Europe Needs Control, Not Autarky: A New Test for European Industrial Autonomy

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Europe’s green transition depends on foreign-controlled supply chains Factories alone do not create industrial autonomy Selective de-risking is stronger than full decoupling

In 2024, China supplied 98 percent of the solar panels Europe imported from outside the bloc. That figure is often used as evidence that Europe has long ago lost the clean-technology race. It signals a real risk but it also obscures the more difficult question. A solar panel, like a battery or a computer processor or power electronics, can be cheap, widespread, and affordable, and still contribute to a long-term erosion of manufacturing options. European industry is therefore not a pure fight between imports and bricks-and-mortar plants. It is the capacity to sustain essential systems, shift providers, advance technology, and dictate terms when markets tighten. A factory in Europe may generate jobs without generating control. An imported product may generate dependency without an immediate threat. Policy must mark out these cases. Europe needs fewer platitudes about resilience and a far less tolerant criterion for who controls the know-how, physical inputs, and strategic choices that sustain production.

European Industrial Autonomy Starts Below the Factory Gate

The standard dependence map is drawn at the border. It states the value and source of finished goods, then interprets a high share of imports as vulnerability. That is a helpful warning indicator, but it is not a comprehensive interpretation of risk. In 2024, China provided €141 billion of the EU's 478 billion extra-EU imports of high-tech goods. Industry-level reports also have China's share at 52.8% for lithium-ion batteries, 54.5% for computers, 40.7% for smartphones, and 63.7% for photovoltaic cells. Even these may underplay the level of risk. Even a single-market traded product can rely on Chinese components, tools, patents, or process expertise. Europe's industrial independence will be determined internally from the factory door, and ownership, supplier approval, machinery, software, and engineering expertise determine whether output can be sustained. Customs inspections reveal where a product entered the EU. They cannot reveal who is able to re-engineer it, replace a failed component, or approve the next generation.

This alters the policy test. The notion that local production is relevant only if it enhances Europe's strategic levers is correct only if a battery plant increases resilience by establishing process know-how, training engineers, bolstering suppliers, and being flexible in the face of a disruption. It is much less true if the chemistry, equipment, critical materials, and design monopoly are firmly held elsewhere. The same rule also applies to solar modules assembled from imported wafers and cells, as well as electronics marketed under a European brand name but manufactured with foreign chips, contract manufacturing, and exclusive supplier agreements. None of this implies that foreign ownership is necessarily detrimental. FDI can provide the cash, agility, and skills that Europe itself lacks. The key question is whether public aid provides sustainable competency or merely local output. Europe's industrial independence cannot be measured according to the inaugural launch of a plant, but according to the decision rights preserved in Europe when the subsidy expires.

Batteries and Solar Expose the Same Control Gap

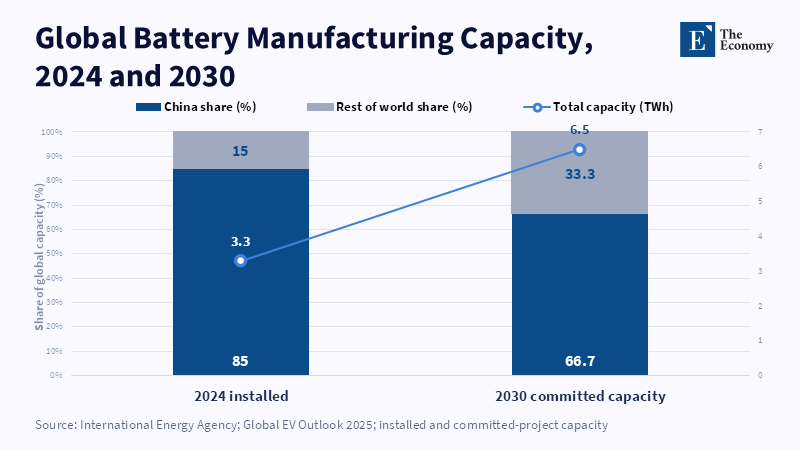

Batteries exemplify how scale without depth can turn into a trap. China commanded roughly 85 percent of global battery cell manufacturing capacity in 2024, and over three-quarters of that was owned by Chinese firms. Its dominance extends to cathode and anode production, refining, machinery, and lithium iron phosphate chemistry. That intense industrial concentration accounts for why battery pack prices in China had in 2025 been around 35 percent below European levels. Europe cannot bridge that difference by constructing one more cell manufacturing plant. It requires an interconnected foundation of material processing, process engineering, pilot lines, recycling, and machinery vendors. Northvolt's failure in March 2025 starkly illustrated the difference. Nameplate capacity does not equal operational capacity. A project can receive political support, attract highly-skilled personnel, and represent a strategic boon, and still dramatically underperform if facing enormous capital costs, lack of market or supply chain momentum, or dampening of demand. So industrial independence for Europe must be measured in actual gigawatt-hours of manufacturing, not necessarily prospects for them.

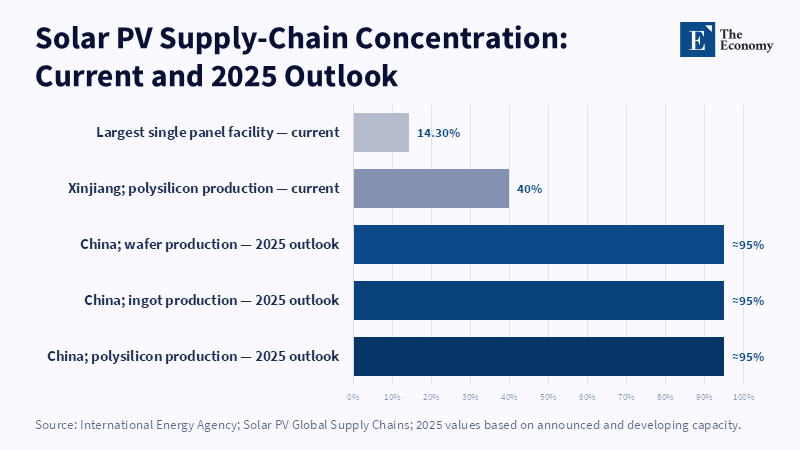

Solar power is the mirror image. Low-cost Chinese modules enabled Europe to add renewable capacity quickly and limit its reliance on imported fossil fuels. Raising prices through the whole market would slow down projects and increase costs for homes, businesses, and government alike, but low prices could also wipe out the industrial base on which tomorrow's choices depend. According to industry data, in 2023, the EU produced just over 15 percent of the modules it consumed. By 2025, the Union had built 12 GW of module capacity, about 2 GW of cell capacity, and less than 1 GW of ingots and wafers. The underdevelopment is therefore not simply at the ends but also in the middle, where the production of wafers, cells, equipment, and process knowledge dictates survival. Europe does not need to duplicate every process-just enough to close the gap at each new step.

Electronics add a third warning. The EU's high-tech deficit with China hit 92 billion in 2024, but the strategic challenge goes beyond only that deficit. Green systems now pack more digital hardware. Electric cars, battery-management systems, renewable plants, grids, and factories all deploy sensors, processors, communications equipment, and power electronics. A pinch point in one small component can slow an entire clean energy project. Meanwhile, Europe's bleeding weakness is not merely China-centric. High-end chips also lean on companies and plants in Taiwan, South Korea, and the US. The European Court of Auditors projected that by 2030, the EU would make just 11.7 percent of global chips, well short of its 20 percent target. A solution to that has to include a front-to-back strategy of functions and substitutability. Slogans on how to de-remote channels cannot fix a supply chain with varying risks by item, tech, and partner.

Managed Interdependence Needs Hard Conditions

The practical alternative to autarky is managed interdependence. That involves accepting that Europe will continue to source technology, capital, and components from abroad while sealing off risks of equipment supply or technology when a single supplier can block all production or impose a de facto toll on advanced-technology goods. It sounds more moderate than opening to everyone, but it calls for tougher policies, too. Foreign investment should be admitted where it fosters learning, supply linkages, and unimpeded access. Public funding, which is more likely to be feasible, should be contingent on concrete objectives. These could be European pilot lines, domiciled engineering teams, supplier development strategies, stockpile arrangements, research requirements, and transparent progression pathways for technical personnel in mastering the process. Such a factory that draws on imported technology can still contribute to European industry and technology throughput, but only if knowledge flows on from a closed operating unit and if related future upgrades are not entirely ruled by outside decisions.

The second lever is procurement. The Net-Zero Industry Act would permit resilience and other non-price criteria to influence certain public procurement and renewable-electricity auctions. In highly concentrated technologies, these criteria are designed to support at least 30% of annual auction volume within each member state, or 6 GW if that number is lower. This is more specific than a general import ban because it can establish a reliable domestic backlog of selected capacity either in Europe or amongst allies. The scope should stay as tight as possible. Grids, power electronics, and other areas where it would be very expensive to do without the last existing producer should be prioritized. Exempting each product category from the policy would both inflate the cost to taxpayers and hinder deployment. Autonomy for European industry requires targeted demand.

Finance must also follow the same principle. The Clean Industrial Deal allocated over 100 billion for clean manufacturing, while the Innovation Fund opened a 1 billion call for electric-vehicle battery-cell projects in late 2024. The issue is not merely the size of the headline. It is whether the ring-fenced capital is connected with transparent deliverables that could endure pressure. Public funds should be released incrementally once project developers indeed hit production, supplier diversity, workforce training, research, and risk mitigation milestones. Governments must also make a clear distinction between a signed memorandum of understanding and an assurance of supply. Raw-material concessional agreements do not always lead to production in mines and refining facilities, and delivery. Europe requires offtake contracts, public support guarantees, recycling capacity, and co-investment in processing. Building a supply chain in Europe means delivery of projects, not just public relations or international pacts.

Trade defense still has a part to play, but it cannot bear the whole strategy. It can match the effects of proven subsidies, slow a damaging import wave, and free international funds for investment. It cannot provide a firm with cathode material, help them design a wafer line, or operate a complex factory competitively. If overused, it can also lead to higher input costs, delay climate policy, and provoke reprisals. The strategy should be conditional and reversible. Trade measures should secure a discrete capability while investment, procurement, and skills policy build that capability. They should terminate when that task is completed or when the ratio of costs to benefits tips into negative territory. European industrial strategic autonomy will succeed neither if it is branded as a voice for permanent protection, nor if price deflation is seen as irrefutable evidence that markets are ever-reliable substitutes for exhausted assets.

Measure Sovereignty by What Survives a Shock

A more meaningful scorecard would be metrics on control instead of location. What it would measure is which technology is owned, key, where process engineers are, how many suppliers are qualified, how rapidly inputs can be substituted, and whether a plant stays profitable when prices or demand shift. It would break down sectors. Batteries need a self-sustaining minimum of cells, active materials, recycling, and process engineering. Solar needs upstream capacity that doesn't fully ensnare the whole value chain, while still maintaining access to low-cost modules. Electronics needs greater transparency on embedded inputs and, as much as possible, more power in equipment, power electronics, and industrial hardware. There are those competing objectives. One mega-shoring campaign that simply lumps together everything in one hunt for the highest-volume factories risks channeling funds into the easiest chokepoint to fix rather than the hardest to pull out of the way. European industrial self-sufficiency needs to be specific enough to challenge and humble enough to be plausible.

To be sure, critics will say this is too expensive, too slow, or too vulnerable to political influence. All of those things are true. Industrial policy can shelter fragile companies and convert transitory aid into a reason for more public expenditure. But the solution is not to ignore concentrated supply networks. It is to routinize the contestability of aid, make it time-limited, and use it as an incentive, not a subsidy. Agencies should set out sectoral objectives transparently, assess the cost of resilience against what they gain, and cease funding unprofitable projects. They should defend intra-European competition too. Independence does not necessarily mean swapping one reliance on foreign production for a small clique of protected domestic ones. The essential idea is a market with more access points, more locations of knowledge, and more leverage. That is not self-reliance. That is a rational exercise of choice.

The figure in the first box is very clear: in 2024, China supplied 98 percent of any extra EU solar-panel imports. For sure, the policy solution does not lie in Europe building every single panel. Rather, it lies in Europe's controlling knowledge of which capabilities must not be lost, and then paying for those capabilities with accuracy. This same principle applies to batteries, chips and the digital equipment at the heart of the green transition. Factories have value; control matters more. Instruments of public investment, purchase, and market shaping need to be assessed on the extent to which Europe's capability to produce, switch, and improve was intact when circumstances grew hostile. European industrial sovereignty will not be ensured by a vow of independence or interdependence. It will be ensured by the process of making interdependence less asymmetric, less invisible, and less fragile. Europe must learn to measure what would still be up and running on the first day of a full-blown shock.

This article is based on an original research article published by The Economy Research. For the original version, please refer to [EU vs. China] The Green-Digital Dependency Trap: China, Batteries, Photovoltaics and Europe’s Industrial Autonomy.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An Enhanced Methodology to Monitor the EU’s Strategic Dependencies and Vulnerabilities. Brussels: European Commission.

European Commission (2024) European Solar Charter. Brussels: European Commission.

European Court of Auditors (2025) The EU’s Strategy for Microchips: Reasonable Progress in Its Implementation, but the Chips Act Is Very Unlikely to Be Sufficient to Reach the Overly Ambitious Digital Decade Target. Special Report 12/2025. Luxembourg: European Court of Auditors.

Eurostat (2025a) International Trade in Products Related to Green Energy. Luxembourg: Eurostat.

Eurostat (2025b) EU High-Tech Trade Back to a Surplus in 2024. Luxembourg: Eurostat.

International Energy Agency (2024) Energy Technology Perspectives 2024. Paris: International Energy Agency.

International Energy Agency (2025) Global EV Outlook 2025: Expanding Sales in Diverse Markets. Paris: International Energy Agency.

International Energy Agency Photovoltaic Power Systems Programme (2025) Trends in Photovoltaic Applications 2025. Paris: IEA PVPS.

Joshi, S. (2026) Early Lessons in the Pursuit of Sovereign AI. Washington, DC: Carnegie Endowment for International Peace.

Ranking News Editor (2026) National Competitiveness Indices and Their Role in Economic Policy Reform. The Ranking News.

The Economy Research Editorial (2026) The Geopolitics of Compute: Sovereignty, Power and Strategic Dependence in the AI Infrastructure Race. The Economy Research.

The Economy Research Editorial (n.d.) [EU vs. China] The Green-Digital Dependency Trap: China, Batteries, Photovoltaics and Europe’s Industrial Autonomy. Dublin and Schwyz: The Economy Research and Swiss Institute of Artificial Intelligence.

Ülgen, S. (2026) From Trade Dependence to Geopolitical Leverage: The EU in an Era of Weaponized Interdependence. Washington, DC: Carnegie Endowment for International Peace.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.