[Warsh Fed] “From a Predictable Fed to a Market-Responsive Fed”: A Price Stability Doctrine Unshaken by Short-Term Shocks

Siobhán Delaney is a Dublin-based writer for The Economy, focusing on culture, education, and international affairs. With a background in media and communication from University College Dublin, she contributes to cross-regional coverage and translation-based commentary. Her work emphasizes clarity and balance, especially in contexts shaped by cultural difference and policy translation.

Authored On

Modified

Hawkish Rate Hold at First FOMC Meeting Under New Chair Comprehensive Review of Communication, Balance Sheet, and Inflation Framework Fed Takes a Scalpel to Its Policy Framework, Shifting Focus From Forecasts to Real-Time Conditions

Federal Reserve Chair Kevin Warsh upended the market’s traditional interpretive framework at his first Federal Open Market Committee (FOMC) meeting since taking office. While forcefully reaffirming the central bank’s commitment to price stability, he refused to pre-commit to a future interest-rate path and openly distanced himself from both the dot plot and forward guidance. The approach suggests a framework in which the inflation target remains fixed while policy tools are determined by evolving economic conditions.

“The Dot Plot Is Written in Pencil With an Eraser”

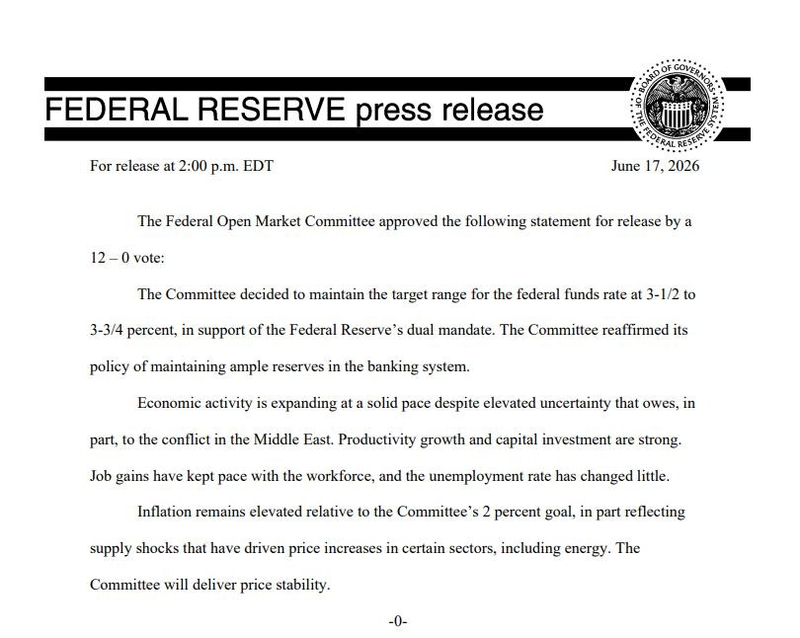

According to CNBC and MarketWatch on June 18, the Federal Reserve unanimously voted during its June 16–17 FOMC meeting to maintain the federal funds rate at 3.50%–3.75%. The decision marked the fourth consecutive pause following meetings in January, March, and April. In the first FOMC meeting chaired by Warsh, all 12 voting members supported holding rates steady. In its statement, the Fed noted that “inflation remains elevated relative to the Committee’s 2.0% objective” and said the situation partly reflected supply shocks stemming from price increases in specific sectors, including energy.

Markets began reacting as Warsh’s press conference and updated economic projections were released. According to CNBC, Warsh referenced “price stability” more than a dozen times during the roughly 43-minute press conference, delivering a distinctly hawkish message. The tone contrasted with his previous remarks prior to taking office, when he had repeatedly suggested the possibility of rate cuts. “Our commitment to achieving price stability is strong, unanimous, and unambiguous,” he said.

At the same time, he avoided specific and direct comments regarding the future path of interest rates. Most notably, he declined to submit his own dot plot projection, which reflects policymakers’ rate expectations. While he said he encouraged colleagues to submit their forecasts in keeping with institutional practice, he personally chose not to do so based on principle. Describing the Fed’s dot plot as “written in pencil with an eraser,” Warsh argued that the projections are inherently subject to change.

Traditionally, the Federal Reserve has published dot plots after FOMC meetings to indicate where policymakers expect interest rates to stand at future points in time. The rationale has been that transparency enhances policy predictability and effectiveness. Warsh, however, views the dot plot as a constraint on policy flexibility. Long critical of the practice, he remarked that “the Fed has spoken too much publicly about its interest-rate outlook.”

Forward Guidance Abandoned After 15 Years

Warsh also made clear that he intends to scale back forward guidance. He believes it has contributed to market confusion by encouraging policy reversals following failed inflation forecasts. In his view, markets should respond to actual economic data rather than attempting to anticipate the Fed’s next move. He argued that when market pricing merely reflects Federal Reserve rhetoric, policymakers themselves lose access to valuable information.

Forward guidance was first introduced under former Chair Alan Greenspan in May 1999, when the dot-com bubble was approaching its peak. It was used only intermittently until becoming a permanent feature of FOMC statements under former Chair Ben Bernanke in 2011 following the global financial crisis. The goal was to reduce uncertainty surrounding inflation. Bernanke also introduced regular press conferences that year and began publishing the dot plot in January 2012. His communication strategy represented a dramatic departure from the Greenspan era, when even rate decisions were not routinely disclosed. That approach continued through the tenures of former Chairs Janet Yellen and Jerome Powell before Warsh shifted direction.

Warsh first joined the Federal Reserve in February 2006 as its youngest governor and departed in March 2011, shortly before press conferences and forward guidance became institutionalized. Following this month’s FOMC meeting, he explained that “the policy statement has become somewhat more concise and certain outdated language has been removed,” adding that forward guidance was excluded because he deemed it inappropriate for the current policy environment. There is precedent for forward guidance sending misleading signals. In 2021, former Chair Powell confidently described inflation as “transitory,” only to later implement aggressive rate hikes known as “giant steps,” dealing a significant blow to the Fed’s credibility.

Macroeconomic theory generally divides monetary policy into rule-based and discretionary approaches. For decades, academics and markets have favored rule-based frameworks on the grounds that central bank credibility rises when policymakers adhere consistently to predefined principles and objectives. Discretionary approaches, in contrast, have often been criticized for reducing predictability and undermining confidence. Warsh, however, is attempting to combine the two. While emphasizing price stability as a firm rule, he simultaneously argues against precommitting to a rate path. The inflation objective remains fixed, but the policy tools used to achieve it will depend on prevailing economic conditions. His refusal to submit a dot plot and his retreat from forward guidance reflect the same philosophy.

A Communication Strategy With Fewer Hints

Warsh did not signal an imminent rate hike. He stated that only one proposal was discussed at the meeting and that “none of the 19 participants” believed a rate increase or even a warning of one was necessary. While the dot plot shifted in a more hawkish direction, he stressed that no rate hike has been predetermined for the July meeting or any other near-term gathering. “We will meet again in six weeks,” he said, reiterating that future decisions will depend on incoming data.

Another defining feature of the Warsh era is a comprehensive review of the Federal Reserve’s operating framework. On June 17, he announced the creation of five task forces as his first formal reform initiative since taking office. The groups will focus on five areas: the Fed’s policy communication framework, balance-sheet management, economic data collection and utilization, the impact of emerging technologies such as artificial intelligence on productivity and labor markets, and the Federal Reserve’s inflation policy framework.

These initiatives reflect priorities Warsh identified before assuming office as core reform objectives. The most closely watched is the balance-sheet task force. Warsh has long argued that the Fed’s asset holdings, which expanded to approximately $6.7 trillion through successive crises including the global financial crisis and the pandemic, distorted market price formation and excessively expanded the central bank’s role. The task force will reexamine from first principles the appropriate size of the balance sheet and the framework for quantitative tightening (QT).

The data task force will conduct a comprehensive review of the economic indicators and analytical systems used in policymaking. Warsh has argued that traditional statistics alone are insufficient to capture the realities of a rapidly changing economy and that policymakers should make greater use of real-time data and new analytical techniques. The AI and productivity task force will examine how the spread of artificial intelligence affects productivity, labor markets, and long-term inflation, and how those effects should be incorporated into monetary policy. Warsh has consistently maintained that AI will boost productivity and ultimately exert a disinflationary effect by lowering the cost of goods and services.

The communications task force will redesign how the Federal Reserve communicates policy. Warsh stated that “press conferences are an effective communication tool, but they are most appropriate when there is important news to convey.” The inflation framework task force will reassess how the Fed measures inflation and formulates policy decisions. Warsh believes the central bank’s role is not to reassure markets or support asset prices, but to maintain price stability.

That philosophy is also reflected in his remarks on inflation. During the press conference, Warsh rejected suggestions that the Fed might reconsider its 2% inflation target. He argued there is no reason to revisit the target until the Federal Reserve has reestablished both its commitment and its ability to achieve it. He also reaffirmed his longstanding view that “inflation is primarily determined by monetary policy” and that “inflation is a choice.” The statement reflects a belief that long-term inflation trends are ultimately shaped by central bank policy decisions.

Recent developments in energy markets illustrate the point. International oil prices surged following disruptions linked to the Iran conflict and the closure of the Strait of Hormuz, but the critical question remains whether the shock proves persistent. Expectations of increased supply have also emerged, driven by the possibility of the United Arab Emirates’ withdrawal from OPEC and a resumption of Iranian crude exports. If the conflict is resolved quickly and maritime shipping returns to normal, upward pressure on energy prices could gradually ease. Should the energy shock fail to evolve into sustained inflation, the need for additional monetary tightening would diminish accordingly. Under that scenario, market expectations for further rate hikes this year, which strengthened immediately after the June FOMC meeting, could also be revised.

Siobhán Delaney is a Dublin-based writer for The Economy, focusing on culture, education, and international affairs. With a background in media and communication from University College Dublin, she contributes to cross-regional coverage and translation-based commentary. Her work emphasizes clarity and balance, especially in contexts shaped by cultural difference and policy translation.

Similar Post