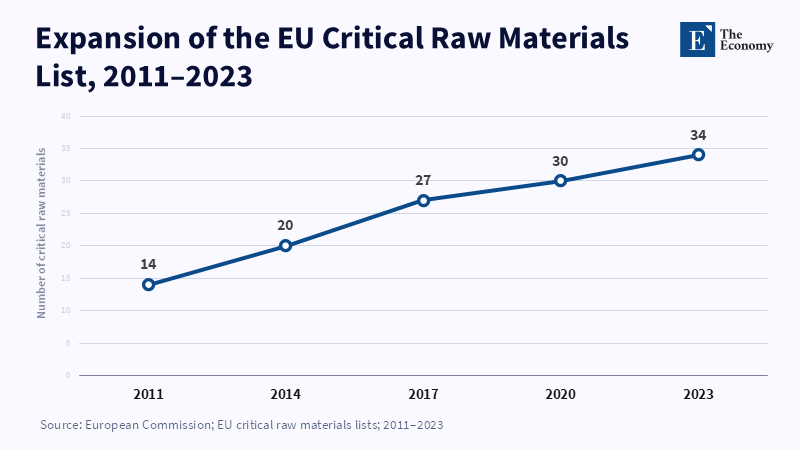

This concept of a “zone of dependence” is analytically useful in avoiding two opposite errors. One is to treat all non-allied suppliers as equal strategic threats. The other is to envisage the possibility of resilience being re-established only inside a tidy circle of perfectly aligned democracies. In fact, the EU's most important external suppliers span a continuum ranging from a strategic core of allies and like-minded partner regimes, through strategically distant states, to an interim category of transactional, issue-specific, or nonaligned states whose cooperation would be highly advantageous but can never be assured. China holds this middle position in a manner uniquely its own-too deeply integrated into Europe's supply chains to be considered just a marginal source of risk, yet too far removed to be considered a trustworthy systemic partner. The same general category may also include some or all of the economies of India and Brazil, although the respective risk profiles will not be the same. This zone cannot be defined by a single headline percentage of the share of all “critical supplies” in one geopolitical grouping. A country belongs in the zone of dependence only where significant exposure to system-critical EU supply chains coincides with comparatively weak geopolitical affinity. The category should therefore be based on both supply-chain importance and political distance, rather than on aggregate import value alone. Because the resulting shares vary with the product basket, weighting method and political-distance threshold, aggregate estimates should be treated as model-dependent rather than as fixed measures of EU vulnerability.

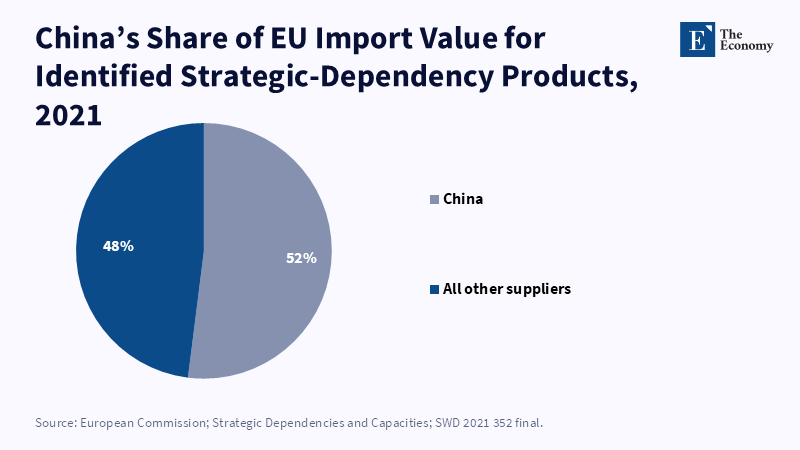

Exact calculations of how much of all “critical supplies” is in one geopolitical grouping are sensitive to the product basket used, the aggregation weighting scheme used, whether the calculation considers gross import values or irreplaceable inputs and whether the analysis focuses on mineral extraction, refining, or magnet production. The data that is publicly available more reliably substantiates the general diagnosis than any single aggregate figure can. One can be confident, at least, that official EU assessments repeatedly identify China as the premier foreign supplier in many nationally and strategically sensitive dependencies.[27] The Commission's 2021 assessment of strategic dependencies approximated that China supplied roughly 52 percent of the 137 identified products associated with essential dependencies.[28] The 2023 enhanced method produced 204 such products in sensitive industrial ecosystems where the EU meets significant foreign dependencies and highlighted the large number of single points of failure at stake.[29] The ECB's more recent foreign-critical-inputs calculation again identified China as the most prominent source of such inputs. Its precise nature and extent are subject to contestation, but China's centrality is not.[30] This centrality is also qualitatively different from the position of other countries in the zone. Brazil, for instance, is important for some raw materials and agricultural value chains, but does not possess China’s processing dominance, manufacturing capacity, tight integration into electronics and clean tech supply chains and coercive trade signals associated with China.

India is the key to the European diversification strategy, providing scale, engineering capacity and diplomatic flexibility for closer cooperation with the EU, but its long-standing strategic independence should prevent treating it as an overly simplified alternative to the Chinese threat.[31] Shifting some sourcing toward India or Brazil may reduce this risk without eliminating it, instead distributing exposure across a more plural and usually more manageable supplier base. That is the reason why “diversification” should not be mistaken for “security”. Depending on which supplier was substituted for an existing one, the type of new dependence created, as well as the institutional channels available in a crisis, will certainly matter. The zone concept also helps explain how European resilience cannot be directly inferred from the location of processing plants. A mineral refined or assembled within the EU does not become a European capability if the plant is dependent on Chinese feedstocks, Chinese technology, Chinese equipment, Chinese intellectual property, or Chinese ownership and corporate control.[32] Likewise, imports from outside Europe do not necessarily mean a strategic challenge if long-term contracts, multiple routes, interchangeable standards and allied crisis planning are such that dislocation is highly unlikely and highly manageable.

The key issue is the ability to manage continuity of supply. The Commission's Critical Raw Materials Act embodies this insight in its mix of domestic-capacity benchmarks with diversification, recycling and international relationships rather than assuming that extraction within Europe is the only pathway to resilience. The 2030 indicators, 10 percent of annual demand from extraction, 40 percent for processing and 25 percent for recycling, should be viewed predominantly as risk-reduction targets, rather than an exclusive strategy for self-sufficiency.[33] The zone of dependence must therefore be disaggregated by mechanism. Sometimes the risk is coercive leverage; other times it is export restriction exacerbated by domestic shortage, environmental policy, or industrial strategy.[34] In other cases, it is the fact that market concentration allows the supplier to appropriate scarcity rents even in the absence of a political motive. China may belong to all three categories in the case of different commodities. This again explains why a uniform policy toward “dependence on China” makes little sense from an analytical perspective. The EU does not need the same treatment for rare-earth magnets and pharmaceutical precursors, for processing of battery material or cloud infrastructure hardware and for ordinary consumer goods. The “zone” scheme makes sense only if it does not reduce important distinctions to a slogan.

5. Comparison with the US: Europe’s Energy–Technology Double Bind

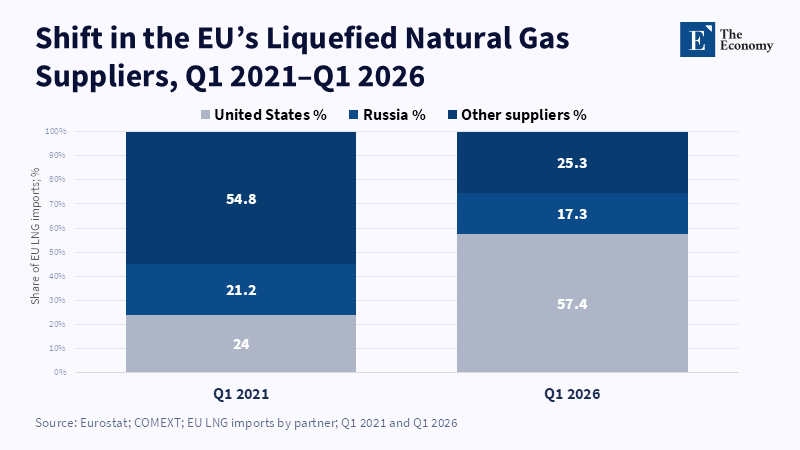

The comparison with the United States helps define what strategic autonomy means in practice. Europe's fundamental problem is not, as it seems at first glance, dependence on China alone. It is the development of a dual asymmetry in which dependence on the United States in certain energy and security fields has increased alongside dependence on China in certain technology and industrial chokepoint fields. This is not a symmetrical equivalence. Dependence on an ally may still create commercial exposure, but alliance institutions, legal remedies and crisis consultation generally make it more governable than reliance on a geopolitically distant supplier. The two dependencies are shaped by the legal environment, alliance politics, market structure and crisis behavior in various ways. Nonetheless, the comparison is instructive, as it draws the limits of a naïve debate on autonomy. If the goal was, literally, self-sufficiency, Europe would need to replace large parts of both relationships at huge economic expense. If the goal is resilient autonomy, the challenge is instead to lower exposure where influence and impact are high, while keeping all reliance, even on close partners, controllable rather than monocentric. The energy dimension of this double bind became more visible after 2022. It was revealed when the old Russian model of using the energy sector as a weapon fell apart. However, by 2025, Norway remained the EU’s leading pipeline-gas supplier, while the United States had become the EU’s dominant LNG provider.[35]

The European Commission notes that US LNG supplied nearly 58 percent of EU LNG imports in 2025[36] and Dutch onshore terminals that had previously shipped gas between the Netherlands and the United Kingdom now found their cargoes directed eastward.[37] This was a strategic achievement-it stemmed European losses in Russia’s wake and preserved energy supply security during a period of geopolitical conflict and energy-market restructuring. But it also represents the emergence of a new form of dependence. LNG contracts remain comparatively flexible-certainly more so than pipeline imports and the United States is host to a formal security partnership with Europe. LNG remains a globally traded and relatively flexible commodity, but it is subject to domestic US policies which may change with the timing of elections or US energy policy and is exposed to global competition and regional price pressures, or the growth of trade barriers and conflicting standards for methane and infrastructure. Alliance relations can change, but an alliance does not make Europe autonomous. The technology side is more complex because “technology dependence on China” is not a single story.

Europe is not generally reliant on China for all advanced technologies and in many frontier areas, the most severe non-European dependencies are on the US or other East Asian economies, rather than China. The strategically significant area is narrower: in parts of the green, digital and advanced-manufacturing areas—especially those involving minerals, processing, midstream materials and industrial scale—China occupies chokepoints which could disable downstream European production. Rare-earth magnets, graphite anodes, some battery precursors, gallium and germanium and a variety of industrial intermediates are more important here than finished consumer electronics.[38] The dependence, then, is not simply “Europe buys Chinese technology”, but that Europe's own industrial transition depends on supply chains in which China dominates the crucial upstream or midstream stages. Comparison with the US similarly demonstrates why political cooperation cannot be substituted for market logic. A supply disruption by an important partner is conceivable, but the mechanisms to handle it differ: alliance consultation, legal remedies, strong financial and diplomatic interconnections, joint sanctions regimes and broader reciprocity all increase the political import of coercive behavior. These governing dynamics do not imply the absence of asymmetries. They do, however, translate some aspects of vulnerability into what one might term governable reliance. Reliance on China is less institutionally governable. Although bilateral volumes are again huge, institutional confidence is not; security affinities are less extensive; preexisting coercive pressures and export-licensing controls make the EU less inclined to patience under duress.

Dependence can exist with either Washington or Beijing. The strategic implications of dependence are not equivalent, however: one is built atop an alliance system, while the other is based on a rival state, within an increasingly securitized economic relationship. If applied, this distinction should discipline both Atlanticism and reflexive anti-Americanism within Europe. It would be analytically wrong to treat US LNG dependence as trivial just because the United States is a friend and would be incorrect to mistakenly conclude from that fact that there is consequently no significant strategic difference between Washington and Beijing. What the EU should seek to pursue is not symmetry but rather the reduction of concentrated dependencies so that European freedom of action would not be compromised. This would mean, in energy, that a European insurance policy against emergency substitution should not be allowed to develop into a new single-supplier arrangement; in China-linked industrial ecosystems, it would mean trimming the proportion of supply reliant on bottleneck imports controlled by the Chinese suppliers or institutions. Strategic autonomy in this admittedly weakened form, then, is not neutrality amid the great powers but rather the capacity for a European policy that does not allow its decisions to be constrained by unnecessary exposure to any one of them.

6. Strategic Autonomy: De-Risking Without Decoupling

However, if the diagnosis is selective vulnerability and not centralized reliance, the policy conclusions are fairly specific: the EU should avoid two opposing errors: protectionist common sense, that a large open economy 'can only both be open and hold its own if it can produce everything it needs itself'; and the dogma that diversification automatically produces resilience. The more rigorous concept of strategic autonomy views resilience as best seen as the institutional ability to absorb, reroute and politically endure shocks to system-enabling supply chains while remaining broadly open to flows that do not entail similar risks and burdens. This is de-risking: a narrow and targeted alternative to broad decoupling, as well as a pragmatic policy framework. It requires targeted actions articulated with a targeted rationale. First, more granular monitoring. Aggregate trade figures are too crude and product-level indicators have become too static to reveal the real centers of leverage. The ECB is right to focus on the micro data set to show which firms, regions and stages of production are most vulnerable. The Commission's shift from simple import shares toward identifying single points of failure demonstrated an improvement in its strategic-dependencies framework, but the next phase should be a supply-chain observatory for system-critical inputs, at the EU level, combining customs records, legally permissible firm-level sourcing decisions, certification bottlenecks, stocks, technological interdependencies and patterns of ownership.[39] It should not be a generic barometer for every sensitive sector. It should focus on key products where small upstream shocks can bring down large downstream networks. The objective is to be able to respond more quickly to operational signs of disruption than to formal policy announcements. Hence, the second requirement is disciplined diversification. Diversification is invoked as an assumed benefit in many politically salient debates at present. That assumption is too shallow. Diversification can cause costs by producing smaller production runs, by producing duplicated certification through multiple suppliers, by lowering output due to fixed economies of scale and by raising prices for final consumers or industrial users. Those costs can be tolerated only where substitution in a serious emergency would be too slow, as, for example, in a war. The objective is not to eliminate Chinese sourcing across every green or digital product, but particularly those inputs for which substitution time in a serious emergency is long relative to the time cost of the interruption. For inputs such as permanent magnets, graphite anodes and specialized chemicals, the EU should commit itself to long-term offtakes, through European Investment Bank credit, private-sector demand aggregation and standards cooperation with credible suppliers to turn second and third sources into commercially viable suppliers able to meet required quality standards.

In industries where multiple suppliers exist and switching costs are low, the argument for intervention has even less force. The third requirement is emergency preparedness. Here, the EU should be more willing to acknowledge the difference between price insurance and continuity insurance. Recent International Energy Agency guidance is compelling: strategic stockpiles are best deployed as short-term buffers keeping business going through periods of severe shock in the near term, not as secondary measures for ongoing product market management.[40] This argues for more selective stockpiling than mass stockpiles of all seemingly "critical" goods in readiness. Control releases should be narrow, simple and short-lived to help market adjustment without weakening private incentives to diversify. The fourth requirement is to deploy trade and internal market instruments with far greater specificity. Trade-defense instruments are appropriate where the problem is distortion caused by subsidization or dumped prices. Procurement restrictions apply where reciprocity is not part of strategic public procurement.

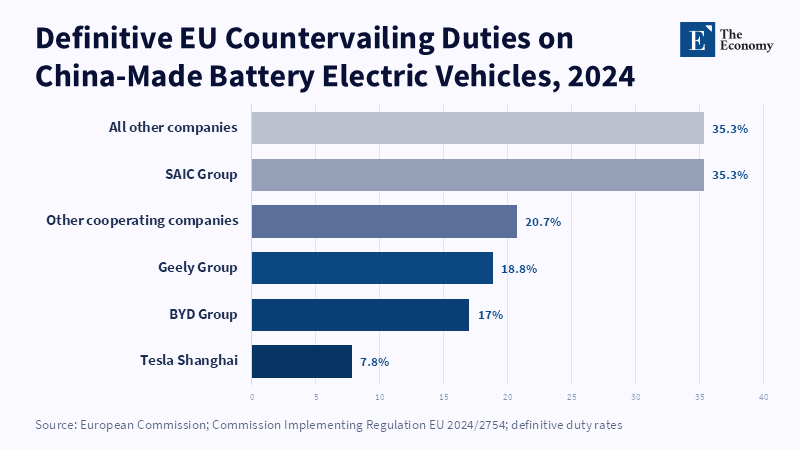

Foreign direct investment screening is relevant where control of key assets or technologies is an issue. The Foreign Subsidies Regulation is relevant when state-supported competition distorts the internal market. The Anti-Coercion Instrument is relevant when political pressures are the source. Those instruments should not be reduced to a uniform ideological statement about “toughness”. The legitimacy of those instruments will depend on a tight causal fit. The EU's recent invocation of definitive countervailing duties on Chinese battery electric vehicles, its first-ever International Procurement Instrument measures in the medical device sector, the Foreign Subsidies Regulation and the provisional agreement to strengthen the EU’s FDI screening regime exemplify an emerging toolbox.[41] But their consistency will rely on whether the Union deploys them as focused responses to specific threats rather than as a broad toolkit to compensate for industrial competitiveness shortcomings. Fifth, the argument implies that European co-production with allies should be viewed primarily as a bargaining tool for risk mitigation, rather than exclusively as an instrument of industrial diplomacy. For some of the resources and components needed, Europe will not have the swift, cost-effective production capacity at every stage by itself. Instead, for those materials, most co-production partnerships with countries possessing a range of geological assets, processing capacities and technology synergies may be both more cost-effective and more “efficient” in economic theorists' terms than unmanaged dependence on imports or prohibitively costly autarky.

But co-production also must be negotiated. If Europe merely shifts one bottleneck to another location without binding offtake commitments, information sharing and priority access during supply emergencies or a formal crisis-coordination agreement, formal diversification may have limited strategic value. The EU must have contractual and institutional crisis guarantees. These counterarguments deserve serious weight. Concentrated trade is, for the most part, a reflection of scale and learning effects, not maliciousness. Chinese investment can build up production, employment and technological production capacity within the EU. Import substitution can be fiscally expensive and can result in permanent support for uncompetitive firms. Coercion is limited through reciprocal dependency: China needs sales, high technology and money in the EU as much as the EU needs inputs from China. All that is true and this is where decoupling per se is unwarranted. But these objections do not provide the defining judgment. They at least partly delineate the few circumstances in which a pragmatic intervention can be confined to its narrow scope. Where disruption would be economically minor, alternative supply is readily available, or substitutes can be secured rapidly, or where mutual dependence is sufficient to prevent coercion, market adjustment should remain the preferred response.

Where globally traded inputs are highly concentrated and difficult to replace, there are costs to doing nothing that may outweigh the fiscal costs of targeted resilience measures. The unresolved question is whether the EU can develop the capacity to implement such a strategy. Its difficulty has never been the lack of tools alone but rather, more often, comes from the fragmentation of policies across member states, uneven industrial capacity, commercial confidentiality, bottlenecks in permitting and delays and disagreements on how much cost to accept before a shock arrives. Such strategic autonomy is a failure if it ends up being not only a slogan, but one that is defined and translated differently by each of the member states; it ends up gathering every possible justification for protection. The credible policy toolkit is more modest in breadth, but more credible in implementation: identify the products and diffusion vectors for which shock-related interruptions would have grave structural consequences; identify who controls each critical juncture; hedge the short term through inventories and contingency planning; diversify over the medium term through finance, standards and pacts; establish improved crisis mechanisms for obvious external coercion; and leave the rest of the economic relations unencumbered. Europe need not cut off trade with China, but it must make it impossible for select Chinese chokepoints to continue to determine the contours of European adaptation.

7. Conclusion - Reducing Leverage While Preserving Openness

China’s status as a major trade partner is not itself the central problem; what matters is whether in a handful of upstream chokepoints the all-in concentrated exposure can be turned into systematic leverage over European production or policy. The answers point to a cautious yes, but one that is still highly asymmetrical. The risk is high where scale, processing power, licensing power and geopolitical remoteness coincide with system-enabling inputs in the critical corridors that EU firms cannot substitute quickly. The risk is modest where markets are contestable, substitutes are available, inventories smooth disruptions, or reciprocal constraints make coercion unviable. It follows that policy should avoid both complacency and panic. Complete disconnection would be irresistibly costly and obfuscate the real challenge. Unqualified openness would breed vulnerabilities precisely where a tiny disturbance could trigger outsized ad hoc consequences. The rational way forward requires a focused combination of assessment, diversification, contingency planning and selective cooperation, including the broadening of instruments with which to regulate, procure, screen foreign investment and deter coercion. Only this approach will prevent strategic autonomy from becoming hollow rhetoric. Removing leverage from critical chokepoints without sacrificing the openness on which European prosperity relies is indispensable.

References

[1] European Commission and High Representative of the Union for Foreign Affairs and Security Policy (2023) Joint Communication on a European Economic Security Strategy. JOIN(2023) 20 final. Brussels: European Commission.

[2,17] International Energy Agency (2025a) ‘With New Export Controls on Critical Minerals, Supply Concentration Risks Become Reality’, IEA Commentary, 23 October. Paris: International Energy Agency.

[3] Council of the European Union (2025) EU–China Trade: Facts and Figures. Brussels: Council of the European Union.

[4,5,30] Essers, D., Lebastard, L., Mancini, M., Panon, L. and Timini, J. (2024) ‘Critical Inputs from China: How Vulnerable Are European Firms to Supply Shortages?’, The ECB Blog, 9 October. Frankfurt am Main: European Central Bank.

[6,32] Carrara, S., Bobba, S., Blagoeva, D., Alves Dias, P., Cavalli, A., Georgitzikis, K., Grohol, M., Itul, A., Kuzov, T., Latunussa, C., Lyons, L., Malano, G., Maury, T., Prior Arce, A., Somers, J., Telsnig, T., Veeh, C., Wittmer, D., Black, C., Pennington, D. and Christou, M. (2023) Supply Chain Analysis and Material Demand Forecast in Strategic Technologies and Sectors in the EU: A Foresight Study. EUR 31437 EN, JRC132889. Luxembourg: Publications Office of the European Union.

[7,8,38] International Energy Agency (2025b) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

[9] Organisation for Economic Co-operation and Development (2026a) Critical Raw Materials Face Rising Export Restrictions, Increasing Risks to Global Supply Chains. Paris: OECD.

[10] Ministry of Commerce of the People’s Republic of China and General Administration of Customs (2023a) Announcement No. 23 of 2023 on Export Controls on Gallium- and Germanium-Related Items. Beijing: Government of the People’s Republic of China.

[11] Ministry of Commerce of the People’s Republic of China and General Administration of Customs (2023b) Announcement No. 39 of 2023 on Optimising and Adjusting Temporary Export-Control Measures for Graphite Items. Beijing: Government of the People’s Republic of China.

[12] Ministry of Commerce of the People’s Republic of China and General Administration of Customs (2024) Announcement No. 33 of 2024 on Export Controls on Antimony- and Superhard-Material-Related Items. Beijing: Government of the People’s Republic of China.

[13,16] State Council Information Office of the People’s Republic of China (2021) China’s Export Controls. Beijing: Foreign Languages Press.

[14] Organisation for Economic Co-operation and Development (2024) Trade Impacts of Economic Coercion. OECD Trade Policy Paper No. 281. Paris: OECD Publishing.

[15] Aguilar, P., Darracq Pariès, M., Jouvanceau, V., Meunier, B. and Spital, T. (2026) Global Implications of Export Controls on Rare Earths: A Model-Based Assessment. ECB Occasional Paper No. 384. Frankfurt am Main: European Central Bank.

[18] World Trade Organization (2022) China—Measures Concerning Trade in Goods and Services: Request for Consultations by the European Union. WT/DS610/1. Geneva: World Trade Organization.

[19] World Trade Organization (2025) China—Measures Concerning Trade in Goods and Services: Communication from the European Union. WT/DS610. Geneva: World Trade Organization.

[20] Bailey, M.A., Strezhnev, A. and Voeten, E. (2017) ‘Estimating Dynamic State Preferences from United Nations Voting Data’, Journal of Conflict Resolution, 61(2), pp. 430–456.

[21,22] Adarkwah, G.K., Sabel, C.A. and Zilja, F. (2026) ‘Measuring Geopolitics: The Promise and Limits of UNGA Voting Data for IB Research’, Journal of International Business Policy, 9, pp. 102–123.

[23] European Commission and High Representative of the Union for Foreign Affairs and Security Policy (2019) EU–China: A Strategic Outlook. JOIN(2019) 5 final. Strasbourg: European Commission.

[24] Blanga-Gubbay, M. and Rubínová, S. (2023) Is the Global Economy Fragmenting? WTO Staff Working Paper ERSD-2023-10. Geneva: World Trade Organization.

[25] International Monetary Fund (2026) People’s Republic of China: 2025 Article IV Consultation. Washington, DC: International Monetary Fund.

[26] Organisation for Economic Co-operation and Development (2025) The Market Implications of Industrial Subsidies. Paris: OECD.

[27,28] European Commission (2021) Strategic Dependencies and Capacities. Commission Staff Working Document SWD(2021) 352 final. Brussels: European Commission.

[29,39] Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An Enhanced Methodology to Monitor the EU’s Strategic Dependencies and Vulnerabilities. Single Market Economy Papers WP2023/14. Brussels: European Commission.

[31] Ministry of External Affairs, Government of India (2024) Annual Report 2023–24. New Delhi: Government of India.

[33] European Parliament and Council of the European Union (2024) Regulation (EU) 2024/1252 of 11 April 2024 Establishing a Framework for Ensuring a Secure and Sustainable Supply of Critical Raw Materials. Official Journal of the European Union, L 2024/1252.

[34] Organisation for Economic Co-operation and Development (2023) Raw Materials Critical for the Green Transition: Production, International Trade and Export Restrictions. OECD Trade Policy Papers No. 269. Paris: OECD Publishing.

[35] Eurostat (2026) EU Imports of Energy Products—Latest Developments. Statistics Explained. Luxembourg: Eurostat.

[36] Council of the European Union (2026a) Where Does the EU’s Gas Come From? Brussels: Council of the European Union.

[37] Reuters (2026) ‘EU’s Ribera Warns of Increasing Dependence on US LNG’, Reuters, 28 January.

[40] International Energy Agency (2026) ‘Designing an Effective Strategic Stockpiling System for Critical Minerals’, IEA Commentary, 27 January. Paris: International Energy Agency.

[41] Council of the European Union (2026b) European Economic Security. Brussels: Council of the European Union.