Asymmetric Monetary Policy and the Firms That Break First

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

A rate hike and a rate cut do not carry equal force Tightening hits firms when financing constraints bind Policy should track credit damage, not only inflation

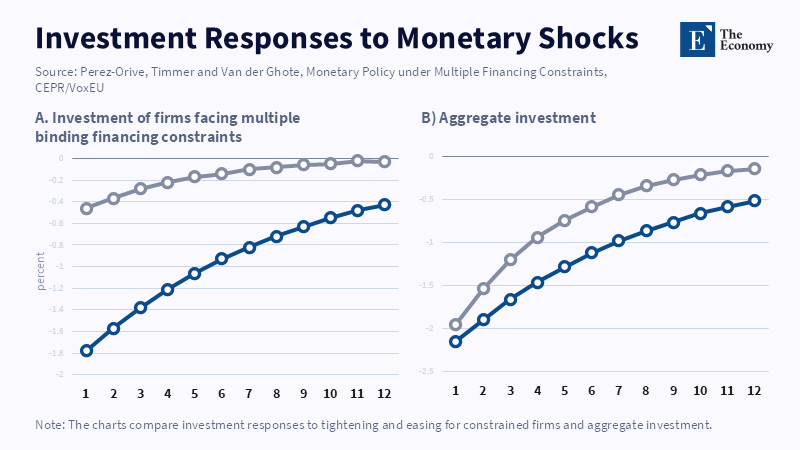

A single policy shift could appear minuscule on a central bank graph and massive on a firm's cash-flow report. A 0.25 percentage point hike and a 0.25 percentage point cut are often labeled mirror images. They are not. The latest firm-level research indicates that an easing signal can boost total investment by half the amount that the same tightening signal depresses it. This is the key point providing the foundation of asymmetric monetary policy. The logic is fundamental. When it gets tight, all burdensome loan terms hit the weakest point first. When it gets easy, the most relaxed part of the relief channel is still far from a firm’s balance sheet. This has implications for the size of the footprints that can be left by identical baby steps. One baby step can halt ventures, freeze hiring and break lines of credit. One baby step lower might only make banks more willing to talk. Policy must stop treating the actions as equivalent.

Asymmetric Monetary Policy Starts Inside the Firm

Old-style monetary policy is overly smooth. It envisions a policy rate sliding into market rates and then into credit, spending and jobs. That chain still exists, but it obscures where the shock really happens. The shock occurs in loan covenants, collateral schemes, interest-cover thresholds, floating debt, bank risk limits and managerial jitters. A firm does not check if the central bank nudged a perfect quarter point. It asks if the following payment pushes over a barrier, if profits still cover a burden, or if the bank will carry on a credit line. Asymmetric monetary policy is rooted in that space between the public rate and the private constraint. It is not just about interest rates; it is about which constraint becomes effective at the outset.

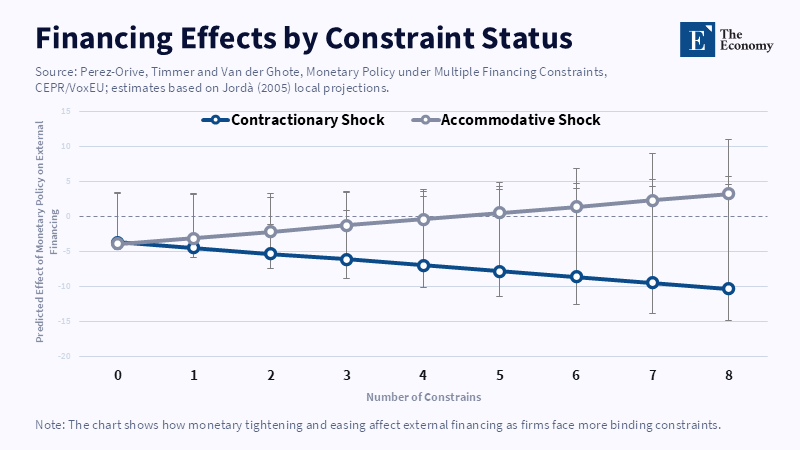

That difference is important because many firms confront more than one gate simultaneously. One firm may have a sufficient cushion of pledged assets but relatively weak current earnings. Another may be receiving strong sales but burdened with a relatively large amount of short-term debt. A third may pass bank tests but fail a bond-market test. When rates rise, all these gates can scream shut together. The tightest gate wins. Investment can collapse not because each individual lender produces a negative answer, but because one binding constraint is enough to halt expansion. When rates decline, the reverse may not happen with equal force; a lax gate cannot compensate for a different, more restrictive one. This is the reason asymmetric monetary policy should be judged by the weakest balance sheet, not by the average firm.

Labor-market evidence is equally persuasive. The U.S. Federal Reserve Bank of Richmond has shown that a 7-tenths-of-a-percentage-point raise was more clearly felt in higher unemployment than a 7-tenths fall. The estimated jump in unemployment after hiking was larger and sharper than the plunge after cutting. This does not imply that reductions in the rate create no effects. It rather implies that cuts inside the typical intentions of official statements tend to have a constraining effect via permission and creating confidence and future demand; while hikes have a constraining effect via immediate restrictions. Local firms can delay expansion after a reduction; they cannot always delay a higher debt burden after an increase. That is the asymmetry.

Why Easy Money Does Not Pull Every Firm Forward

Expansionary policy is never just an open green light. The green light is a good analogy only if the road is clear, the machine is fueled and the machine eagerly steers to move. A lower rate may normalize the credit price that can ease borrowing, but it can never intentionally lead a timid owner to decide on borrowing. It cannot return the lost sale. It cannot fix a weak balance merely by itself. It cannot make a bank suddenly forget a recent impairment. This is the quiet side of asymmetric monetary policy. Tight money can block actions quickly. Lax money relies on reliability, demand and trade credit channels to help produce activities.

The new SME data make this point concrete. The OECD's 2025 SME finance underscores show that the median interest rate for SMEs in the OECD scoreboard hit 6 percent in 2023, up from 4.4 percent in 2022. In the EU, small floating rate loans increased from 1.9 percent in July 2022 to a peak of 5.7 percent in November 2023. Another indicator revealed that a record 78 percent of SMEs suffered higher interest rates in 2023. These numbers show how quickly a rate cycle hits smaller firms. They also show that it may take longer to make the reverse journey. Even when headline rates are falling, banks may preserve higher fees, more stringent collateral criteria and broader risk screens. Credit does not thaw at the same rate as it freezes.

This should change how policymakers interpret weak investment following a cut. A low take-up rate does not necessarily mean that firms do not want to borrow because they are lazy, irrational, or too pessimistic. It could mean the second constraint is still in force. A firm that delayed investment for two years to conserve cash would not be willing to borrow to purchase a new machine just because the policy rate fell once. A lender that tightened lending criteria could not mean opening the credit door to the same borrower immediately. Demand could be sluggish. Inventories might be high. Owners could be wary that a further inflation shock will bring another hike. In such a world, the fact that monetary policy is asymmetric should not be surprising. It reflects rational behavior in the face of balance sheet damage.

Asymmetric Monetary Policy Hits Small Firms and Developing Economies Harder

The effect of the imbalance is more pronounced for small firms since they are closer to the constraint. Large firms can issue bonds, use cash flow, shift their borrowings between international borders, or bargain with several banks. But very often, small firms are left with one deposit, one overdraft, one seasonal credit line. They may not even have simple firepower to go looking for new finance. That explains why policymakers should look at small business credit data with fresh eyes in monetary debates. Small and medium-sized Enterprises (SMEs) account in all OECD economies for 99 percent of firms and generate somewhere between half and one percentage point of value added. A policy that considers them irrelevant is not neutral. It dismisses that corner of the economy where asymmetric monetary policy is most likely to hit.

Developing economies present another dimension. In many low- and middle-income countries, firms experience shallow capital markets, ultra-short loan maturities, ineffective collateral systems and banks that are packed with government paper. A rate increase increases working capital costs, shrinks banks' risk appetite and drags funds into the safer terrain of public paper. The pain is not limited to weak firms. Even healthy firms are likely to suffer increased rejection rates where banks have less room to lend. From Uganda's credit registry, the evidence suggested that a contraction in the monetary policy reduced credit supply, increased loan rejection, increased loan volumes and rates and exerted broad real effects. That is asymmetric monetary policy in a setting where the credit pipe is narrower from the start.

Recent cross-country evidence from developing countries presents the same lessons with additional nuance. In those economies, a 100 basis point increase in the policy rate made managers 12-19 percent more likely to report finance as major obstacle. Rate reduction increased loan application activity by roughly 17 percent, but the response to easing was not an echo of the response to tightening. Firms with closer relations to banks were somewhat more resilient, but unconnected firms were more sensitive and less resilient. This is the critical divide. It is not only small firms, but also large firms. It is connected firms, disconnected firms. It is baked firms versus barely banked firms. In developing economies, that divide can determine whether a rate increase reduces demand or crushes the economy's capacity.

Worse still, the macro backdrop has high stakes. The World Bank projects that emerging market income will stay below the pre-pandemic trend, with per capita income in 2027 around 6 percent lower than what was projected before the pandemic hit. It points to a downward drift in the growth of emerging markets that has occurred over decades, from 5.9 percent in the 2000s to 5.1 percent in the 2010s and roughly 3.7 percent in the 2020s. High policy rates, in this climate, are not bouncing off a neutral bottom. It’s bouncing off weak investments, sky-high debt and narrow fiscal space. A rate hike could still be needed to contain inflation. But it should be seen as a more formidable lift in countries where financial restrictions are already tight.

A Better Rulebook for Asymmetric Monetary Policy

A better rulebook begins with a simple question. Before each rate hike, central banks should consider which firms are approaching the edge of the constraint, not just where inflation will be in two years. That does not mean dropping inflation targeting. It means embracing the better map of transmission; rate hikes should come with dashboards on SME loan rates, rejection rates, covenant violations, floating rate loading, collateral pressures and maturity extensions. This data exists in many banking books, but it is usually supplemental. In an asymmetric world, it is paramount. The real question is not only whether policy is too tight. Instead, where does tightness become rationing?

A role is also needed for finance ministries and supervisors. If a tightening requires support, it should be narrower, temporary and linked to credit flow rather than cheap money for everyone. Credit guarantees offer a defense of good small firms without threatening the central bank's inflation objective. Development banks can offer an investment lifeline to firms when private banks pull back. Tax systems can permit faster loss carry-forwards for businesses struggling with interest overheads. Supervisors can observe whether banks are translating risk pressure into blanket denial. Such measures should not undermine the policy rate's message. They should avert the message from becoming a blunt shock for well-informed but financially constrained businesses.

The main critique is predictable. Any cushion, critics will declare, blunts the anti-inflation message. That is indeed an existing danger. Poor support can sustain feeble firms, increase demand and postpone the adjustment needed. But the right answer is not to deny asymmetry. It is the fashion supports that distinguish between demand, warmth and credit injury. A grant that boosts expenditure differs from a guarantee that protects a producer's working-capital line. A wide-rate subsidy differs from a two-year investment fund with a transparent qualification. Asymmetrical monetary policy requires better weaponry, not mush. A second is that central banks can't possibly hit every type of firm. And that's right, but right misses the point. They don't have to hit everyone. They have to stop firing the perverse shots of averages that pay wages, renew loans and sign investment contracts. A quarter-point rate rise is not just a macro message. It is a contractual flash flood. A quarter-point reduction is not a rescue plan. It is an offer many firms cannot take. That truth should shape the next rate cycle. This rate cycle should be judged not only by the speed with which inflation hits the target, but also by the amount of productive capacity lost along the way.

This opening statistic should disturb policy debate, for it unsettles a comforting symmetry. It shows that monetary policy is not a balanced switch. Tightening can destroy investment faster than easing can rebuild it. That does not make contraction wrong. Inflation can also hurt the firms most exposed to credit stress. It does mean each upward step should face a higher evidential burden and each downward step should be paired with proof that credit is actually reaching constrained firms. Asymmetry should become a defining feature of monetary policy, bank regulation and SME lending. A rate cycle begins with a baby step, but it matters whose balance sheet it lands on.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abuka, C., Alinda, R.K., Minoiu, C., Peydró, J.-L. and Presbitero, A.F. (2019) ‘Monetary policy and bank lending in developing countries: Loan applications, rates, and real effects’, Journal of Development Economics, 139, pp. 185–202.

Barnichon, R., Matthes, C. and Sablik, T. (2017) ‘Are the effects of monetary policy asymmetric?’, Federal Reserve Bank of Richmond Economic Brief, 17-03.

Dramé, D. and Léon, F. (2025) ‘Do firms react to monetary policy in developing countries?’, European Economic Review, 178, 105102.

Dramé, D. and Léon, F. (2025) ‘How does monetary policy shape economic activity in developing countries?’, VoxDev, 22 September.

Drechsel, T. (2023) ‘Earnings-based borrowing constraints and macroeconomic fluctuations’, American Economic Journal: Macroeconomics, 15(2), pp. 1–34.

Jordà, Ò. (2005) ‘Estimation and inference of impulse responses by local projections’, American Economic Review, 95(1), pp. 161–182.

Lian, C. and Ma, Y. (2021) ‘Anatomy of corporate borrowing constraints’, The Quarterly Journal of Economics, 136(1), pp. 229–291.

OECD (2025) Financing SMEs and Entrepreneurs: An OECD Scoreboard 2025. Paris: OECD Publishing.

Perez-Orive, A., Timmer, Y. and Van der Ghote, A. (2026) ‘Monetary policy under multiple financing constraints’, VoxEU, 1 July.

Tenreyro, S. and Thwaites, G. (2016) ‘Pushing on a string: US monetary policy is less powerful in recessions’, American Economic Journal: Macroeconomics, 8(4), pp. 43–74.

World Bank (2025) Global Economic Prospects, June 2025. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.