[EU vs. China] Beyond Import Shares: A Risk-Based Framework for EU Trade Dependence on China

Published

1 The Economy Research, 71 Lower Baggot Street, Dublin 2, Co. Dublin, D02 P593, Ireland

2 Swiss Institute of Artificial Intelligence, Chaltenbodenstrasse 26, 8834 Schindellegi, Schwyz, Switzerland

European research on trade dependence often treats high import shares as evidence of strategic vulnerability. However, this article finds that the relevant risk is narrower and more structural. It uses the concept of import vulnerability at the product level alongside the Substitution Difficulty Index and an industrial-criticality filter to distinguish exposure from adaptive capacity and to map the resulting risks onto policy-relevant categories. Import concentration alone cannot determine the severity of trade dependence, which also depends on inventories, latent suppliers, product substitutability, switching costs, domestic production networks, and changes in global supplier concentration. These categories support differentiated policy responses, from monitoring to supplier diversification for vulnerable and substitutable imports, industry preparedness to conditional industry support for less flexible imports and strategic stockpiling or allied co-production for the most system-critical dependencies. The empirical application to the European Union's trade with China reveals that system-critical vulnerability is currently limited to a few value-added system-enabling products; a broad decoupling is unnecessary and the strategic objective should be selective de-risking.

1. Introduction - From Trade Exposure to Strategic Vulnerability

European debate on economic security has moved quickly since 2023, but the analytical core of that debate remains underdeveloped. The principal public indicators Europe uses for exposure to China are still bilateral trade deficits, headline import shares, or politically salient data related to a few consolidated industries. They are fine for describing commercial magnitude. They are not good measures of strategic risk. A large import flow may be commercially significant yet readily replaceable. A much smaller flow may sit at a narrow chokepoint in an industrial chain and carry a materially larger systemic risk. The European Union's economic problem with China is not a generalized dependency across its overall import structure. It is a more precisely targeted kind of dependency in those details of products where supplier concentration, substitution difficulty and downstream industrial importance all align. That is the point beyond which a trade flow becomes a question of strategic resilience, readiness, and in limited cases, strategic autonomy.[1]

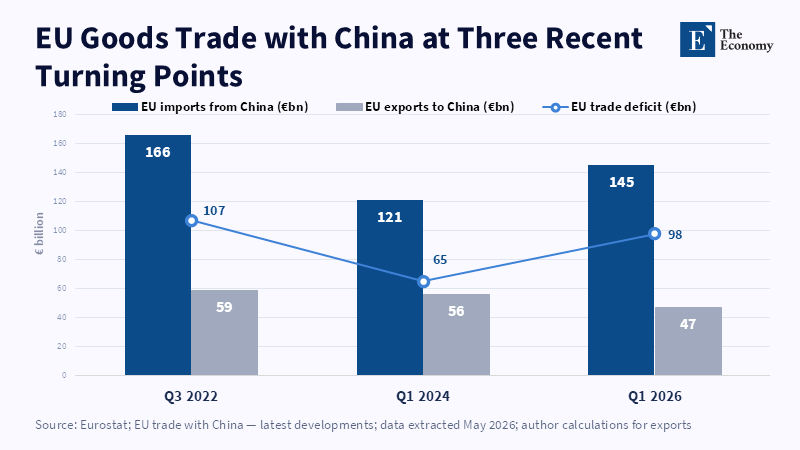

The pressing need for that differentiation became acutely apparent in 2023-2026. While China remained the European Union's largest source of EU goods imports in 2025, accounting for 22.3 percent, the EU's goods deficit with China hit €98 billion in the first quarter of 2026, the highest quarterly deficit since the third quarter of 2022.[2] Simultaneously, more than half of the EU's high-tech imports in 2024 came from China and the United States combined, with China providing 30 percent of total extra-EU high-tech imports.[3] These aggregate numbers cannot alone dictate vulnerability, but they have made evident why a more discriminating diagnosis has become unavoidable under current economic-security circumstances.

Recent events have also shown that trade conflicts and supply risks cannot be reduced to a single political slogan or macroeconomic explanation. Since 2023, official EU policy has looked like a mixed set of concerns: Chinese export restrictions on some crucial materials; its own fears about distortion in battery electric vehicles and other growing industries; the Economic Security Strategy that frames supply-chain resilience as one of many kinds of risk. That history does not indicate a common cause for each EU-China trade discord, whether subsidies, exchange rates, or bilateral deficits. It does indicate a non-reducible policy need: a product-by-product analysis that reveals when dependence becomes a vulnerability policymakers can scarcely afford to overlook, like strategic stockpiling, industrial aid, restrictions on imports, or protection of investment.[4]

The central argument is that the EU should assess China-facing trade dependence through a layered diagnostic rather than through import shares alone. The first layer should identify whether a product is import-vulnerable. The second should assess whether it is difficult to substitute in practice, rather than merely in theory. A third filter should determine whether the product is system-enabling for wider industrial production, infrastructure or strategic technologies. Only if all of these conditions exist in a given product should the EU treat dependence as a strategic vulnerability. Such a conditional approach is conducive to de-risking without causing unnecessary decoupling, and it makes sense of how the EU might have different strategies for different products: reinforcing and stockpiling for a few, supplier diversification for many, and a strategic combination of measures for a very narrow list.[5]

That argument also corrects for two common mistakes in European policy debate. The first is to claim that all import concentration is automatically a source of strategic weakness. The second is to take any domestic or intra-European production as a sign of strategic strength. Neither assumption is justifiable in isolation. An import relationship as dominated as that for ethanol may be quite easily regulated if other sources are accessible, stocks can buffer disruptions, or the good is not systemically important. Meanwhile, domestic manufacturing may not add strategic robustness if the vital intellectual property, upstream inputs, or scale capacity remain external.[6] The real issue for EU policymakers is not to quantify the overall dependence on China, but to identify which product relationships entail economically significant risk under today's conditions of supply chain fragmentation, industrial competition, and periodic coercion.

2. Why import shares are insufficient

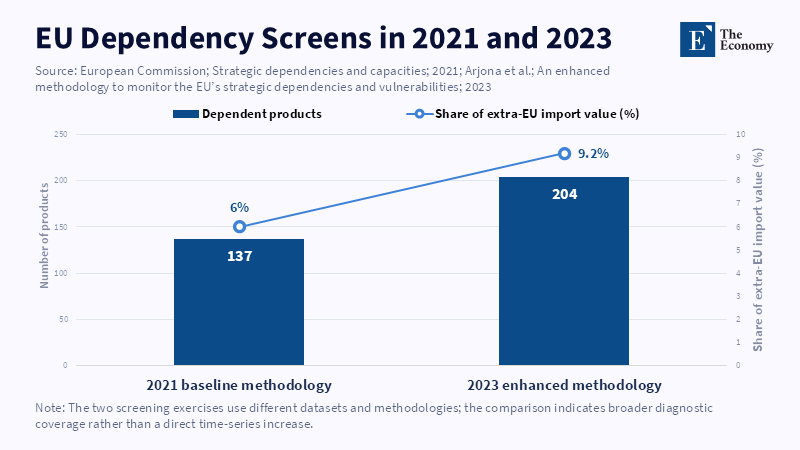

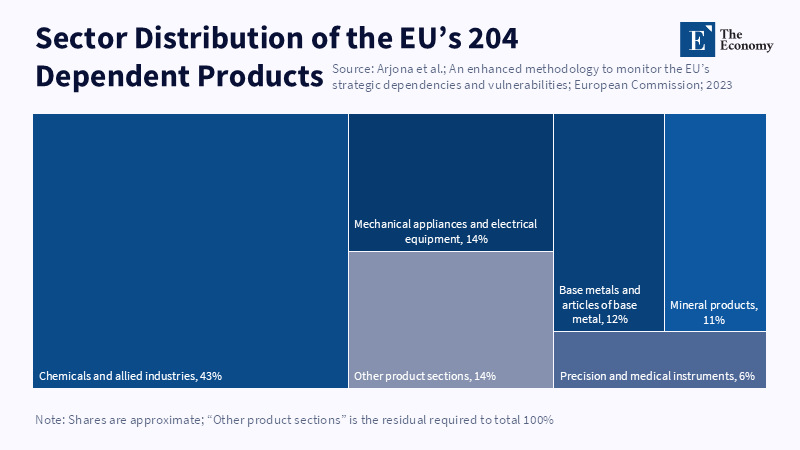

Import shares are descriptively powerful because they are simple. They show where the EU imports from and how much it imports. However, strategic vulnerability is not equivalent to commercial weight. The European Commission’s first screening exercise in 2021 identified 137 products in sensitive ecosystems for which the EU was highly dependent and those products represented around 6 percent of total extra-EU imports.[7] In 2023, the enhanced methodology reflected a more granular level of product data and incorporated network analysis to identify a total of 204 products in sensitive ecosystems that had high foreign dependence, including parts that could be exposed to single points of failure.[8] The conclusion is clear. The EU's strategic challenge is not excessive import dependence for most products. It is that a comparatively narrow slice of the EU's overall mix of imports can matter strategically.

This is confirmed by more recent evidence. A 2026 note by Commission economists identified 835 foreign-dependent products across five strategic ecosystems, accounting for 16 percent of EU import product lines and 17 percent of their value.[9] China was the primary supplier for 47 percent of those products and roughly half of their total value or €206 billion out of €404 billion.[10] Again, the evidence is selectively indicative of lower and higher-risk dependence: the growth in the number of dependencies is due to a broader coverage of ecosystems, using a multi-layer structural framework, not necessarily to an increase in higher-risk dependence on China. The analytical challenge is therefore to distinguish simple foreign dependence from dependence that is either impossible, excessively expensive, or very slow to break.

The failure of import shares to be informative flows from the economics of substitution. The Organization for Economic Co-operation and Development has made the case that trade dependence has analytical significance when three conditions occur in conjunction: high exposure to the risk of disruption, strategic or economic importance, and limited scope for diversification or substitution.[11] This formulation highlights the limitations of a large bilateral import flow. It indicates exposure, but not necessarily the risk of disruption; it indicates nothing about the availability of alternative suppliers; and it indicates almost nothing about how the disruption's impact might cascade through output, prices, or crucial services.

A second problem is that import shares are backward-looking snapshots of customs flows, whereas strategic vulnerability is a property of an economic system under stress. They do not measure inventories, contract duration, product heterogeneity, transport lead times, regulatory approvals, technical certification, switching costs inside production lines, or the capacity of buyers to redesign products if supply is interrupted. A product may look exposed on a customs ledger while remaining governable because buyers hold months of inventory and can switch suppliers with modest engineering changes. Another product may represent a tiny fraction of import value but be nearly impossible to replace because downstream equipment has been designed around specifications available from only a handful of suppliers worldwide. The policy error is to infer resilience or fragility from value shares before these mechanisms are examined.[12]

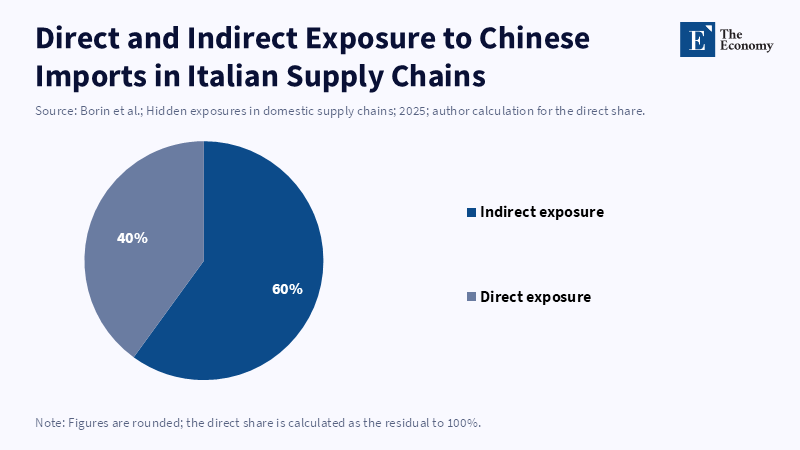

A third weakness of import shares is that they abstract from the domestic transmission structure. A supply disruption impacts not just the directly import-reliant firm, but also the surrounding domestic buyer-supplier network. A case study of Italy, exploiting firm-to-firm data cross-matched with customs information, demonstrates that the costs associated with imports from China were equivalent to 3.6 percent of its firms' costs, and around 60 percent of this supply shock was indirect, rather than direct.[13] Indirect exposure to Chinese imports exceeded direct exposure in roughly 90 percent of local labor markets.[14] Conventional international trade data therefore understate where external shocks land and by how much. If the EU relies solely on bilateral import shares to measure trade openness, it will miss the internal geography and sectoral distribution of external trade risk.

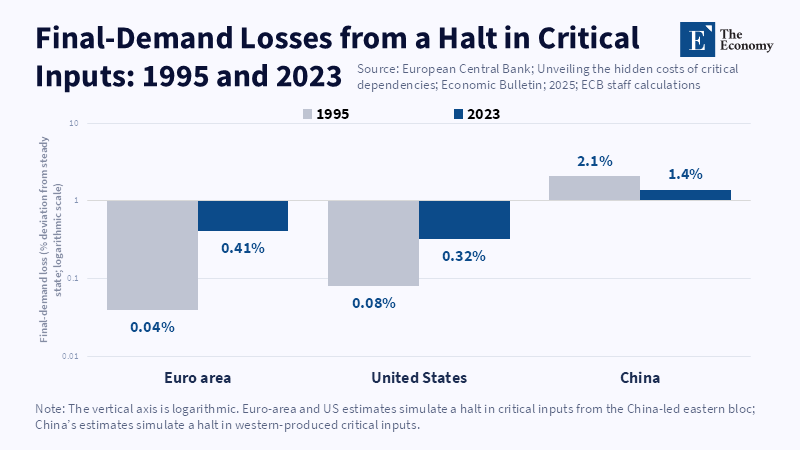

The macroeconomic evidence points in the same direction. The ECB's analysis of critical dependencies reports that in the euro area, supply risks are focused on a narrow group of narrowly diversified, low-diversification and low share of global supply, and in the European Union, a large number of strategically relevant items. In 2023, approximately 30 percent of the euro area's critical dependencies obtained from China may have been vulnerable to a single point of failure if export shares and network centrality are combined.[15] Most importantly, the ECB estimates that, in the event of a sudden stop of critical dependencies, the effect is disproportionate to the corresponding trade value: the loss in final demand is approximately twenty times that explained by the share of inputs lost. From 1995 to 2023, the euro area's estimated final-demand losses from a sudden stop of critical dependencies from the eastern bloc increased from 0.04 percent to 0.41 percent.[16] Those are not just import-share effects in the narrow customs sense. These are system effects arising from bottleneck inputs.

The composition of dependencies is also relevant. The Commission's early analysis revealed that 57 percent of the most foreign-dependent products were intermediate goods and 16 percent were raw materials, whereas final goods represented 27 percent.[17] And this matters because raw materials and intermediate goods tend to have broader downstream impacts. For example, a scarcity of a key raw material or industrial input can adversely affect various downstream industries simultaneously; by contrast, many final consumer goods with large import shares present a strategically lesser problem, because their disturbance is less apt to proliferate throughout entire production chains. This is precisely why the relevant indicator is not simply large imports, but large imports of system-enabling goods or small imports with large forward linkages.

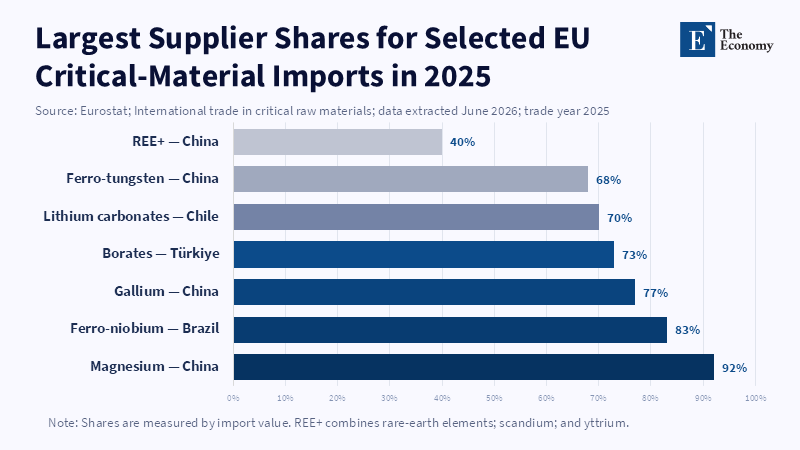

Examples of China-facing critical raw materials are particularly clear. According to Eurostat’s 2025 data, China made up 92 percent of EU imports of magnesium, and in the case of the EU’s imports of the two other critical raw materials, rare-earth elements, scandium and yttrium, sourced from China accounted for 40 percent by value and China was the main partner for 11 of 14 detailed product lines.[18] Critical raw materials imports are not just high or low. They are concentrated in a non-trivial way because the products are system-enabling in automotive, electronics, renewables, aerospace, or military. Eurostat also shows that a few critical raw materials have main suppliers that make up more than two-thirds of EU imports. This is, again, the same sort of concentration that importing value alone does not reveal.

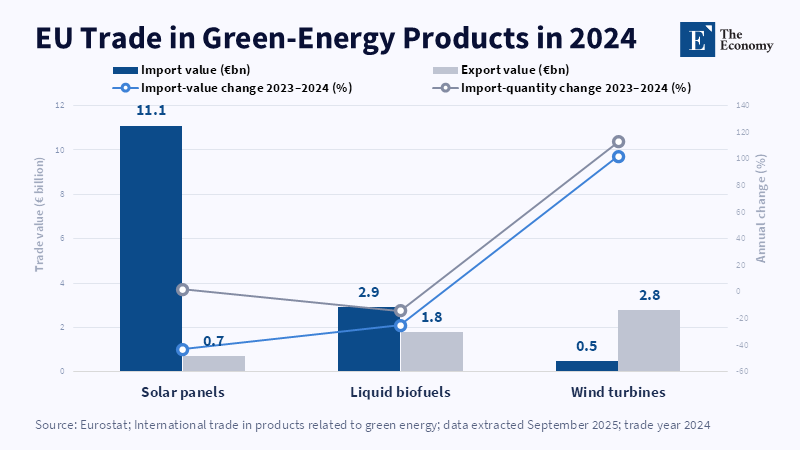

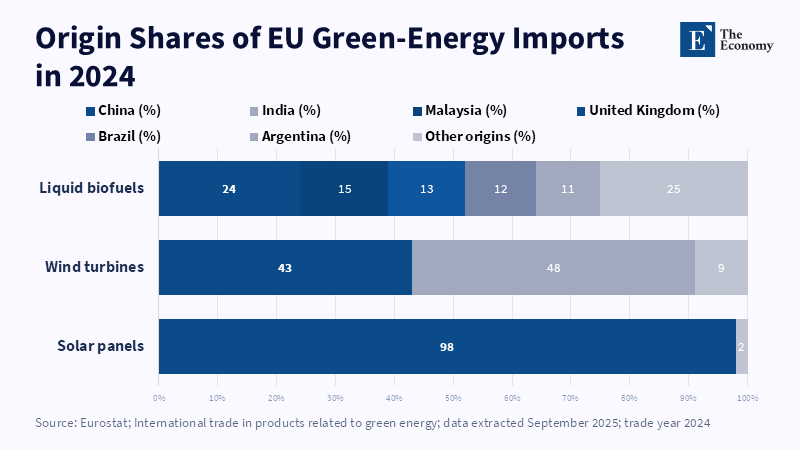

In contrast, however, there exists a number of commercially significant import categories that are politically visible even if they may not display strategic vulnerability. The differentiation is even more stark in the case of green-energy products. In 2024, for example, China accounted for fully 98 percent of the EU's extra-EU imports of solar panels. Clearly, this implies severe concentration, though the policy significance of that concentration differs from the implication of extreme dependence on an upstream raw material or an industrial input. As solar modules are a stockable commodity, the deployment of installations can be less fungible than the crisis would dictate; whereas the core issue may be upstream, in wafers, cells, equipment, and industrial capacity, rather than in the customs value of panel imports. That does not diminish the potential concern, but it does help to explain why an emphasis on import share does not reveal the underlying mechanism of concern.[19]

A final limitation of simple import-share-based logic is that it ignores time. Carnegie’s framework identifies a distinct class of emerging-risk products: goods that retained relatively low current import vulnerability but became harder to substitute between 2019 and 2024 because production concentrated in fewer countries. In 2024, this group included 267 products worth around $341 billion, including network communication equipment, electric motors, and other data-processing machines.[20] These products are significant, not because they had already become the most pressingly risky dependencies, but because their risks were rising as policy was still playing catch-up. A simple statistical indicator that only considers present import shares or even present levels of concentration would not distinguish these movements until they had already become problems.

Thus, the practical conclusion is narrower than many political soundbites, but arguably more demanding. The EU does not have a broad-based crisis of reliance on China across its entire import architecture. It has a more focused dependence on a specific suite of products, whose disruption will cascade through the rest of the economy because of their strategic significance. The decisive combination is supplier concentration, limited substitutability and systemic importance that makes those products important. For that reason, vulnerability must be assessed at product level rather than inferred from the overall trade balance with China or headline import values.[21]

3. IVI and SDI as a diagnostic tool

A more credible EU framework begins by distinguishing two sets of questions that are often mixed. One is whether an import relationship itself is vulnerable. The second is whether the relationship is hard to substitute once it is disrupted. The Import Vulnerability Index and the Substitution Difficulty Index are useful exactly because they separate those questions. In Carnegie's 2026 model, the Import Vulnerability Index measures dependence on imports and the consequences of interruptions in supply, and the Substitution Difficulty Index measures how hard it would be to replace the good with alternative suppliers or substitutes.[22] The framework then sorts the product into a two-dimensional space rather than forcing a single ranked list. That's an important conceptual advance because policy needs to understand not just how exposed the EU is, but also what flexibility it would have to adjust in response.

The IVI can be constructed from indicators of source-country concentration, using the Herfindahl-Hirschman Index, import share of the largest supplier, inverse number of suppliers, and volatility of flows.[23] Carnegie's formula explicitly adopts the same components to construct a simple product score of import dependence between zero and one. Although earlier Commission work does not use the same label, it shares precisely the same logic: an expression of extreme sourcing, the apparent scarcity of world output, and the relative absence of a strategic industrial capacity are summarised in the development of an index of critical dependence on those thousands of product lines. Neither treats import vulnerability as a matter of concern per se: both use it as a benchmark for measurement.

The Substitution Difficulty Index contribution is considerably more novel and, in terms of policy, more significant. Carnegie measures the difficulty of substitution using the inverse of a latent supplier count, which is modeled as a function of the variance of unit costs over suppliers as a stand-in for heterogeneity of products, and the entropy of the distribution of supplier shares, to infer the concentration of the supplier structure.[24] These variables are relevant since the ability of a product to be substituted is not obviously the same as import concentration. A product may be imported from a narrow base of suppliers, and yet be readily replaceable if there are many latent suppliers elsewhere. Alternatively, a product may appear relatively stable, since imports are currently spread across many suppliers, but be extremely difficult to substitute if the production of the good takes place in a few countries or if the heterogeneous nature of suppliers means that technical switching costs are high.

This distinction has an immediate analytical payoff. A product in the high-vulnerability, easy-to-substitute box is a different policy problem from a product in the low-vulnerability, hard-to-substitute box. In the first case, the EU is already importing heavily from a narrow set of suppliers, but credible alternatives exist, so diversification, trade facilitation, or a medium-term rotation of suppliers could significantly reduce risk. In the second case, imports look stable at present, but the global market might be so structurally concentrated that any future shock would be very difficult to absorb. The second is a preparedness problem rather than one of diversification in the narrow sense.[25] This is why the specific matrix matters more than any single aggregate score.

For the EU, however, IVI and SDI should not be the final stage of diagnosis. They are the first stage. The second stage should overlay industrial criticality. Carnegie is correct to argue that it is the structural role of the good in the productive economy that is relevant, not the trade volume at stake. The goods that have high forward linkages, including, especially, raw materials and intermediates, can halt multiple downstream sectors. And the ECB's modeling reaches a compatible conclusion: critical dependencies matter, precisely because they are production inputs with very low substitutability whose disruption has amplified effects on final demand. A product-level EU framework needs to take IVI/SDI as a starting point, adding the forward linkages or system-critical filter thereafter to identify strategically vulnerable items.[26]

That sequencing also helps preserve analytical discipline. A common flaw in economic-security debates is to load geopolitics too early into the classification process. Political distance, coercive intent, and past use of export restrictions are important, but they answer a different question from the one addressed here. The first stage should determine whether the product relationship is economically consequential under disruption. Only after that should policymakers add geopolitical filters concerning country risk or coercive intent. The Council’s economic-security framework itself separates supply-chain resilience from coercion and technology leakage as distinct risk categories. Doing so prevents trade monitoring from collapsing into a predetermined geopolitical narrative and helps keep de-risking proportional.[27]

The framework has to be supplemented with its temporal dimension, monitoring over time. If the IVI-SDI map is static, and captures only the bottlenecks at the moment, it will be unable to catch riskier product lines, where world production is becoming increasingly concentrated, that the emerging-risk category can clearly highlight in Carnegie's example, where present thresholds under discussion. Specifically, the EU should monitor explicitly a set of lines that does not begin in the least-vulnerable and most-competitive trade position, but finishes there. Electric motors, communication network equipment, and some data processing machinery belong to that set according to Carnegie's comparison. These are not yet the most acute dependencies, but the situation that benefits most from early diversification and suffers most from late intervention.[28]

Any EU implementation of IVI and SDI should also, therefore, reflect the limitations of trade data. Commission and academic analysis is well aware of the fact that trade data, although a practical indicator, tends to overstate or understate the industrial capacity along the trade chains: using exports as a proxy for domestic capacity can overstate a country’s actual productive capacity where goods are re-exported and, conversely, suggesting an individual indicator than can understate the true capacity of that country in those cases where exported goods are consumed internally. This issue, however, appears to be far wider. Trade data does not account for ownership structures, licensing dependence or for patents and process licenses; nor for concentration of logistics routes or distribution of inventories inside the Union. Trade data also do not capture product certification issues inside sectors where technical standards, safety certifications, or customer qualification processes contribute to slowing down switching. In any event, it is essential, yet not sufficient, to use trade data to screen.[29]

This requires that any institutionalized EU diagnosis be layered. The first layer should be trade-based and continuous: COMEXT, Eurostat, BACI, and related customs data should be used to update IVI and SDI scores, quarterly or yearly. The second should involve market-structure validation; surveys to firms, customs microdata if available, public procurement records and policy consultation should help test whether latent suppliers are even viable. The third should involve industrial-propagation analysis; input-output tables should help estimate their downstream exposure, and, if possible, firm-level network evidence. The fourth layer should be a strategic overlay, focused on geopolitical risk, ownership/control of technologies, and crisis relevance. This would enable a useful correction for the blind spots of the customs-based indicators, while maintaining the strength of the IVI-SDI method.[30]

Another, final, reason for preferring the IVI-SDI logic is that it keeps policy ambition in check. Vague pronouncements about dependence on China open the floodgates of policy remedies: generalized reshoring; blanket tariff escalation; symbolic local-content mandates. The OECD's recent inquiry offers a useful counterweight to that tendency. It concludes that simply shifting inward does not automatically enhance supply chain resilience, and that policies seeking to relocalize trade can impose more than an 18 percent shrinkage in global trade and a 5 percent hit to global real GDP, without consistently improving stability.[31] A more focused diagnostic is thus primarily a tool to prevent costly policy overreach. If the EU is unable to distinguish high IVI from high SDI, or current dependence from nascent dependence, it will apply large, coarse instruments to complex problems and pay dearly for the analytical imprecision.

4. Product-level risk categories

Beyond this, four categories of products emerge that yield policy-important differences once import vulnerability and substitutability are separated. The usefulness of this typology is not a straightforward taxonomy but emphasizes who will be asked to share the burden and according to what principle: proportionality. If a good is easily substituted, it should not erect a greater policy burden than the quantities where substitution capacity is geographically or structurally limited would lead to. In the same way, a category of goods that are temporarily not import-dependent but are structurally becoming less substitutable should not simply be disregarded, as those flows are currently not import-dependent.

The first are low-vulnerability, easily-substitutable products. These products reside within what by now is familiar ground: Carnegie’s supply-chain comfort zone. They are not overly exposed to import distortions, nor are they structurally difficult to replace. In fact, they are often standard goods supplied by many nations with low product differentiation and low switching costs. It is these products for which the case for government intervention is the weakest. Light-touch monitoring and maintenance of open channels of trade should be the aim. Interventions that advocate industrial activism should be firmly resisted at this level of categorization. A significant flow from China does not in and of itself imply a strategic dependency, if it has social visibility, nor due to the nation of origin if other credible suppliers are available. Normal competition policy and standing applications of trade policy are the correct responses if the product is not system-enabling.[32]

The second group relates to high-vulnerability, easy-to-substitute goods. These are products for which the EU is heavily exposed today but where switching remains technically and commercially feasible; they can often be attractive for the EU to import in high concentration, in some cases because a majority can be obtained from one or a few suppliers, but where, in principle, substitution is technically and commercially possible. According to Carnegie's matrix, this area best indicates where the EU should seek to gradually lower its reliance, with the constraint being the easy availability of alternatives. These are the cases of diversification. The key policy instrument would be transparency, searching for a supplier, the use of trade agreements and strategic partnerships, and, as with onshoring, where necessary, the procurement of redundant capacity rather than single-source optimums. Munkøe’s typology is also convincing on this issue; where supply is strong diversifiability, efforts should be aimed at giving consumers and the EU as a whole access to substitutes instead of investing in a large single domestic plant.[33]

The third subsample contains low-vulnerability, hard-to-substitute goods. These are the most uncomfortable from a strategic standpoint because they instill a false sense of security. Possible current import stability or high diversification in the export basket could be overshadowed by the presence of hurdles to imports overcoming existing installed bases because global supply remains determined by a handful of countries, the exporting sector has significant heterogeneity, or licensing and engineering requirements translate into high switching costs. Carnegie recommends preserving strategic stocks and specifically protecting the supplier structure (by multi-commodity supplier holdings and multi-asset holding companies), sheltering supplier diversity, forging long-term agreements, and holding low-to-moderate levels of precautionary stocks. The assessment is persuasive that the category is of concern in particular to the EU because a few of the technology-intensive products undergoing "source country" transition are in fact of this category. Carnegie's emerging-risk analysis shows an increase in supplier concentration in network communication equipment, electric motors, and data-processing byways since 2019, and in its early stages, has not resulted in any emergent "serious current threats to imports". Such tendencies are precisely the domains in which early policy action can make sense, because it is facilitating avoidance, rather than attempting to remedy, a lock-in now apparent.[34]

Finally, there is the category of high-vulnerability, hard-to-substitute goods. The most dangerous quadrant is the one where immediate exposure is problematic, and the adaptive capacity is weak. In this case, a short-term single damage event is foreseen and difficult to cope with, and the downstream impacts can be very large. Trade policies are rarely enough. Carnegie identifies domestic capacity, allied co-production strategies, and long-term offtake agreements as appropriate measures. Munkøe identifies strategic stockpiles, high-profile strategic projects, and broader government assistance among other practical options for the cross-categorization of low diversifiability with low substitutability. Using ECBs by the single-point-of-failure lens of weak dependency from China fits well with this category: even small import shocks in important concentric and central exporting locations can produce outsized macro effects.[35]

Several China-facing raw materials clearly fall into this category, although not all with the same intensity. Magnesium may be the most straightforward example. According to Eurostat, China accounted for 92 percent of EU imports of magnesium in 2025. This material is used in industries as diverse as automotive, aerospace, and electronics, and its supply risks have been comprehensively identified in the Commission's framework for critical raw materials for years. But magnesium is not only concentrated; it is concentrated in such a way that it serves the whole industrial sector. Rare earths constitute a slightly more complex yet still strategically significant case. In 2025, 40 percent by value of EU imports of this group of materials originated from China, but China was the main supplier for 11 out of 14 detailed product categories, and the top three suppliers accounted for fully 96 percent of all EU imports by weight. However, what is most significant here is not only China's immediate market share, but the weakness of the alternative market and the impossibility of rapidly scaling up substitute sources of supply.

Recent Chinese measures also deepen the distinction between concentration and strategic vulnerability. The European Commission's trade-barrier documentation records that, in July 2023, China imposed export controls or licensing requirements on gallium and germanium; in October 2023, on graphite; and, more recently, on antimony and some related commodities. The fact that such actions do not always foreshadow weaponized levels of import dependency does not mean that, for some trades, supply interruption could remain little more than a theoretical concern. Where the trades involve commodities already identified by a high degree of supplier concentration and high substitution costs, the inherent risk category must be moved up a notch. Here, the EU is not concerned with an ordinary market dependency but with a material preparedness problem.[36]

At the same time, the classification must be abstract enough to take account of different causal pathways. A good might fall into the high-high category because global manufacturing is geographically concentrated, because economies of scale for an alternative supply of that good are a decade long, because of regulatory barriers that slow changeover, or because domestic demand is fixed to a design standard that cannot be changed quickly. These are not the same problems and cannot therefore have the same solution. For some crucial raw materials, recycling, substitution, and offtake might trump tariffs. For some manufactured goods, the constraining factor may not be physical scarcity, but concern over supplier isolation, history, and scale. What is good about the risk category classification, then, is that it does not lump all dependence on China under one policy umbrella.

The common counterarguments deserve full weight. Concentrated sourcing can reflect efficient specialization rather than fragility. Diversification can raise costs for firms and consumers. Chinese investment in Europe can sometimes expand local manufacturing capacity rather than weaken it. Domestic production may remain commercially non-viable without continuing support. Those objections invalidate any mechanical presumption in favor of shorter or nationalized supply chains. They do not negate the diagnostic framework; they sharpen it. Intervention should be limited to products for which the likely economic damage from disruption exceeds the efficiency costs of mitigation and where the selected instrument addresses the actual source of vulnerability.

One final, underappreciated category is the transition case across quadrants. Goods do not stay still. Carnegie's distinction between high-risk and emerging-risk goods is valuable because it introduces movement into the framework. By 2024, some goods had already jumped the hurdles to become both high-risk and hard to substitute; others had become harder to substitute without yet being vulnerable. This dynamic perspective should be another central element of EU practice. In economic-security policy, the most expensive errors are rarely failures to respond promptly to fully visible vulnerabilities; they are failures to act when diversification was still a realistic option and when the supply base had not yet consolidated into hardened dependencies. A quarterly or annual EU top-ranked list of those products drifting into emerging-risk status would be more insightful than yet another static political ranking of dangerous imports.[37]

5. Policy implications

The policy implication of the risk-based approach is not generalized deregulatory decoupling from China; it is selective de-risking, as product-specific analysis would indicate. The difference is not merely semantic. Broad decoupling presumes as an objective in itself the reduction of all bilateral trade dependence. Selective de-risking considers that objective as specifically aimed at the reduction of those economic vulnerabilities that have serious market stability implications, while at the same time preserving the benefits of economic openness where it is without either economic security gains or economic stability risks. The EU's own economic-security framework would point to this approach. The EU Council itself sees supply-chain resilience as part of a broader economic-security dialogue, and the OECD suggests strongly that inward-looking measures are counterproductive if they come at the expense of efficiency without compensatory benefits for stability.[38]

The first requirement is institutional. The EU needs a standing product-level monitoring system that ties together customs data and industry’s criticalities. The Commission has taken a step in this direction with more and more fine-grained dependency maps and with the Supply Chain Analytics Hub, but that diagnostic remains more useful as the basis for episodic studies than as a regular part of decision-making. The next step should be the launching of an operational vulnerability observatory with quarterly updates, with at least IVI-type and SDI-type indicators but with additional trend-flagging for increasing risk products, that would be used for immediate Commission, Council, and Member States' preparedness work rather than with merely analytical publication outputs. Early warning only helps if it moves procurement, financing, and industry-to-industry coordination before the disruption.

The second requirement is mostly methodological and therefore requires the EU to move from static customs snapshots to integrated market intelligence. Borin et al. show that micro-level domestic network data can reveal significant trade exposure that average input-output tables greatly underestimate. This does not suggest that Brussels is able or should construct incumbent firm-level maps for every supply chain. However, it does suggest that for sensitive products and high-risk emerging risks, customs data should be validated with firm surveys, industry associations, critical infrastructure operators, large importers, and where legally and institutionally possible, microdata on firm networks. Without this second layer, the EU will know where imports enter the Union, but not where the financial hardship would have occurred, and the real economy would have suffered.[39]

The third lesson is that diversification policy should be used mostly in the high-vulnerability, easy-to-substitute, and emerging-risk quadrants. In those fields, the EU should strive to broaden the supplier base before dependence hardens. Trade agreements, raw material agreements, export-credit, supplier-finance tools, transparent tender design, or assistance for supplier qualification can trump tariffs. Some evidence of this has already been displayed in the Critical Raw Materials Act. It's explicitly targeted at diversification through broadening import sources and partnerships with reliable third countries, rather than through aggregate import compression measures. That is the correct strategy in those commodities for which the central challenge involves the lack of inherent alternatives, rather than narrowing actual choices.[40]

The fourth implication indicates that the stockpile should be used much more judiciously than political debate would sometimes have it. Stockpiles are most justified where the product is absolutely unique, the damage caused by any disruption would be huge, and there is the ability to store the material without prohibitive degradation or cost. The EU’s 2025 Stockpiling Strategy is significant because it extends preparedness planning to critical raw materials and seeks EU-wide coordination rather than purely national reserves. That's reasonable. But this should never be a backstop to diversification, nor is it practicable for all critical products. It is a bridging tool for the high-SDI categories, particularly wherever alternative-capacity lead times are long and supply interruption is plausible.[41]

The fifth implication is about industrial policy. Support should focus on the so-called hard cases: high-vulnerability, hard-to-substitute products in which market diversification alone will not do. It is instructive to look at the approach taken by the Critical Raw Materials Act: setting out standards for extraction, processing, and recycling, as well as not becoming overly dependent on one third country for each strategic material, combined with supply-chain oversight, stress testing, and a collaborative approach to maintaining stock levels. Its 2030 benchmarks-10 percent extraction, 40 percent processing, 25 percent recycling, and no more than 65 percent reliance on one third country for each strategic material-are not an exclusivist call.[42] They are a reminder that some supply chains will need some internal or allied capacity to be resilient, rather than simply trying to pin market reliance further afield.

Even in that realm, industrial policy should always be conditional, and never doctrinal. Domestic capability should not be developed simply because a product is politically sensitive or because the country exports to China. The criterion should be: does the product end up in the high-high quadrant following application of the industrial criticality filter, is market-based diversification quasi-structurally impossible, and could the capacity become at least conditionally viable in an EU or allied market? Lifelong support for non-viable production is not resilience; it is simply money redistribution. The CRMA’s combination of strategic projects, permitting speed-ups, and risk-preparedness obligations is forward-looking exactly because it gets to a scale more modest and more structured than 'buy European' unconditioned sentiment.

Sixth, trade-defense instruments must not be equated with dependency reduction, even in the case of China. The EU's definitive countervailing duties on battery electric vehicles from China applied, like all countervailing duties, on the basis of the threat of injury to EU producers from market distortion due to subsidization in China. That may be prudent policy in the case of one product in one sector, but it is not by itself a model for strategic dependency management. Strategic vulnerability does not necessarily entail subsidization; subsidization does not necessarily entail strategic vulnerability. Trade defense is thus a risk-reduction tool, not a blueprint for economic security policy. Relying on it in place of targeted national comparisons of strategic products risks a mismatch between threat and response.[43]

The seventh implication is collective purchasing and demand aggregation. The expansion planned in 2025 of the EU Energy Platform to an EU Energy and Raw Materials Platform is not insignificant. Collective gas purchasing since the Russian invasion of Ukraine demonstrated that even in a game with few new entrants, coordination limited intra-European competition. The same principle could, suitably adapted, apply to some critical materials and strategic inputs. For products placed in the low- or high-vulnerability, hard-to-substitute portions of the matrix, coordinated purchasing would enhance bargaining power, help secure long-term contracts, and mitigate the risk that member states outbid each other under stress. This cannot become a common EU purchasing agency. It must evolve as a focused instrument for the relatively small number of products for which the economies of scale and aggregation make a tangible difference.[44]

The eighth implication, political and legal, is directly related to that challenge. EU firms and Chinese businesses require most of all a concerted message from Brussels that diversified sources, not broad-based disengagement, are the aim. This is important as the upshot of this will be the minimization of unwarranted escalation and its associated costs to European firms without any corresponding security benefit. This is also important as the current status quo is not that of an EU-China trade war but rather of focused clashes, fine-grained export restrictions, and increasing defensive policy. The adoption of a risk-based approach enhances the EU's standing in such an environment by making visible that economic measures are evidence-based, proportionate, and target particular products or bottlenecks, rather than being reflective of an indiscriminate anti-China paradigm.

The ninth implication concerns allied dependence. One of the strongest defenses of de-risking away from China is that substituting into allies’ supply chains can keep Europe dependent on other countries. That argument is an accurate answer, at least up to a point. The Commission's 2026 work explicitly recognizes that politically aligned partners can impose trade restrictions, too. But perhaps the biggest policy take-away is that diversification is not impotent; it just requires thinking about dependence by governability as well as by concentration. Dependence on a reliable partner with open institutions, compatible legal norms and substantial experience in negotiated disputes sets it apart from dependence on a supplier combining concentration with repeated export restrictions, or one that is a geostrategic source of friction.

Taken together, these implications amount to a doctrine of proportionality. Low-risk goods require little more than monitoring. Vulnerable-but-substitutable goods call for diversification and supplier development. Stable-but-hard-to-substitute goods demand preparedness, precautionary stocks, and long-term contracting. High-vulnerability, hard-to-substitute goods justify the most intensive mix of instruments: stockpiles, strategic projects, allied co-production, recycling and substitution support, crisis exercises, and, in some cases, selective screening of investment or technology transfer. That is selective de-risking in operational form. It is economically more disciplined than broad decoupling and strategically more serious than continuing to treat bilateral import shares as a sufficient measure of risk.[45]

6. Conclusion - Selective De-risking Through Product-Level Diagnosis

The EU's problem in its China-facing import profile is not the scale of trade; it is the very narrow grouping of system-enabling goods for which imports are already highly exposed, or fundamentally difficult to substitute or becoming harder to substitute. Observed import levels alone do not reveal this grouping. They can hardly fail to record commercial proximity, even when that is of no use from the perspective of political exposure. Instead, they obscure the economic dynamics that convert proximity into strategic vulnerability: remote sourcing, elaborate supply chains, product heterogeneity, transmission through domestic upstream supply chains, and close downstream industrial interdependence. This, then, is the criterion based on import vulnerability and substitution difficulty, filtered through industrial criticality, which provides the most prudent guide to European policy. It is more appropriate than bilateral balances, sector-based headlines, and broad-brush assertions about dependence on China. That set of frameworks results in a cautious yet challenging policy recommendation. The EU must not adopt across-the-board decoupling but establish systems of selective de-risking, with differentiated approaches to differentiated product risks. Monitoring must be continuous, diversification focused, stockpiling selective, and industrial policy held in readiness for the genuinely hard cases where market correction is too slow or too weak to be effective. If Europe does not make these distinctions, it will underreact to real bottlenecks or overreact to trade balances that are both commercially sound and strategically sustainable.

References

[1, 5, 20, 22, 24] Ülgen, S. (2026) ‘From trade dependence to geopolitical leverage: The EU in an era of weaponized interdependence’. Washington, DC: Carnegie Endowment for International Peace.

[2] Eurostat (2026a) EU trade with China: Latest developments. Statistics Explained. Luxembourg: Eurostat.

[3] Eurostat (2025a) ‘EU high-tech trade back to a surplus in 2024’, Eurostat News, 24 September. Luxembourg: Eurostat.

[4, 6] European Commission and High Representative of the Union for Foreign Affairs and Security Policy (2023) European Economic Security Strategy. Joint Communication JOIN(2023) 20 final. Brussels: European Commission.

[7, 17] European Commission (2021) Strategic dependencies and capacities. Commission Staff Working Document SWD(2021) 352 final. Brussels: European Commission.

[8, 12, 23] Arjona, R., Connell García, W. and Herghelegiu, C. (2023) An enhanced methodology to monitor the EU’s strategic dependencies and vulnerabilities. Single Market Economics Papers, No. 14. Luxembourg: Publications Office of the European Union.

[9, 10, 29, 45] Bonnet, P., Di Girolamo, E.F., Pagano, A., Velazquez, B. and Zaurino, E. (2026) EU foreign dependencies: Assessment of trade and geopolitical vulnerabilities. DG Trade Chief Economist Note 2. Brussels: European Commission.

[11, 21, 31, 32] Kowalski, P. and Andrenelli, A. (2025) ‘Economic security and vulnerabilities in international supply chains’, in OECD, Economic Security in a Changing World. Paris: OECD Publishing.

[13, 14, 30] Borin, A., Conteduca, F.P., Leone, F., Mancini, M. and Zoi, P. (2025) How global are local supply chains? CESifo Working Paper No. 12271. Munich: CESifo.

[15, 16, 26, 35] Attinasi, M.G., Boeckelmann, L., Gerinovics, R. and Meunier, B. (2025) ‘Unveiling the hidden costs of critical dependencies’, ECB Economic Bulletin, Issue 5/2025. Frankfurt am Main: European Central Bank.

[18] Eurostat (2026b) International trade in critical raw materials. Statistics Explained. Luxembourg: Eurostat.

[19] Eurostat (2025b) International trade in products related to green energy. Statistics Explained. Luxembourg: Eurostat.

[25, 33, 34] Munkøe, M.M. (2026) ‘Strategic approach to mitigating Europe’s critical dependencies: Aligning economic security instruments with the criticality of supply chains’, Intereconomics, 61(3), pp. 180–188.

[27, 38] Council of the European Union (2026) European economic security. Brussels: Council of the European Union.

[28, 37] Arjona, R., Connell García, W. and Herghelegiu, C. (2024) Supply Chain Tectonics: Empirics on how the EU is plotting its path through global trade fragmentation. Single Market Economics Papers. Luxembourg: Publications Office of the European Union.

[36] European Commission (2026a) Chinese export restrictions on gallium, germanium, graphite, antimony and other materials. Access2Markets Trade Barrier Database. Brussels: Directorate-General for Trade and Economic Security.

[39] European Commission (2025a) DG GROW Supply Chain Analytics Hub. Brussels: Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs.

[40, 42] European Parliament and Council of the European Union (2024) ‘Regulation (EU) 2024/1252 establishing a framework for ensuring a secure and sustainable supply of critical raw materials’, Official Journal of the European Union, L series, 3 May.

[41] European Commission (2025b) EU Stockpiling Strategy: Boosting the EU’s material preparedness for crises. Brussels: European Commission.

[43] European Commission (2024) ‘EU Commission imposes countervailing duties on imports of battery electric vehicles from China’, Access2Markets News, 12 December.

[44] European Commission (2026b) EU Energy and Raw Materials Platform. Brussels: European Commission.