The Global Energy Shock Is Not a Fixed Fate

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

The 2026 Hormuz shock turns a regional war into a global energy shock The article shows why global shocks hurt more, but not forever Trade shifts buy time; technology reduces future exposure

A single maritime route has revealed the rapid expansion of an energy crisis beyond its area of origin. Once the Strait of Hormuz was effectively sealed off in early 2026, the net reduction in oil supplies was calculated at some 12 mb/d, or about 11 percent of the pre-war global supply. This is not a domestic shortage with distant spillovers. It is a world energy price shock embedded in transport, food, chemicals, power and credit costs simultaneously. Yet the magnitude of the initial blow should not be over-interpreted as a full measure of eventual costs. Markets move, firms switch between types of fuel, buyers replace suppliers, governments release stockpiles and higher fuel prices accelerate technological adaptation. The pertinent policy issue, therefore, is not whether a global energy crisis can be avoided after it is initiated, but how rapidly nations can differentiate outcomes.

Why This Global Energy Shock Is Different

The European crisis of 2022 was severe. Its first form was regional. Russia reduced pipeline gas flows into a market that had built capital, heating systems and power prices around that flow. Europe experienced the greatest price increase, while many non-regional producers enjoyed a cost advantage. That differential mattered. European firms could import some lower-priced goods, put more money into other fuels and find time to shift some manufacturing offshore. The 2026 impact proceeds along a second axis. Hormuz is a critical route for oil, LNG and refined products. When flows go down through it, the world's importing regions, Asia, Europe and others, compete to acquire identical replacements for those cargoes. Costs for ships and insurance climb in concert. Energy-intensive imports no longer provide the same relief because their makers also incur additional costs. The impact, therefore, spreads through energy costs as well as traded goods prices.

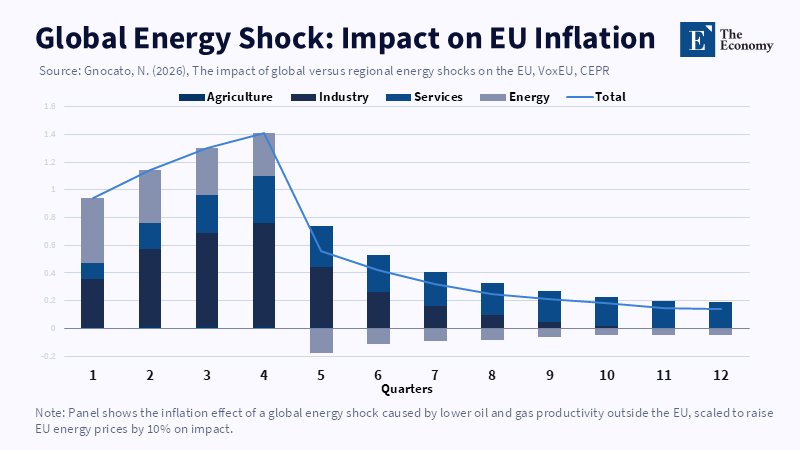

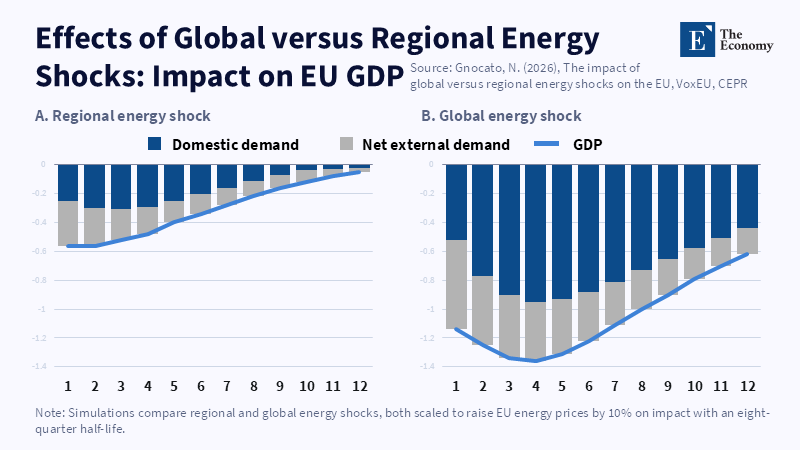

Model results illustrate these differences. Setting a regional and a global shock to increase the EU energy price by 10% at the outset, the latter produces far more imported inflation. The non-energy contribution to peak inflation averages around 1.1 percentage points with the global shock, against around 0.2 percentage points with the regional shock. Output also declines more because of a simultaneous foreign slump and because a fall in domestic household income and investment reduces supply. A separate ECB estimate finds that a geopolitical oil shock that raises the real oil price by 10% can slow euro-area GDP growth by 0.2 to 0.3 points over the first three years. All this describes the initial risk accurately. It indicates why a global energy shock cannot simply be read as a rerun of 2022 with a different geography.

The Missing Variable Is Economic Adaptation

The weakness emerges later. Short-term models tend to take for granted that oil and gas are difficult to substitute away from and that flows of trade adjust only very gradually. That's fine for the first few months of a crisis. That assumption weakens as the time horizon extends. Europe's response after 2022 shows why. In 2021, Russian gas accounted for roughly 45% of EU imports, but by 2025 this had shrunk to about 12% and 152 bcm to 36 bcm respectively. Between August 2022 and January 2026, the EU's gas demand shrank 19%. This wasn't without pain. Industrial activity declined, households paid more and taxpayers bore substantial costs. But the feared physical shortage didn't take up residence in the economy. New LNG terminals, storage policies, contracts, lower demand and faster shift away from fossil power-all changed the shock's initial impact on the system.

It also changed the scale of the damage. One recent estimate suggests that the 2022 energy shock left euro-area energy efficiency about 3% higher than a no-shock trend pathway in 2026. Potential output was still approximately 0.8% lower, so adaptation did not render the crisis painless. However, the same research estimates that the output shortfall would have been approximately 1.3% if the efficiency response had been 80% lower. That difference is the gain from the adjustment. It captures firms transforming operations, cutting waste and aligning research with energy-efficient technologies. The implication is relevant to today's global energy shock. A model that assumes technology and fuel use remain close to their pre-shock values describes exposure, not the inevitable long-run outcome. Over time, the extent of the cost of the shock has depended on how rapidly resources, skills and policies transition to less energy-intensive production.

Europe's power system provides a second sign of that transition. In 2024, low-carbon sources supplied 47.5% of EU gross electricity consumption, compared with 28.6% a decade earlier. It does not, for example, protect it from the demand- and supply-side shocks of oil, which is still dominant in transport, aviation, farming and the petrochemical sector. It does, however, reduce one potent mechanism by which a fuel shock feeds into the headline cost of power. This is visible in 2026. Crude oil prices and a number of refined products were higher than in 2022. Wholesale power prices have moved by a margin that was slightly lower than in 2022, as the larger share of generation responded to this change by switching away from fossil fuels. A global energy shock, in other words, still ripples through to Europe, but it is now an economy with a different generation profile. Resilience is cumulative. The investment made after the last crisis will mitigate the next one.

Trade Redirection Buys Time, Technology Changes Exposure

Trade redirection is the quickest form of adjustment, although it has a ceiling. Emergency stocks of oil, spare capacity, extra ports and longer voyages all support a partial offset of a lost flow. Leading into March 2026, members of the IEA agreed to release 400 million barrels of emergency oil, the largest coordinated release in the agency's history. The two main Gulf producers, Saudi Arabia and the United Arab Emirates, diverted some exports to ports outside the Gulf, while American producers increased output and exports. Gas markets began a comparable process. Canada's first large LNG export terminal sent its first shipments in 2025, averaging full-year exports of 295 million cubic feet a day, all sent to East Asia. That volume is a trivial fraction of what would disappear with Qatari exports, but it demonstrates the larger truth. An importer counteracting a worldwide energy shock can still adjust routes, reschedule contracts and rebalance sources, even if no unaffected markets are available.

The redirection is, in most cases, mostly a redistribution of scarcity. It can shift fuel from one customer to another without increasing the aggregate supply. It can also generate a new dependence on a handful of exporters. Change in technology shifts the exposure itself. Electrified transport, heat pumps, efficient machines, storage and a stronger grid require less imported fuel for every unit of output. The distinction is crucial. A new LNG deal may guard a country against a single producer or a single chokepoint. It cannot insulate that country against the global gas price. A factory that reduces gas consumption by a third has altered the price transmission channel by which the shock arrives at its costs. This is why East Asia's response will be as important as its search for North American cargoes. A move away from Gulf LNG to Canadian or US LNG provides near-term relief. A transition towards clean power, storage and lower fuel use provides a durable form of insurance.

Prices will not always make the adjustment cleaner. The IEA has already pointed to some Asian power systems turning back to coal from gas because of high LNG prices. That step might keep the lights on, but it will add to emissions and create reliance on another imported fuel. It also makes clear why relying on markets alone cannot be enough. Businesses always react to the signals and systems built around them. If the grid is shaky, storage is rare and clean projects are held up in the approvals process, then the cheapest alternative is likely to be the last one that anyone would envisage. Good policy should not oppose that switch. It should determine which alternatives are available first. The goal is not to forecast a singular, inevitable course of action following a global energy shock. It is to increase the range of plausible options before the next crisis demands a quick choice.

Policy for a Global Energy Shock That Lasts

The first task is to isolate emergency protection from structural policy. Households in hardship and most key industries may encounter a short-term necessity for assistance in response to a spike in fuel and food prices. Wide-based subsidies and income-tax relief are a clumsy long-term compromise. They dilute the incentives for firms and households to save energy, bolster demand when supply is constrained and transfer the bill to the central government. EU support for energy between 2022 and 2024 implied a cumulative fiscal cost of approximately 2.2% of GDP. Repeating the practice in the event of a prolonged global energy shock would imply less cash for grids and storage, railways, building modifications and factory efficiency. Assistance should therefore be targeted, temporary and preferably gains-linked with its long-run objective of reducing fuel use. The aim is to avoid hardship without arresting the economy at the energy pattern that produced the hardship.

The second task is to combine trade and technology as one resilience policy. In the transition, Europe will need at least two sets of oil and gas suppliers, but also ports, interconnectors and coordinated purchasing rules, which will stop members from racing against each other. Strategic reserves should have not only the crude but also the refined products that get tight first. Meanwhile, public investment should hasten power grids, storage, clean generation and industrial retrofits. Long-term North American LNG contracts help address Gulf over-exposure, but an oversized fixed gas infrastructure would slow the detachment from world fuel prices. Contracts should be measured against demand reduction plans, not viewed as a policy in themselves.

One frequent concern is that cleaner supply chains introduce new vulnerabilities. Solar panels, batteries and grid hardware depend on a group of minerals and manufacturing capacity that is heavily weighted towards a handful of countries. It is a valid point of concern. But it is also a risk that does not make fossil-fuel dependence any safer-oil and LNG shipments also originate in concentrated producers, cross exposed sea lanes and have a globalized price that reaches consumer prices in a matter of days. Though clean technology has its own supply dangers, components can be warehoused, repaired, repurposed and sourced through a variety of channels. Once in operation, wind farms and solar plants require no daily shipment of fuel down the Strait of Hormuz. The right response, then, is not to replace one fixed reliance with an equally inflexible form of its own. It is to develop diversified supply directions, while decreasing the recurring fuel cost, which leaves Europe and Asia open to future conflicts.

The opening number is the warning: 12 million barrels per day disappeared from normal supply after one regional war trapped one narrow waterway. No reserve, no trade deal, no solar programme can erase that initial blow. The economic clock is not to be set at the instant the ships draw to a halt. It is to be set at the choices for the days that follow: economies that simply subsidize consumption will bear the shock longer; those that shift trade, reduce needs and accelerate innovation will still bear the burden, but a little less each year. A global energy shock is global at the point of impact. It does not need to remain a deficit at the scale of destruction. Policymakers need to pass one strict test now, whether the next shock meets a familiar economy or one that has learned how to depend less on the chokepoint that failed. That education must embark before a tranquil market makes the lesson easy to forget.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arce, Ó., Battistini, N., Bouabdallah, O., Lis, E. and Mohr, M. (2026) ‘A tale of two energy crises – initial conditions matter’, The ECB Blog, 3 June.

Bachmann, R., Baqaee, D., Bayer, C., Kuhn, M., Löschel, A., Moll, B., Peichl, A., Pittel, K. and Schularick, M. (2024) ‘What if? The macroeconomic and distributional effects for Germany of a stop of energy imports from Russia’, Economica, 91(364), pp. 1157–1200.

Baumeister, C. and Hamilton, J.D. (2019) ‘Structural interpretation of vector autoregressions with incomplete identification: Revisiting the role of oil supply and demand shocks’, American Economic Review, 109(5), pp. 1873–1910.

Canada Energy Regulator (2026) ‘Market snapshot: Canada’s natural gas production kept climbing in 2025’, Canada Energy Regulator, 20 May.

Chtatou, M. (2026) ‘Shockwaves from the Gulf: The Iran War and its impact on the global economy and energy markets’, Eurasia Review, 28 June.

European Commission (2026) REPowerEU – 4 years on. Brussels: European Commission.

Eurostat (2026) ‘2024: nearly 50% of EU electricity came from renewables’, Eurostat News, 14 January.

Gnocato, N. (2026) ‘The impact of global versus regional energy shocks on the EU’, VoxEU, 25 June.

International Energy Agency (2026) The Middle East and global energy markets: Key facts on the Strait of Hormuz, oil and gas markets, and the IEA’s response. Paris: International Energy Agency.

Lane, P.R. (2026) ‘Analytical perspectives on energy supply shocks’, speech at the Centre for European Reform, London, 13 May. European Central Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.