Digital Payment Inclusion Is a Design Problem, Not a Cash Problem

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Digital payments replace cash only when they feel easier than cash Poorer users adopt when payments are cheap, simple, and trusted Inclusion depends on open systems, merchant use and fraud protection

Cash is not disappearing on schedule. The most obvious sign is not the explosion in apps, cards, or QR codes. It is the chasm between use and trust. In 2023, cashless transactions per individual increased at a much faster rate within emerging and developing economies than in advanced ones. Transactions also accelerated rapidly. Despite this, cash withdrawals accounted for a much larger percentage of GDP in poorer markets than in the more affluent. That ratio reveals the true message. People are not rejecting digital payments. They are exploring them. They embrace them in the presence of affordability, proximity, simplicity and security. They maintain cash in the presence of digital arrangements that seem necessary, confined, unstable, or opaque. Consequently, digital payment inclusion is not a crusade to kill cash. It is a design test. The systems that succeed do not always offer an app. They let the initial transaction almost feel as simple as passing a bill.

Digital payment inclusion begins with cash-like convenience

A common framing assumes cash is an outmoded form, while digital is an innovation. The policy problem is not so simple. For the billions of less-affluent users, cash has four inherent advantages more important than convenience. You can pay with it nearly everywhere. You can pay with it: offline, without a PIN or data plan, without a bank branch or pipeline, without a power source. It provides anonymity and the flow of very small but personally meaningful choices. It automatically enforces the minimal obligation on both sides that something is exchanged. It proves instantly that the payment has taken place. Any digital system has to meet those standards before it can replace cash in daily life. Speed alone is not enough. A fast transfer is useless if it fails at the shop, adds a fee or forces the user to ask someone else for help.

Therefore, digital payment inclusion must be based on going from first use to full use. A low-income household might activate an account upon the receipt of a wage, a grant, a refund, or an allowance. However, that does not mean that the account has been useful for that household. The more relevant question should be, "Can that household use the account to pay a shop, to send money to family members, to receive a refund, to read the account balance, to correct an error and to trust the results without losing time or dignity?" If the response is negative, then the digital account is only a threshold. The individual remains in the cash economy.

The best policy indicator then is not whether 3 million accounts were opened over the last year, but what percentage of low-income users are using their accounts repeatedly without cashing out. Another indicator has to distinguish where digital payment inclusion takes hold: rent, electricity, transport, school fees, medicine and food payments; small business or artisan materials purchases. These are not niche payment areas. They are the payment areas that determine whether a digital system is embedded in daily life. When a state simply digitizes tax portals, online markets and formal salaries, it extends a digital layer over an existing formal system. When it digitizes small, local payments repeatedly and provides basic support for first-time users, it begins to change the cash economy.

Recent global evidence makes this gap clearer. Financial account ownership has hit historic highs and most adult individuals in low and middle-income economies own mobile phones. Yet, 1.3 billion adults are outside the formal financial sector. Even those who do have accounts often pay their utility or school bills in cash. One lesson is obvious. Access can increase while usage stays thin. Digital payment inclusion is not reached when people are considered connected. It is reached when a few digital payments become a safe habit and trusted utility in low-income locations where cash was once king.

Poorer users do not need more digital ambition

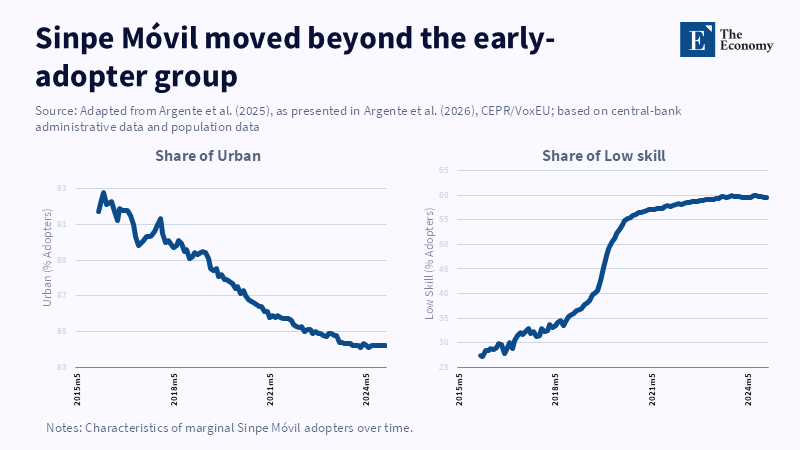

The ultimate policy takeaway is the income gradient. New payment systems start with the rich, urban and educated. That is expected. The key question is how rapidly the convergence occurs. If uptake remains skewed upmarket, digital payments become merely another mark of social advantage. If, by contrast, the technology extends down the income distribution in a few years, it may revolutionize the financial ecosystem. For this reason, the policy priorities must shift from absolute usage numbers at launch to the velocity of diffusion into the Bottom. It is not just more transactions; it is the proper users signing on early enough that the network attains network effects.

The best systems cut three costs at once. They drive down the cost of money by enabling free or very cheap person-to-person transactions. They drive down physical costs by making the system "work" through phones, QR codes, agents, shops and bank integration. They cut mental cost through simple ID's, reassuring confirmations and flows you recognize. These details seem trivial. They are not. To a low-income user, a failed payment can cost a bus, a hospital visit, or a penalty fee; to an informal merchant, an awkward checkout screen can cost a customer. The poor don't need more digital grandeur. They need fewer steps and fewer excuses for fear.

The difference between better and worse systems is also a reminder that change requires awareness. In the absence of other reinforcement, consumers will not use a new payment rail simply because it exists. They will purchase it only if family, traders, government agencies and employers all send the same message: "This method is okay here, at this time and this day". Marketing should not be ignored early. Early marketing is infrastructure. If people are to learn the utility of the device, the dealer's accounting method, the acceptance point, the cheat-prevention and the troubleshooting contact, they need social proof. Without social proof, a good system looks like a high risk even to the well-off.

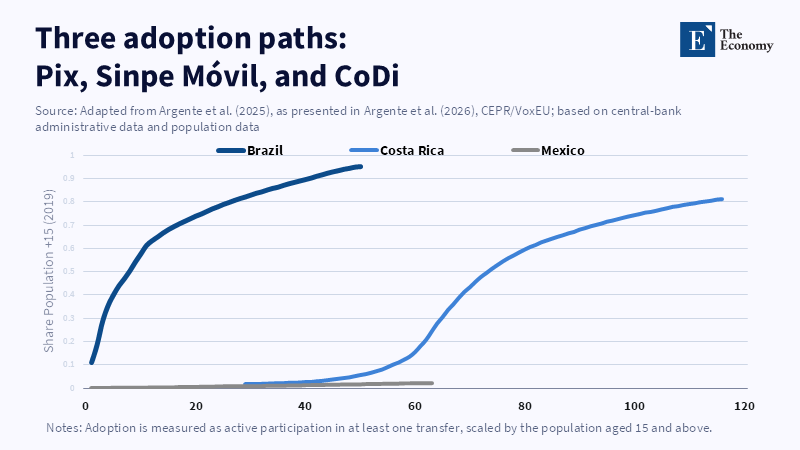

Recent payment statistics illustrate how wide the differences can be. In some markets, fast payments have entered public routine, while in others, they are still a niche. Brazil and Argentina, which in 2023 had among the highest levels of fast-payment use per person. India, for which the increase in total cashless volume from January 2023 to January 2024 was predominantly driven by fast services. Both can also focus on other signs of disparity. However, the lesson is the same: a digital rail can gain traction in society if it's affordable at the point of use and present in normal daily life. As contrasting examples of prevalence, the worst cases are those presenting a formal system that simply does not gain acceptance by merchants and, in consequence, by poorer users.

Interoperability renders applications as a form of public infrastructure

Interoperability is the silent argument that underpins effective payment apps for digital payment inclusion. Cash carries well because it is not locked in a brand. A bank note can circulate, hand to hand or float from kiosk to bus to farm gate to home without asking what network its receiver is on. Many digital systems still fail this fundamental cash benchmark. They may work within a bank, a wallet, or a platform, so there is little point in investing unless everyone else is on it too. If not, it becomes a costly extra for traders and an inconvenience for consumers, forcing households to juggle a toolkit of multiple apps, balances, cards and accounts.

This is also significant for small firms. A shop might try one digital payment route when it is still inexpensive, but turn away digital payments when each additional wallet requires another instrument, another fee, another period of settlement and another customer service connection. Merchant acceptance is called a 'business problem', but its underlying symptom is really a 'business inclusion' problem. If the corner shop remains cash-only, the neighboring community remains cash-based. Digital payment inclusion cannot be created by consumer infrastructure alone. It has to create acceptance at the local retailer as well.

A fractured market can still deliver high digital uptake, particularly among youthful and city-dwelling consumers. But it cannot eliminate cash as the ultimate fallback: if a particular wallet can’t pay another, if a small shop can’t accept dominant apps without taking a commission, or if a customer has to guess which code will work until he hits the right number – then the world remains incomplete. The same goes for public payments: a welfare transfer that is delivered digitally but is only spendable after withdrawal does not cut dependence on cash – it just shifts the line from a government office to an agent, or a cash machine.

The policy solution is not for a single private winner to take over the market, which introduces a new set of risks, where a dominant platform could facilitate payments while extracting tolls, collecting data and excluding competition. The preferable solution is to establish public rails that are universally accessible, with standard uniform interfaces, robust safeguards against fraud and a minimum of merchant frictions at the interface. The state does not have to operate every wallet, but it does have to define the competition rules that the other providers are competing on. The goal of digital payments inclusion is to have providers compete on the quality of the product, not on inherent closed systems.

Digital payment inclusion needs trust, privacy and a cash bridge

The most convincing critique of faster digital payment inclusion is that it can compound risk. That is true. Distrustful users are perhaps most vulnerable to the fallout of fraud, failed transfers, data misuse or a frozen account. The elderly and those with low literacy will likely require help to operate a wallet or banking application. Women might find mobile or SIM control by others within their household a barrier. In some low and middle-income economies, many would require assistance in reaping the benefits of a formal account. A forced move away from cash would punish the people it was meant to include.

This calls, however, for better design, not for slower reform. Trust can be fostered through good consumer protection, immediate resolution of grievances, transparent pricing and privacy norms comprehensible to everyday consumers. Smaller customers must clearly comprehend what failed, the responsible recourse provider and the probable resolution timeframe. They should not be required to possess the expertise of a lawyer in order to undo a transaction gone awry. They should not be compelled to convert all personal transactions into a data trail that can be monetized or exploited. Making digital payments inclusive does not justify offering privacy as an advanced feature for the affluent.

Another critical component is cash. Cash can be retired only once digital rails can withstand outages, crises, hacks and patchy connectivity. The optimal approach for at least the transitional period is dual access. Digitize wages, benefits, taxes and fees where digital access is actually preferable. Protect that access to cash for those not (yet) well served by digital rails. This is not a step back. It is a guardrail against false inclusion.

The agenda is clear. Quantify the income gradient of adoption, not simply the national volume of transactions. Mandate interoperability for key retail payments. Audit digital transfers by asking if the acquired digital money can be used for everyday transactions, not whether it can be received. Evaluate banks and fintechs by the failed-payment rate, complaint resolution, merchant acceptance and usage by low-income and rural customers. If these indicators become commonplace, inclusion in digital payments will no longer be a slogan, but an operational goal.

Predictions will not determine the future of cash. At the counter, on the clinic doorstep, at the bus stop, over the market stall and through the family remittance, cash will be determined. What determines cash use is whether digital payment inclusion provides the certainty now experienced with cash to low-income users; if it does not, cash will remain rational and if it does, cash will not be forced to go away. Therefore, the policy goal is not to push cash away, but to develop systems to which poor users can readily access, navigate unaided and trust uncoerced. Cash will go away when digital money is considered to deserve that place.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Argente, D., Gonzalez Alvarez, P., Méndez, E. and Van Patten, D. (2025) ‘Drivers of Digital Payment Adoption: Lessons from Brazil, Costa Rica, and Mexico’, NBER Working Paper No. 34280, National Bureau of Economic Research.

Argente, D., González-Alvarez, P., Méndez, E. and Van Patten, D. (2026) ‘Why some digital payment systems replace cash and others don’t’, VoxEU.org.

Di Iorio, A., Kosse, A. and Mustafi, I. (2025) ‘And so we pay: more digital and faster, with cash still in play’, CPMI Brief No. 8, Bank for International Settlements.

Drenik, G. (2026) ‘Cash On Its Way Out? Only If Digital Payments Can Work Together’, Forbes.

European Central Bank (2024) ‘Study on the payment attitudes of consumers in the euro area (SPACE 2024)’, European Central Bank.

Klapper, L., Singer, D., Starita, L. and Norris, A. (2025) The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy. Washington, DC: World Bank.

National Payments Corporation of India (2025) ‘Unified Payments Interface Product Statistics’, NPCI.

Reuters (2024) ‘Brazil’s instant payment transactions more than doubled on Black Friday’, Reuters.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.