Fed Communication Strategy: Promise Less, Explain Better

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Markets react to what policy surprises reveal, not only to their size Warsh’s quieter Fed should reduce promises without hiding its reasoning Central-bank credibility depends on evidence rather than constant forecasts

Two rate moves by the same 25 basis points may trigger market reactions ten times greater. It isn't the change; it's the story the market believes. More tightening than the market had priced is taken to be good evidence of a serious issue. Less tightening than expected provides weaker, less conclusive information. That's why discussion of a new Federal Reserve communications strategy shouldn't be thought of as a choice between constant updates and silence. Instead, it is a choice between promises about rates and clear reports on how the central bank will respond as conditions change. Kevin Warsh is correct to strip away the forward-looking promises that risk quickly becoming outdated. But his quieter Fed can work only if it talks clearly about its objectives, evidence and how it decides to act.

Markets Don't Read Minds-They Price Signals

Financial markets cannot read central bankers' minds; they can only price their signals. These signals come from speeches, forecasts, press-conference transcripts, reports and the movements of other assets. Such judgments are tentative. Price pressures could be mounting or easing or the job market could be strengthening or weakening. An investment thesis that made sense on Monday may no longer be plausible when the committee meets six weeks later. Forward-looking messages do not solve this problem; they can aggravate it by giving market participants more phrases to interpret, run and reweight. The market begins pricing not only the economy but also its assessment of the Fed's assessment of the economy, creating a feedback loop in which both players watch each other closely and which risks generating many false signals.

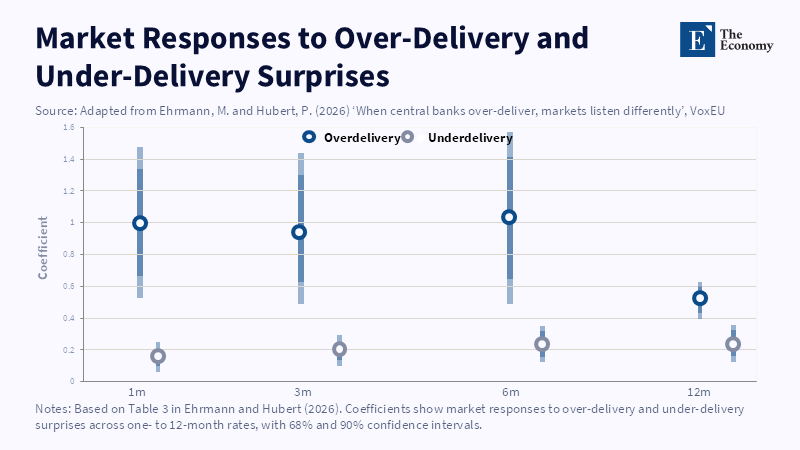

An analysis of 2,381 policy decisions made by the central banks of 14 advanced economies from January 1997 to March 2023 found that about 18% exceeded market expectations and 20% fell short. For short-term rates, the move after such a surprise tightening was as much as 10 times greater than when the decision disappointed the market. This was not solely because markets were startled by an unanticipated action. Revisions to the forecasts made in advance of the decisions indicate that investors interpreted stronger-than-expected tightening as new information about the economy itself. A larger increase was seen as an indication that the central bank perceived inflation pressures or demand conditions to be more robust than public forecasts had assumed. Thus, a surprise increase in tightening was sending at least two messages: that policy had changed and that the central bank's private assessment of conditions might be more serious than indicated by the available public data. Loose communications ahead of such moves amplified the shock, forcing investors to reconsider both the rate path and their views on economic conditions.

This finding shifts the framing of the policy question. It suggests that the objective is not to make every meeting’s announcement wholly predictable, because that is impossible when economic circumstances shift and judgment is involved. Nor should the Fed endeavor to eliminate all surprises from the markets; they may be necessary when inflation conditions change rapidly or the economy faces risks to financial stability. Rather, the objective should be to mitigate the risks of false expectations fostered by precise future policy pledges. A useful Fed communication policy would commit to an unchanging objective but leave its chosen means flexible. The market should understand the Fed’s goal and what facts it weighs most heavily. It should not treat a projection for the path of interest rates as a commitment. Such an approach allows policy to be responsive as data change, without transforming every update into a test of central-bank credibility.

A Better Fed Communications Strategy: Principles, Not Predictions

The chairman’s initial meetings offer a concrete example of such a split between principles and predictions. The target range for the federal funds rate remained 3.50–3.75% after the May 1 policy meeting by a 12–0 vote. The accompanying statement, at 132 words, was a marked reduction from April’s 246-word missive. The statement eschewed forward guidance, emphasized the central bank’s 2% inflation goal and concluded with a clear promise to maintain price stability. Chairman Warsh also eschewed putting his own individual projection in the Fed’s dot plot-a summary of policymakers’ expected future interest rate settings. This was a clear statement: a firm objective, an unspecified plan to act when the time comes and then evaluate the economic situation in the next meeting. It aligns with an environment where forecasts are likely to fail between meetings and allows the Fed to adjust policy as needed, rather than being constrained by past commitments.

This logic is particularly pertinent when the economy is buffeted by supply-side shocks-for instance, a spike in energy prices or the impact of war, tariffs or a large migration event. A policy set based on predictions made prior to such events may prove inappropriate when the relevant data become available. If so, strict forward guidance will compel the central bank either to stick to a suboptimal policy and thereby risk higher inflation or to reverse course and thus undermine its credibility. Such an action is not in itself irresponsible; policy should change when conditions change. Rather, the error is in creating the illusion that the earlier plan was based on solid ground. The Fed’s strategy review in early 2025 reaffirmed the 2% long-run inflation target and its regular review of its strategies and communication framework. This provided an appropriate foundation: keep the objective fixed and let the path vary as conditions do.

However, policy cannot simply float free when conditions change; it must have rules of engagement. While the Fed may not wish to codify a mechanistic formula, the Fed should clarify the relative order of importance it assigns to the criteria that determine policy outcomes. If the economy faces inflation pressures that are well above target, for example, a Fed communication should clarify whether those pressures are widespread or narrowly based, whether they seem likely to be persistent or temporary and what they represent: demand-driven growth or supply constraints. It must also clarify what data and trends would signal that inflation is returning to target. In like fashion, when labor conditions appear to be cooling, the communication should articulate the source of this cooling-whether it stems from a slackening in demand, a slower labor-supply growth trend or simply the normalizing of an overheating labor market. This would not constitute a pledge of rates, but a road map of the decision process. The communications should guide the way without suggesting the route is predetermined.

Warsh’s Quieter Fed Risks Becoming Obscure

Warsh’s first post-meeting news conference offers an immediate indication of the risks. Although Warsh said many words about price stability, he offered few specifics about the thresholds that would trigger a rate increase. Market participants, reacting to the vagueness of the announcement, swiftly adjusted their expectations upwards, quickly pushing short-term yields higher. Within days, many forecast analysts moved from expecting as many as three Fed hikes in 2026 to anticipating as many as three cuts in early 2027, a 150 basis-point shift. This broad range of expectations does not demonstrate the failure of the new strategy; many different conclusions can be drawn about an inherently uncertain economic future. But it does indicate that reducing the quantity of communications does not automatically translate into greater clarity of message. Simply dropping sterile and well-worn phrases may leave the underlying communication policy hidden in plain sight. When the Fed chair explains less about the factors driving his policy response to economic developments, each adverb and adjective carries more weight. What is left unsaid or expressed imprecisely may have large market consequences.

An April 2024 survey by the Brookings Institution of 29 Federal Reserve watchers asked whether the new chairman should continue to hold press conferences after every meeting; 83% responded “yes.” When asked whether they found the dot plot useful, 56% responded either “useful” or “very useful,” while 19% responded that they “didn’t use it at all.” More tellingly, only 56% indicated they “had a clear or mostly clear view of the Federal Reserve’s likely future reaction to changing economic data, down from 66% in April and 80% in October 2021.” Those are the views of professionals, not of the general public, but even this small sample reveals the fundamental problem with the earlier framework: the Fed produced an abundance of communications, yet a significant fraction of its closest observers could not form a consistent understanding of how its policies would respond to evolving economic conditions.

The solution, therefore, is not simply to revert to old practices and reinstate every past press conference, every speech, every dot. It is to keep the channels that support accountability and shed the ones that appear to commit future actions. The press conference following every policy meeting ought to continue. That forum is an indispensable tool for explaining votes and decisions, presenting economic interpretations and answering direct questions about prevailing risks. The Fed should rein in excessive commentary by regional Fed presidents and other officials who tend to add little to the debate beyond their own interest rate predictions. And the dot plot should be either fundamentally restructured to avoid offering the illusion of certainty or placed within an entirely different, clearer framework. It could display ranges rather than single points, connect forecasts of policy to underlying economic assumptions and offer a more honest accounting of forecast uncertainty. The quarterly economic report proposed by former Fed Chairman Ben Bernanke in early 2025 embodies such a structure, offering a shared framework and alternatives.

Critics of this approach might suggest that less forward-looking guidance will increase risk premia and thus raise borrowing costs for consumers and businesses. That is indeed a real possibility. A central bank that does not share its detailed reasoning could reduce transparency for borrowers, leading to difficulties in pricing instruments like corporate bonds, home mortgages and bank loans. But the old, highly explicit, approach also had costs: it gave rise to overtrading on minute shifts in language, lent an outsized importance to individual dots in policy projections and turned even necessary policy reversals into events that damaged credibility. The proper contrast is not between perfect transparency and strategic obscurity, but rather between disciplined communication and cacophonous communication. A disciplined framework could diminish uncertainty by improving clarity around policy objectives and likely responses, without revealing how individual interest rates are set on any particular date. The central bank’s ability to link its actions back to verifiable evidence is the most reliable foundation for its policy credibility.

Less Forward Guidance, More Proof

A more effective Fed communication policy would adhere to three habits, although these should probably not be presented as a formal rulebook. First, the central bank should repeatedly affirm its long-run objectives in clear, consistent language. Second, it should use its communication as an opportunity to lay out the evidential basis for each decision, especially at moments when inflation exceeds the target. Third, it should describe what sort of data shifts or new information would alter its assessment of the relevant risks, without pledging a specific action date or target for policy. This strategy would help households, businesses, financial firms and markets make informed decisions without inducing them to second-guess the chairman’s personal forecast of future developments. And this approach would protect the central bank from political influence: a central bank able to explain how its policy choices follow directly from economic developments is more resilient to allegations of politically motivated decision-making.

This framework should apply to decisions that exceed market expectations, too. When the Fed opts for larger policy adjustments than anticipated, the explanation accompanying the decision should clarify the immediate trigger: whether the action was prompted by new data on price pressures, emerging risks to financial stability or revised thinking on the restrictiveness of policy. An announcement of an unexpectedly larger policy change warrants explanation because the magnitude of the market’s response is so sensitive to it. Any message needs to be forceful and unambiguous regarding why tighter monetary policy is now necessary and on what basis, but it also must avoid giving the impression that the outlook for inflation and interest rates is now entirely certain or static. Decisive action is most powerful and effective when it is supported by evidence that can be verified or refuted.

The tenfold variation in market responses demonstrates precisely why both the extremes of the old communication strategy-both over-messaging and its flip side of tactical silence-must be avoided. Central-bank communications do not just reflect policy; they help shape policy itself by conditioning the context in which a given policy action is taken. Warsh has made the right choice in signaling-in the parlance of transportation-the loss of the turn signal when the road is uncharted and unpredictable. What he should not do is dismantle the road map. The Fed should reduce its forward promises and its tendency to communicate merely for the sake of being heard. However, when it acts, the case it presents regarding the objective and the evidence must be impeccable. A quieter Federal Reserve can be a stronger Federal Reserve, but that standard is high and demanding; it entails discipline over noise and evidence over projection.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Ahmad, S. and Wessel, D. (2026) ‘Grading Fed communications: A 2026 survey of Fed watchers’, Brookings Institution, 8 May.

Bauer, M.D., Pflueger, C.E. and Sunderam, A. (2024) ‘Perceptions about monetary policy’, The Quarterly Journal of Economics, 139(4), pp. 2227–2278.

Bernanke, B.S. (2025) Improving Fed Communications: A Proposal. Hutchins Center Working Paper No. 102. Washington, DC: Brookings Institution.

Board of Governors of the Federal Reserve System (2026a) Federal Reserve Issues FOMC Statement, 17 June. Washington, DC: Board of Governors of the Federal Reserve System.

Board of Governors of the Federal Reserve System (2026b) Statement on Longer-Run Goals and Monetary Policy Strategy. Reaffirmed effective 27 January 2026. Washington, DC: Board of Governors of the Federal Reserve System.

Chavez-Dreyfuss, G. (2026) ‘US bond market expects rate hikes the Fed may never deliver’, Reuters, 25 June.

Delaney, S. (2026a) ‘From a predictable Fed to a market-responsive Fed: A price stability doctrine unshaken by short-term shocks’, The Economy, 19 June.

Delaney, S. (2026b) ‘Chair Warsh removes the “turn signal,” adopting the playbook of the Greenspan Fed’, The Economy, 22 June.

Ehrmann, M. and Hubert, P. (2026a) The Overdelivery Premium: When Monetary Policy Decisions Exceed Market Expectations. CEPR Discussion Paper No. 21241. London: Centre for Economic Policy Research.

Ehrmann, M. and Hubert, P. (2026b) ‘When central banks over-deliver, markets listen differently’, VoxEU, 25 June.

Jarociński, M. and Karadi, P. (2020) ‘Deconstructing monetary policy surprises: The role of information shocks’, American Economic Journal: Macroeconomics, 12(2), pp. 1–43.

McGeever, J. (2026) ‘Markets hear Greenspan echo as Warsh Fed goes quiet’, Reuters, 23 June.

Nakamura, E. and Steinsson, J. (2018) ‘High-frequency identification of monetary non-neutrality: The information effect’, The Quarterly Journal of Economics, 133(3), pp. 1283–1330.

Ragusa, G., Gürkaynak, R.S., Motto, R. and Altavilla, C. (2020) ‘Financial market reactions to monetary policy signals’, VoxEU, 3 August.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.