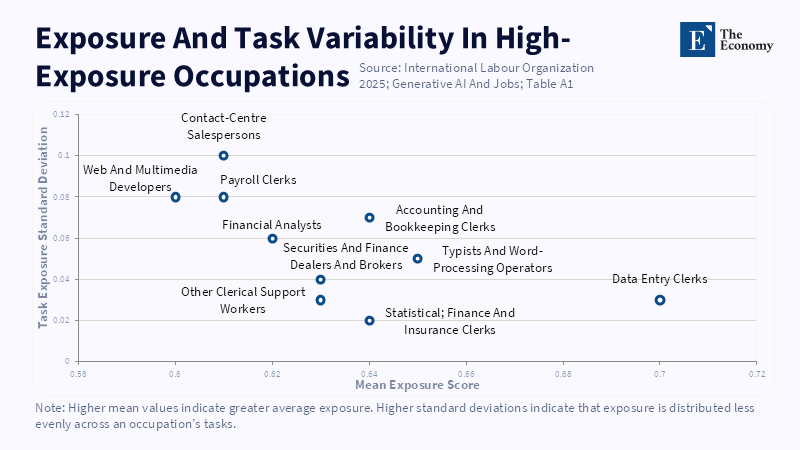

Exposure and Task Variability in High-Exposure Occupations for AI

Exposure and Task Variability in High-Exposure Occupations for AI

Picture

Real name

The Economy Graphics

Bio

The Economy Graphics is a dedicated visual research team for The Economy, responsible for producing high-quality data charts, analytical graphics, and visual summaries that support the publication’s coverage of global economic, financial, technological, and policy developments. Drawing on data from research articles, public datasets, institutional reports, and The Economy’s own research team, the account transforms complex information into clear, structured, and publication-ready visual materials.

Its work emphasizes accuracy, methodological transparency, and visual consistency across The Economy’s editorial ecosystem. By translating quantitative findings and research-based insights into accessible charts and data-driven visuals, The Economy Graphics serves as a foundation for The Economy Intelligence, helping readers understand market structures, institutional trends, and long-term economic shifts through evidence-based visual analysis.

Its work emphasizes accuracy, methodological transparency, and visual consistency across The Economy’s editorial ecosystem. By translating quantitative findings and research-based insights into accessible charts and data-driven visuals, The Economy Graphics serves as a foundation for The Economy Intelligence, helping readers understand market structures, institutional trends, and long-term economic shifts through evidence-based visual analysis.

Authored On

Modified

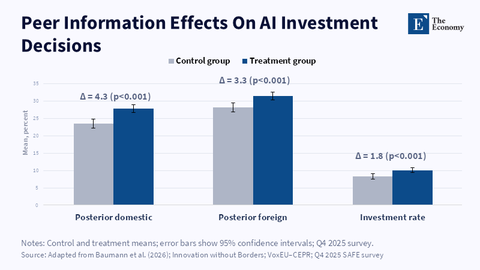

Related article: Why AI Fiscal Erosion Begins Before Jobs Disappear | The Economy

Picture

Real name

The Economy Graphics

Bio

The Economy Graphics is a dedicated visual research team for The Economy, responsible for producing high-quality data charts, analytical graphics, and visual summaries that support the publication’s coverage of global economic, financial, technological, and policy developments. Drawing on data from research articles, public datasets, institutional reports, and The Economy’s own research team, the account transforms complex information into clear, structured, and publication-ready visual materials.

Its work emphasizes accuracy, methodological transparency, and visual consistency across The Economy’s editorial ecosystem. By translating quantitative findings and research-based insights into accessible charts and data-driven visuals, The Economy Graphics serves as a foundation for The Economy Intelligence, helping readers understand market structures, institutional trends, and long-term economic shifts through evidence-based visual analysis.

Its work emphasizes accuracy, methodological transparency, and visual consistency across The Economy’s editorial ecosystem. By translating quantitative findings and research-based insights into accessible charts and data-driven visuals, The Economy Graphics serves as a foundation for The Economy Intelligence, helping readers understand market structures, institutional trends, and long-term economic shifts through evidence-based visual analysis.