Space Innovation Funding Is the Missing Half of Market-Making

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Space became commercial because public authority first made the market credible The US needed less direct funding because deep private capital could finance the risk China shows why state funding matters when pre-IPO markets are thinner

In 2024, the global space economy was around $613 billion. And the remarkable thing isn’t just how big it was. It was an almost entirely commercial economy. Four-fifths of it, in fact. That is the clearest demonstration that space is no longer a Cold War-era public mission with a handful of contractors. It is a market based on launch slots, satellite broadband services, remote sensing, defense contracts, data management and long-term bets about orbital logistics. However, this change can be misinterpreted. Public authority does matter because it creates markets. It directs missions, determines safety regulations, procurement channels and early demand. But mere market creation does not account for why the US advanced more quickly than others. The missing factor is space innovation funding. Where the investor base is already substantial, the state can set the fabric for development and retire from the domain. Where that base remains thin, the state must also supply the funding itself.

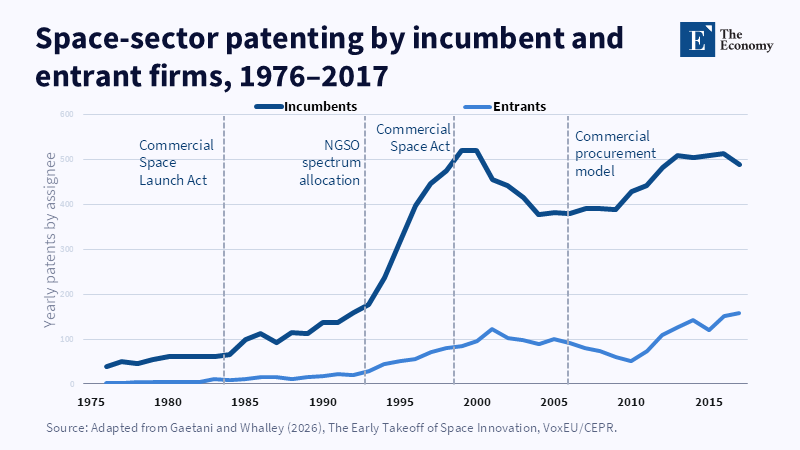

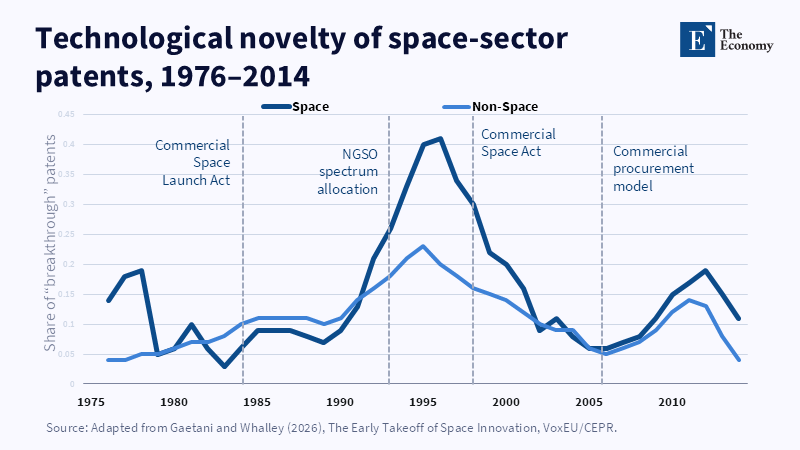

Space Innovation Funding Changes the Market-Making Story

The more insightful way to view the new space age is to separate two tasks that are often treated as one. One of these is market construction. It is governments who say a new activity can be used, bought and even done; it is they who remove the first credibility gap; they are the first credible buyers. They establish their own public procurement buyers who contribute by setting licensing standards and give companies a reason to venture forth with little support in the consumers' marketplace. This is very important in the space age because the first market is typically not the mainstream consumer market but the defense, the civil science sector, weather observation, navigation, launch access, or the public's research labs. Without the anchors there, the private company's nearly impossible problem is why put billions into systems that, on average, require years of flight, are prone to fail and are aimed at potential users in the distant future?

The second task is funding. Market construction proclaims there will be demand. Space innovation funding determines whether firms survive long enough to meet space construction. This distinction dramatically changes the policy lesson. It is not enough to say the public authority has to create usable markets. That is true, but incomplete. The same policy leads to different outcomes in two countries because capital markets are not the same. In the United States, a young space firm can raise huge sums of money pre-IPO. It can take advantage of the existence of venture capital, growth equity, strategic investors, private credit and secondary markets. In a middle power with a less well-established pre-IPO market, the same firm may secure a contract but not have a balance sheet. In China, the state attempts to fill this funding gap through subsidies, guidance funds, cheap credit and public-private investment vehicles. The issue is not the state or the market. It is the part of the market that the state has to supply.

The US Did Not Need a 1960s-Style Money State

The US did not reproduce the space race of the 1960s. It did not have to. The Apollo model belonged to a world of national prestige, Cold War fear and large federal budgets. But today's US model is different. It does not view NASA and defense agencies as funders alone but as market makers: paying customers it can work with. NASA's commercial cargo and crew programs provide the pattern. The amount of development support was not insignificant, but larger still was the credibility of a route to a service contract. SpaceX was allotted up to $396 million under the COTS arrangement, followed by a $1.6 billion commercial resupply contract and then a $2.6 billion Commercial Crew one. Boeing was awarded $4.2 billion in that crew framework. All that mattered. But the deeper significance was that they were signals to investors that the state would buy from firms that proceeded according to "fixed milestones".

This signal arrived in a capable capital market. By 2024, right in the middle of a slow exit cycle, US venture funds still had $307.8 billion of dry powder on the books; the deal-flow volumes for that year amounted to around $215 billion for fresh US venture deals and later-stage privately owned companies could have remained privately owned for longer because investors would fund them until they raised an IPO. But this is the key reason the US State was able to avoid carrying the entire funding burden. It did not have to opt for blank-cheque funding or inaction: instead, it could generate demand, specify safety and performance parameters, apply fixed-price contracts and fund a large proportion of the climb from the private markets. This is not to say that public funds were not relevant; instead, they were catalytic. The state paid for credible markets, private capital paid for building scale, speed and failure.

This does not imply that the US model is comparable to pure market success, but rather simply describes it as a public-private system where public agencies lowered the technical and demand risk and private investors took the scale and financial risk and universities, federal laboratories and defense customers supplied talent, test problems and early credibility. It built upward because of its presence in a single market in which a founder could employ engineers, win a milestone contract, raise a private funding round, acquire a defense customer and extend the delay on an IPO without detaching from the country's funding base. This is a unique best practice; it cannot be taken for granted elsewhere. This, too, is why the United States appears more free-market than it is. The intervention is not always a grant; there are times when there is no grant but a customer with whom private capital may cooperate.

China Shows Why Direct Funding Still Matters

China demonstrates the other side of the same policy logic. Its commercial space industry has developed quickly, but it has done so in a system where direct resources are a far more significant variable. This is not just a space story. It forms part of a larger industrial policy model. China has supported strategic industries through direct subsidies, tax reliefs, state provision of land, government guidance funds and state-backed debt. That has come at quite a cost. An estimate concluded that in 2023, the state had weighed in with a figure representing 4.4% of that nation's GDP to support industrial policy. Meanwhile, the government support for electric vehicles alone (funding mechanisms, procurement contracts, antitrust interventions) is estimated at over $230b between 2008 and 2023. Also for 2024, China's government guidance funds were reported to manage about RMB 4.52 trillion (around $623 billion). Also, Beijing announced a national guidance fund for venture capital of about RMB 1 trillion in 2025.

These numbers teach a simple lesson. If pre-IPO private capital is unable to take on the size and risk of the mission, then directly financing the space program can be more important. While China has plenty of private companies and dedicated entrepreneurs, its private-sector system has been subject to the exit pressure, policy swings and a weaker private risk culture than what prevails in the US. In such a context, one government contract may be insufficient; space will be necessary to partner with the state, to co-found, to finance the plant, to grow the supply chain, to safeguard early demand. And this can work. China's private-sector investment in space infrastructure grew dramatically in 2024, reaching roughly 2 billion in private funding and private launch companies are heading toward reusable rockets. But it can also be treacherous. When capital is too strongly policy-driven, companies tend to go after generous subsidies rather than customers and scale arrives before discipline. Funding must therefore remain performance-based and not simply a function of standing.

Space Innovation Funding Should Fit the Capital Market

The policy mistake for other countries would be to imitate the US surface model, without imitating the US capital base. A government can readily publish a space policy, create a space agency, offer challenge grants and declare procurement targets. Yet if private rounds are not forthcoming, it may fail. That is especially important for Europe, Japan, India, smaller advanced economies and middle powers with no Silicon Valley to neutralize the scarcities of a small domestic market. They should not, as a rule, treat the US case as proof that direct funding is generally unnecessary as a general phenomenon. It was less so in the United States because the pre-IPO market was large already. For countries that have not established that pool, public finance should not be treated as a distortion per se; it may be the conduit linking a policy announcement to a standing industry.

This bridge must be erected carefully. Funding for space innovation must not become a permanent safety net. It must mean phased risk-sharing. Governments should purchase results, not just hardware. They should use milestone contracts, matched funding, first-loss insurance, anchor tenants, public test-facilities and force competition at every stage. Firms failing to reach technical milestones must be cut off. Firms reaching milestones must face increasing private co-financing requirements. This prevents both types of failure. It prevents weak-market failure, where promising companies become extinct before the demand builds. And it prevents the subsidy trap, where the weakest companies survive because managers fear being blamed for losses. The goal is not to substitute government for investors. The goal is to facilitate the building of markets where there were none.

The messages should also be borne out in other ministries. For educators-those in engineering, economics and policy -funding space innovation should be treated as a real-life lesson in how to do industry policy: not only in 'why' and 'what' to fund rockets, but in 'how' to commercialize technology. Universities can design lab courses to simulate how to buy equipment, design a system, obtain export licenses, arrange financing and plan the vehicle. University service offices linking research labs with venture funds, defense accelerators and public test beds will expose students to how difficult otherwise 'frictionless' frontier technology is to bring to market. Policy schools should create neutral policy test beds at universities, where policy ideas can run through experiments before becoming political promises. Any nation training its engineers without training its entrepreneurs will produce talent waiting for a customer to show up. Any nation training its policy students without teaching financing will build missions that no firm can support.

Space Innovation Funding Must Be Disciplined

The strongest criticism is that funding more from the public purse will just mean more money wasted. This is a real problem. Space is awash with technospeak, political glamour and security language that mask mediocre choices. The answer is not to deny funding. It is to price risk more carefully. Agencies should enhance transparency by identifying contractual objectives, releasing milestone reports, limiting open-ended support and avoiding the rush to protect a single national champion too early. The American experience provides many lessons here, although in China, direct cash infusions can steer a program quickly, only if used in conjunction with market testing, or else they risk over-investing in capacity.

That space innovation funding is therefore not a marginal issue. It is the other half of the new industrial policy. The opening fact matters because it indeed costs $613 billion to create a space economy, it did not happen in free markets alone and it did not happen in a government budget alone. It thrived where public demand, known rules and private capital always intersected. The next countries that seek to gain a space position should begin with a clear audit of their own capital markets. If the depth of private growth finance is such that the state can accommodate market building as its main strategy, that strategy may work. If this is not the case, direct government funding must run from the very beginning to deliver the market creation that truly works. The call for action is very straightforward: do not ask any more whether the state or the market will build space. Ask a different question instead: can public authorities build the market and finance the gap before their rivals do?

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Advisory Ranking (2026) ‘Investment banking & capital markets advisory industry outlook 2026: Strategic dealmaking, private capital, and the return of issuance discipline’, Advisory Ranking, 31 January.

Gaetani, R. and Whalley, A.T. (2026) ‘The early takeoff of space innovation’, VoxEU, Centre for Economic Policy Research, 4 June.

Garcia-Macia, D., Kothari, S. and Tao, Y. (2025) Industrial Policy in China: Quantification and Impact on Misallocation. IMF Working Paper No. 2025/155. Washington, DC: International Monetary Fund.

Kennedy, S. (2024) ‘The Chinese EV dilemma: Subsidized yet striking’, Center for Strategic and International Studies, 20 June.

NASA (2012) ‘First contracted SpaceX resupply mission launches with NASA cargo to space station’. Washington, DC: National Aeronautics and Space Administration.

NASA (2025) ‘Commercial Crew Program Essentials’. Washington, DC: National Aeronautics and Space Administration.

National Venture Capital Association and PitchBook (2025) Q4 2024 PitchBook-NVCA Venture Monitor. Washington, DC and Seattle: NVCA and PitchBook.

Ranking News Editor (2026) ‘Global innovation rankings become a strategic tool for national economic policy’, The Ranking News, 16 March.

Reuters (2025) ‘China to set up national venture capital guidance fund, state planner says’, Reuters, 6 March.

Space Foundation Editorial Team (2025) ‘The Space Report 2025 Q2 highlights record $613 billion global space economy for 2024, driven by strong commercial sector growth’, The Space Report, 22 July.

The CEPR, Space Foundation, IMF, CSIS, Reuters, RankingNews and AdvisoryRanking details were checked against the source pages.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.