Inflation Expectations Need a Shock Filter

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Inflation expectations can turn an oil shock into lasting inflation Bond prices are useful, but they often mix forecasts with fear Policymakers need a shock filter before markets overreact

Financial markets move many times faster than household budgets. That's the real policy challenge behind the new inflation scare. In June 2022, U.S. consumer inflation measured 9.1 percent. A few months later, euro-area inflation hit 10.6 percent and UK CPI hit 11.1 percent. Those were not just price shocks. They were expectation shocks. Firms raised prices in anticipation. Employees demanded payback. Central banks slammed on the brakes because delay was expensive. The key to the inflation scare is not that each oil price spike must be met with blanket panic. It is that inflation expectations can turn a temporary shock into a lasting inflation problem. The liabilities of a temporary supply shock were magnified because firms, workers and investors began to act as if inflation had changed fundamentally. The next test is already apparent in energy futures and bond yields. A new supply shift need not turn into a second inflation regime. It may, however, if officials interpret the market message too literally, too late, or confuse fear with foresight.

Inflation expectations now require a more transparent public role. The usual inquiry is whether markets are concerned about inflation. That is too coarse a question. Markets are constantly pricing several risks at once: they are reflecting expected prices, risk premiums, liquidity pressures, fiscal strength, hedging demand and pressures to trade rapidly once new information arrives. Is there a narrower, more practical question? Yes. Which fraction of a market move indicates a real change in inflation expectations and how much is merely the price of being exposed to a volatile shock? This distinction is meaningful because a misinterpretation can mislead current policy. To overreact in the moment to a one-day energy price spike could wreak monetary havoc with nil impact on actual oil production. Conversely, to under-react in the moment to a persistent shock could allow firms and households to incorporate higher inflation into contracts. Beyond following the markets, policymakers must even learn to read them.

Inflation Expectations Need a Shock Filter

The recent inflation episode showed that inflation expectations are not a side issue. They are a part of the transmission system. As soon as the energy and food prices increased after Russia’s invasion of Ukraine, headline inflation began to accelerate. But then the inflationary panic migrated into wages, the terms of contracts, the prices in retail outlets, the rents and the momentum of politics. The most damaging aspect was not the initial surge in prices. It was the lost time during which central bankers "pondered" whether the initial "shock" was, in fact, transitory. That pause increased the influence of inflation expectations. As soon as consumers begin to regard every fresh input to price as confirmation of a longer economic momentum, the economy clamors for protection from the future. Firms defend margins, workers defend earnings and lenders defend real returns. While that protection might be rational for each contingent of the economy, it's disastrous for the whole.

This is why the inflation expectation series that we are concerned with represents, at most, a shock filter. A shock filter neither minimizes the inflation target nor diminishes its value; it merely shields the target from bad measurements. Simply looking at the estimates we have from Treasury inflation-protected securities and breakevens is revealing, since they are published daily; here, they have the critical feature of market discipline. But they are not pure measures of expected inflation. A 5-year breakeven (an estimate of the price level when five years from now) around 2.5% may seem placid compared with the spike at 10% in 2022, but it does not tell us what then is the policy-relevant quantity: How much of the implied price increase is due to future expected inflation and how much to compensation for risk, for example? It does not reveal whether it is coming from demand, energy, fiscal, or simply thin trading. And it utterly misses the fact that treating this single number as the measured predictor is too narrow and the resulting forecast is less accurate.

Inflation Expectations Are Not the Same as Bond Prices

The case for caution is compelling: the price of bonds can undershoot as well as overshoot. In early 2026, U.S. inflation pressures went up again, as higher energy prices took hold. The April consumer price index registered a 3.8 percent gain year on year, whereas the energy index increased 17.9 percent and Gas went up 28.4 percent. At the same time, long Treasury yields examined the 5 percent mark and daily five-year breakeven inflation traded close to 2.5 percent in early June. Those bits of data suggest the market was not ignoring the threat of inflation. They do not, however, confirm that the market, faced with the magnitude of the inflation threat, had found the equilibrium rate of inflation. A yield is the price of money across time and it tells many different stories. Inflation is just one story, while fiscal risk and term premia have their own to tell, too.

This is relevant because the lessons of 2022 are often understood too literally. It is claimed that central banks were behind the curve in 2022 and that they should respond now with even more haste to commodity price moves. This idea is straightforward but simplistic. The stronger lesson is that central banks must respond more quickly to persistent inflation expectations (even as they respond more slowly to individual headline price moves). An oil price blip will boost headline CPI but have a limited shelf life. The same oil price move will dissipate when the supply-demand balance reverts, inventories adjust and oil consumption cools. But a speed-up in response is critical once the hit migrates into core prices, to real wage demands and to medium-term inflation expectations. This is the difference between a temporary hit to the price level, which then causes relative-price adjustments and an inflation process in which non-temporary price hits induce an inflation response. While one damages living standards, the other induces behavioral changes that the central banks cannot address, but must do their best to eradicate.

Real-Time Inflation Expectations Need a Cross-Market Test

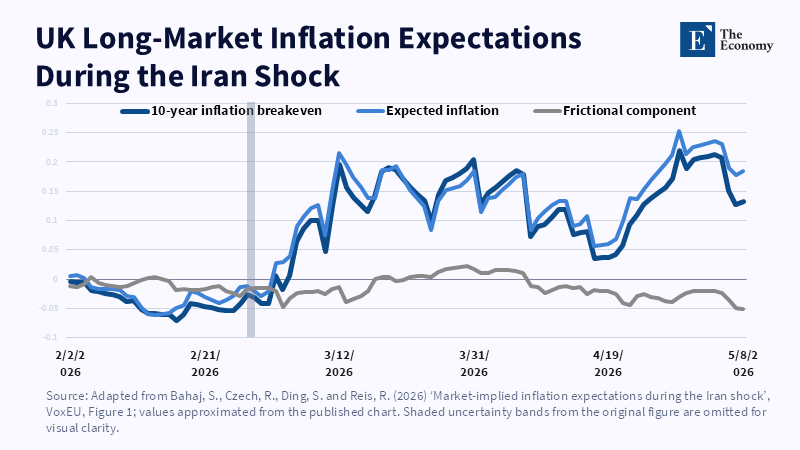

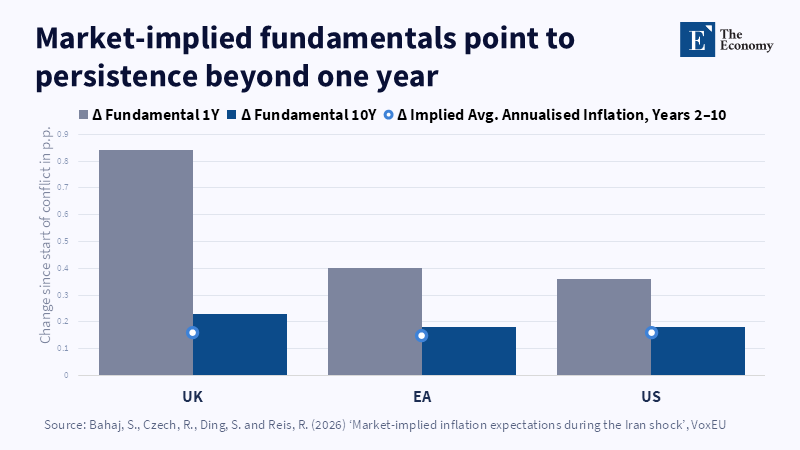

A better inflation expectations system should compare markets across countries and instruments. The point of the new approach is not to produce a single magic number. It is to generate a clearer accounting frame so that when oil futures, survey data, foreign exchange, inflation swaps, inflation-linked bonds and nominal bonds all change, the part in common can signal a real adjustment in expected inflation. The part left over may be risk, liquidity, or disequilibrium in any local market. This becomes very relevant for a supply shock. The U.S., U.K. and euro area all import, tax, price and subsidize energy in different ways. The countries' inflation-linked markets are different in terms of depth and composition as well. When oil shocks show up as persistent different inflation premia in those markets, that is information, not noise.

An illustrative benchmark is the energy-shock work on the Iran war. Using a cautiously optimistic scenario where a Persian Gulf closure lasts one quarter and could be unwound gradually, the authors estimate an impact on US headline inflation in 2026 of roughly 0.6 percentage points and about a 0.2 percentage points increase in core inflation. That margin gets to the heart of the policy question. Because fuel is visible and arrives on airhead, headline inflation could surge whereas core inflation would respond less unless firms and workers incorporate the shock into pricing. The method matters as much as the number. It starts with an oil-price path, follows it through to gasoline prices, then derives effects on inflation and household inflation expectations, illustrating better than any simple bond-market reaction how the shock is fed into the economy and for how long.

The policy relevance would be a real-time dashboard to separate the three signals. One is the path inflation is expected to take over the next 1 to 3 years. Another is the inflation risk premium-the price investors require to bear variance risk. And the third is an estimate of the impact of supply shocks-the supply-shock pass-through measure based on energy futures, tradables prices and import exposure. And one that need not be hard to use, ranges, revision notes and public language that states exactly what we can learn from any given signal. In that sense, the Cleveland Fed has begun down that road with its combined Treasury yield, inflation swap, survey expectation, CPI and risk premia model. Moving toward systemic cross-market supply-shock decomposition as a policy tool seems the next logical step.

Policy Should Respond to Persistence, Not Panic

The difficult part is the communication. Central banks often claim to 'look through' temporary supply shocks. This phrase is elegant in theory and potentially dangerous in practice. People do not 'look through' their electricity bills. Firms do not 'look through' their transport costs. If your pay is fixed, you do not 'look through' your shopping bills. When the authorities use that phrase before a clear test, it can seem almost callous. A clearer message would say this.A central bank should not raise rates simply because oil rose last week. It should act if inflation expectations, wage setting or core prices begin to shift This would be a more disciplined and more credible way of communicating than 'looking through' or fighting 'every shock'.

And outside the central banks, there are other policymakers to address. Ministries of finance should avoid a familiar mistake and avoid broad demand support that would turn the energy shock into an overshoot of demand. They should promptly focus on relief for energy-deprived households and sensitive firms before letting it expire as prices unwind. Agencies should routinely produce sharper, more timely notes on energy pass-through, transport prices and household inflation exposure. Politicians who have officially regulated prices should spare us super-inflationary snap-back equations that exaggerate peaks. The institutions setting the wage-setting system should save low- income workers by preventing the entire economy from indexing to the most recent monthly price peak. These are not extras. These are expectation programs. They are defining whether the energy shock remains a flash in the pan or becomes a new rule for future markets.

The main criticism is that market-based inflation expectations already do this. They are timely. They are real money. They are more difficult to manipulate than projections. All of this is true. However. The market is no final judge. The market is a fast vote that has leverage and hedging needs and fears built in. And when stress hits, too often the most important trades could be a matter of balance sheet constraint, rather than conviction. A fund purchasing protection on inflation may not believe in impending hyperinflation. Rather, it may be guarding a portfolio against a virtually impossible adverse event in the future. That is not trivially academic. If policymakers conclude from heightened demand for hedges that the economy is heading into the future, they may tighten too much and lead the economy into a recession. If they are confused by superficially anchored long-term rates with stability, then they may blunder right into a dangerous rise in near-term expectations.

A second criticism is that decompositions may be too opaque to present to the public. That is a danger. If a model cannot be interpreted, it cannot gain buy-in. The solution is not to avoid models, but to produce them using consistent rules. One line should show the raw market measure. One line should show the inflation expectations estimate. One line should show the risk premium. One footnote should explain what changed in the last update. This makes the uncertainty visible rather than superficial and overly harmonized. This would also make it less tempting to treat every change in the markets as an economic news story. Simple clarity is not incompatible with fine craftsmanship; in fact, clarity enables it.

The last inflation cycle has one last lesson to teach. It is a harsh one. Adjustment costs are greater when policy waits for certainty than when policy chases noise. The target must be an inflation expectations system that travels faster than the official CPI and slower than a market freak-out. The system must be lively enough to anticipate a real shift in expectation, yet strong enough to ignore a crowd market position. The first statistic is still a warning. When inflation hit 9.1 percent in the United States and double digits in Europe, the repair bill was no longer trivial. The next supply shock should not be allowed to bleed the same story. Create the shock filter today. Make sure that it is known to everyone. Deploy it before the next inflation spike turns into a contract, a wage push, or a political mandate.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bahaj, S., Czech, R., Ding, S. and Reis, R. (2026) ‘Market-implied inflation expectations during the Iran shock’, VoxEU, Centre for Economic Policy Research, 5 June.

Bianco, T. and Haubrich, J.G. (2010) ‘Inflation: Noise, Risk, and Expectations’, Economic Commentary, Federal Reserve Bank of Cleveland, No. 2010-05.

Bureau of Labor Statistics (2022) ‘Consumer prices up 9.1 percent over the year ended June 2022, largest increase in 40 years’, TED: The Economics Daily, 18 July.

Eurostat (2022) ‘Annual inflation up to 10.6% in the euro area’, Euro Indicators News Release, 17 November.

Federal Reserve Bank of Cleveland (2026) ‘Inflation Expectations’, Indicators and Data, updated 12 May.

Federal Reserve Bank of St. Louis (2026) ‘5-Year Breakeven Inflation Rate’, FRED Economic Data, updated 5 June.

Haubrich, J.G., Pennacchi, G. and Ritchken, P. (2012) ‘Inflation Expectations, Real Rates, and Risk Premia: Evidence from Inflation Swaps’, The Review of Financial Studies, 25(5), pp. 1588–1629.

Houle, B. (2026) ‘Is the Bond Market Misreading Inflation?’, Ferguson Wellman Capital Management, 22 May.

International Monetary Fund (2023) ‘Managing Expectations: Inflation and Monetary Policy’, World Economic Outlook, October.

Kilian, L., Plante, M.D., Richter, A.W. and Zhou, X. (2026) ‘Quantifying the impact of the Iran war on US inflation’, VoxEU, Centre for Economic Policy Research, 4 May.

Kilian, L., Plante, M.D., Richter, A.W. and Zhou, X. (2026) ‘The Impact of the 2026 Iran War on U.S. Inflation: A Scenario Analysis’, CEPR Discussion Paper, No. 21373.

Office for National Statistics (2022) ‘Consumer price inflation, UK: October 2022’, Statistical Bulletin, 16 November.

Wiltermuth, J. (2026) ‘High inflation is pushing yields to 5% on Treasury bonds’, MarketWatch, republished by Yahoo Finance, 12 May.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.