AI Chip Export Controls Must Buy Time, Not Promise Permanent Denial

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

AI chip controls can buy time, not permanent dominance Chinese substitution limits their long-term power That time must build U.S. and allied capacity

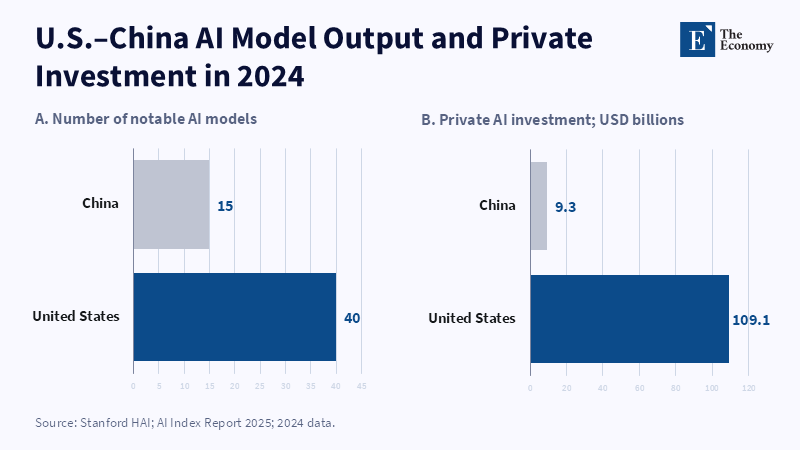

In 2024, U.S. institutions built 40 notable AI systems while China produced 15. Still, private AI investment in the U.S. was $109.1 billion, nearly 12 times China's $9.3 billion. That difference should be heartening and it isn't. A twelvefold lead in private funding coincided with only 2.7 times as many models. Meanwhile, Chinese models approach U.S. performance on several key benchmarks. The core conclusion is certain: the United States is far ahead in funding, processing capacity, chip design and allied chip manufacturing, but not forever. Export controls on AI chips should be viewed through a more demanding lens: not a mechanism to lock China in place or regain a diminished competitive market, but an investment in time and cost at the frontier and an effort with allied and partner attention fixed firmly upon what is created before that time expires.

AI Chip Export Controls Require a Well-Defined Time Scale

The debate makes export controls on AI chips appear to be a binary choice. On one hand, controls are hoped to cement U.S. dominance. Critics argue that controls will reduce sales, accelerate Chinese substitution and ultimately fail. Both camps are wrong. No export policy can force a major state to abandon a meaningful pursuit of strategically important technology. China's quest for self-sufficiency in semiconductors began long before the latest controls. The aim is not permanent denial. The goal is delay. An effective rule should raise the cost of frontier training, large compute clusters, high-bandwidth memory and advanced production. Delay is only effective if it is converted into new capacity. The value of a one-year delay diminishes if power grids are not expanded, chip production does not advance, research spending does not rise and allied policies do not advance.

This changes the right measures of success. China's market share is no longer a good scorecard. Chinese policymakers have strong incentives to favor domestically made chips even if foreign chips outperform them. Also, the certainty of Chinese reliance on U.S. chips under shifting U.S. licensing rules is no longer compelling for Chinese companies. Strategic effects of AI chip export controls can be measured with a small set of rule-of-thumb outcomes: the estimated time-to-frontier-scale training reduction, the cost of building models without restricted systems, the speed of Chinese domestic production, the growth of U.S. and allied computing and the extent of diversion through third countries. Such numbers will always be estimates, but they can still be measured. The real question is whether each year of constraint yields more secure computing, more electric power, more high-bandwidth memory, better implementation and more reliable allied supply. If the answer is no, then the controls are simply an expensive pause rather than an effective policy.

A transparent system would also discipline Washington: controls have too often swung back and forth between restrictions and exemptions and back again, confusing the target countries, harming U.S. firms and reinforcing Chinese fears that access can be withdrawn at will. Transparency need not equal leniency. It is about having clear and consistent thresholds and explaining the security rationale behind them while applying them consistently over time; it also involves a decision to uncouple frontier equipment from commodity goods or to at least limit controls to the specific processing power, memory bandwidth, I/O speed and cluster size that come into play in training advanced AI systems, as well as in missile and military applications. Rules that apply to hundreds of products weaken oversight and encourage estrangement; narrow AI chip export controls are more intelligible because they provide clarity about what is being protected and why.

The Compute Lead Is Real but Not Secure

The U.S. remains dominant in the global AI system, but there is considerable unevenness in this dominance. According to the 2025 Stanford AI Index, 40 prominent U.S. models were published in 2024, in contrast to 15 from China; the index put U.S. private AI funding at $109.1 billion against $9.3 billion in China, indicating a significant lead in finance and frontier development. These figures also show that capital does not easily translate into a proportional gap in output, with Chinese models closing the gap in performance on a range of benchmark tests. China was also the global leader in generative AI patenting activity 2014–23, with 38,500 patent families compared with some 6,300 in the U.S., although patent leadership does not necessarily indicate quality, commercial applications, or strategic importance. Yet no matter how impressive this six-fold filing rate is, it provides evidence for a broad and active technical base.

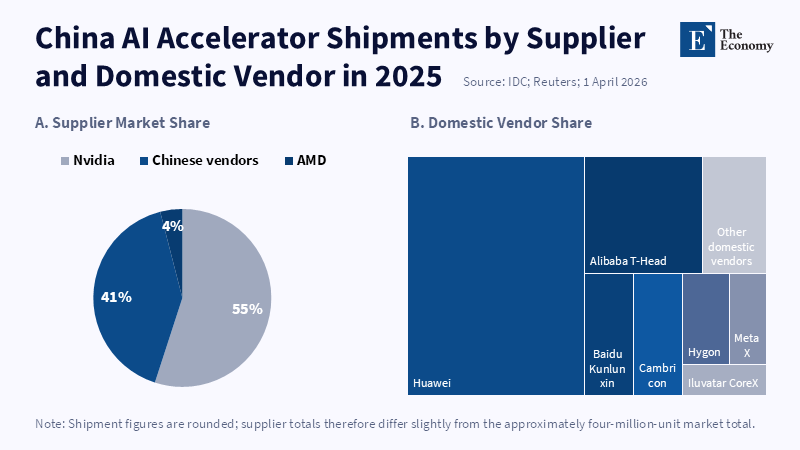

The deeper U.S. advantage lies further down the stack in access to advanced accelerators, high-bandwidth memory, electronic design automation (EDA) software, foundry services, cloud investment and a strong ecosystem of allied suppliers. Those can't easily be replaced en masse. A chip doesn't deliver frontier compute unless it's assembled with high-speed memory and interconnects, software, cooling, power and datacentre engineering to connect thousands of chips. Shipment counts can therefore mislead. In 2025, Chinese vendors supplied roughly 41 percent of the GPU cards shipped in China.

That distinction underpins targeted AI chip export controls; it also offers a caveat against overconfidence. China has demonstrated its skills in adapting models around limited hardware. It can scale up to more chips, optimize software, cut precision, split up tasks, or localize models for the available accelerators. These measures do not compensate for hardware constraints, but they do weaken their power. The same trend applies to production. Restrictions on the most sophisticated equipment can hamper yields and make outputs more expensive, but firms can compensate by manufacturing with older equipment, taking a larger number of steps and raising their costs. There is no outright barrier in this approach; rather, it amounts to a penalty on speed, scale, energy and reliability. This penalty is strategically useful and it can diminish as engineering advances. The strategic value of AI chip export controls, then, hinges on the cost advantage declining no more slowly than Chinese firms can adapt.

Strategic Substitution Changes the Test of Success

Chinese substitution is often cited as evidence that controls have failed. That is a hasty judgment. Substitution can occur, but not as quickly or cheaply as it would without controls. Domestic chips may be more power-intensive, require more units, produce lower yields, have less useful software, or slow down training cycles. If controls are successful, that is a real cost. Whether that cost is sufficiently high and lasts long enough to matter is another matter entirely. Based on this, it is understandable that controls are strongest against advanced manufacturing tools as opposed to every chip possible. Small chips are only easier to divert in large quantities through covert channels. Larger-scale hardware is more difficult to transport, install, maintain and cover up. Control measures should therefore consider that physical principle rather than attempting to control every single echelon of the supply chain.

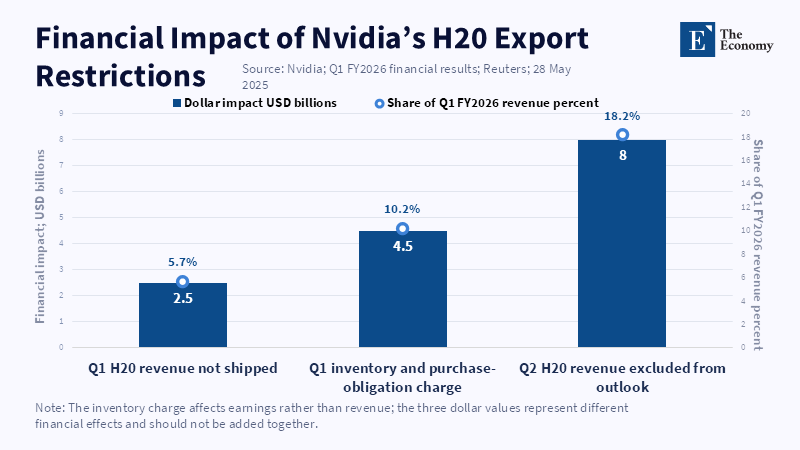

The commercial impact is very real, too. H20 restrictions on NVIDIA's sales in the first quarter of fiscal 2026 resulted in $4.5 billion in inventory and purchase commitments. The company has also announced that it was unable to ship a further $2.5 billion in H20 revenue and expects an impact of $8 billion in the following quarter. In the commercial world, that sort of loss cannot be brushed aside. Revenue is the funding upon which research, software, hiring and future chip generations depend. A policy that prevents U.S. companies from accessing a huge market, while at the same time permitting Chinese chip manufacturers to grow and sell abroad, could very well hit the very advantage it is trying to maintain in the first place. But the answer is not an across-the-board reopening. Low-end chips would not solve China's substitution model. Beijing's worry is not only performance: it's also dependence on the supplier empowered by a global adversary.

The better approach is to limit damage beyond China. Controls should remain strict at the frontier and be lighter in markets where the security argument is weak. Third countries should not be subjected to a confusing maze of sliding caps that encourage cloud providers, developers and states to lean on Chinese offerings. Partners should have clear access in return for strong end-use monitoring, customer screening and enforcement cooperation. That is not a call for unconditional alignment. Nations have their own companies, legal precedents and trade sensitivities. They also have control of vital sections of the semiconductor chain. Dutch lithography, Taiwanese foundries, South Korean memory chips, Japanese chemicals and U.S. design tools all form an integrated manufacturing system. Washington cannot pursue an effective policy by dictating commands to that system from one capital. Instead, the rules have to be established with the states that bear the policy's commercial and political costs.

Substitution establishes a second race outside of China. Chinese platforms and chips need not reach the frontier to win global dissemination; they can do so by price, open access, operational simplicity, state financing and fewer political conditions. Narrow differences in the model market share might be relatively inconsequential to a rural clinic, factory, credit union, or government service compared to lower-cost access. Should U.S. regulation make lawful access prohibitively costly or difficult in middle-income markets, Chinese platforms could become the clear default. Export controls for AI chips must secure frontier capacity, not turn the rest of the world into a licensing maze.

Transform AI Chip Export Controls into an Allied Capacity Plan

Policy must then evolve from there should not be any delays to every delay should emerge into a measurable enhancement of U.S. and allied capacity and this requires crossing the boundary between subsidies for fabrication facilities and capabilities, because the nature of advanced AI is such that AI systems will need power, transmission lines, transformers, cooling units, memory, packaging and delivery systems, technical workers, money for research labs and secure clouds capacity. A manufacturing strategy that ignores memory will build incomplete plants. A security strategy that ignores global demand will leave space for less costly but more competent rivals and thus the export controls on AI chips must be part of a master plan with clear targets for power generation, grid links, advanced packaging, high-bandwidth memory, worker training and secure-trust clouds. The controls merely buy time, which the capacity plan will establish whether it possesses intrinsic worth.

The same should apply to enforcement. More restrictions do not mean better monitoring. Smuggling increases with a rising price difference and weak controls. Governments should shell agencies and other intermediate entities, freight routing, cloud leasing and abnormally discrete bunch buying. Chip firms can share data to flag high-risk orders without turning every device into a monitoring instrument for enablement agencies. Customs agencies require technical staff able to capture the covered configurations. Partners require equal access to the risk data. Penalties should be toughest for major diversion networks, not small firms caught by unclear rules . A focused system will, in any case, leak; the objective is to keep the level of leakage below what is necessary for a continuous entry for the gradient training plan, without imposing such a broad compliance burden that the business struggle doing legitimate work.

The final condition is candor. These export controls on AI chips cannot ensure U.S. dominance; they cannot halt Chinese research, wipe out a national industrial strategy, or prevent all foreign access to computing. They can raise costs and slow access to the largest, most powerful systems. That is useful but limited leverage. An honest assessment of that leverage might actually be good policy: it would outline how much delay was achieved, how much leakage occurred and how much capacity was created during a planned cycle. If the United States continues to lag in new U.S. factories, nuclear power stations, memory lines and allied agreements, though, then tighter controls will not merely be necessary, but also insufficient.

The initial figures should stand as a warning. A country with almost twelve times the private AI investment generated only 2.7 times as many market-relevant models in 2024, even while its main rival led by a significant margin in generative AI patent volume. The U.S. has the more robust compute foundation, but the knowledge gap is now close enough to penalize delay and bad policy. AI chip export restrictions are justified when they safeguard the small handful of assets that still impose a hard frontier constraint. They are counterproductive when they substitute for investment, alienate allies or cut U.S. companies off from global demand. The point is not to defend a market that may now be politically sealed. It is to translate fleeting hardware superiority into permanent capability. Each month bought by a control should show up elsewhere as a new fab, a more resilient grid, a safer cloud, a deeper skills base, or a more dependable alliance. Otherwise, time will be wasted.

This article is based on an original research article published by The Economy Research. For the original version, please refer to Frontier Compute, Export Controls, and Strategic Substitution in U.S.–China AI Competition.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Baptista, E. (2026) ‘DeepSeek-V4, the Chinese AI model adapted for Huawei chips’, Reuters, 24 April.

Bureau of Industry and Security (2024) ‘Commerce strengthens export controls to restrict China’s capability to produce advanced semiconductors for military applications’, U.S. Department of Commerce.

Gupta, R., Walker, L. and Reddie, A.W. (2024) ‘Whack-a-Chip: The futility of hardware-centric export controls’, arXiv.

Liu, J. and Lee, J.-A. (2026) ‘Strategic stalemates: The paradox of export controls in the U.S.–China AI race’, arXiv.

MacCarthy, M. (2026) ‘Ball game’s over—the US is out of the AI chip market in China’, Brookings Institution, 17 June.

Maslej, N., Fattorini, L., Perrault, R., Gil, Y., Parli, V., Kariuki, N., Capstick, E., Reuel, A., Brynjolfsson, E., Etchemendy, J., Ligett, K., Lyons, T., Manyika, J., Niebles, J.C., Shoham, Y., Wald, R. and Clark, J. (2025) Artificial Intelligence Index Report 2025. Stanford Institute for Human-Centered Artificial Intelligence.

NVIDIA Corporation (2025) ‘NVIDIA announces financial results for first quarter fiscal 2026’, NVIDIA Corporation, 28 May.

Office of the United States Trade Representative (2024) Four-Year Review of Actions Taken in the Section 301 Investigation: China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation. Washington, DC: Executive Office of the President.

Pan, C. and Chen, L. (2026) ‘Chinese chipmakers claim nearly half of local market as Nvidia’s lead shrinks’, Reuters, 1 April.

Semiconductor Industry Association (2025) 2025 SIA Factbook. Washington, DC: Semiconductor Industry Association.

Wang, J., Kunievsky, N., Lou, B., Sun, T. and Evans, J. (2026) ‘U.S. policies unintentionally accelerated China’s open AI ecosystems’, arXiv.

World Intellectual Property Organization (2024) Patent Landscape Report: Generative Artificial Intelligence. Geneva: WIPO.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.