China’s Domestic Market Remains Stagnant Despite Massive Stimulus Measures as Property Collapse and Eroding Consumer Spending Power Take Their Toll

Authored On

Modified

Retail sales decline in May for the first time since December 2022 Industrial output remains resilient, but domestic demand weakness persists Property downturn remains the root cause, making prolonged deflation increasingly likely

China’s consumer market has entered negative growth territory for the first time since the lifting of COVID-19 lockdowns. As the property sector slump stretches into its fourth year, declining household asset values and weakening consumption are deepening simultaneously. Although Beijing has deployed massive fiscal resources to stimulate domestic demand, the housing market—the starting point for any meaningful consumption recovery—remains trapped in a downturn. With policymakers’ capacity to further support the property sector also diminishing, concerns are mounting over a prolonged period of deflation and domestic demand weakness.

First Consumption Decline Since the End of COVID Lockdowns

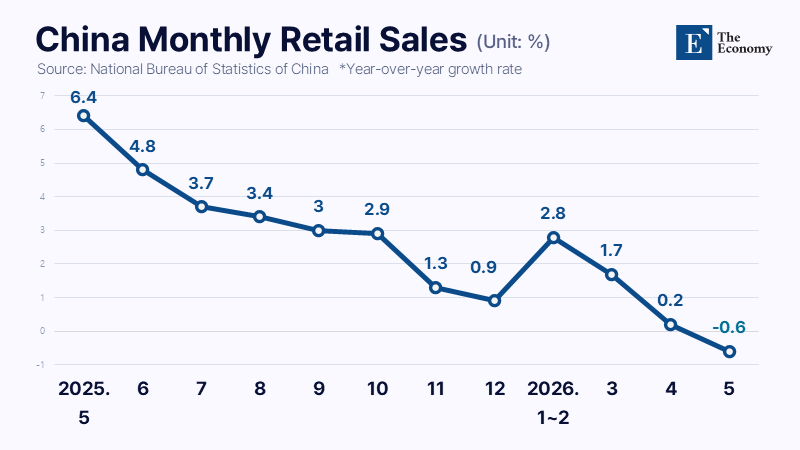

According to China’s National Bureau of Statistics on June 17, retail sales in May fell 0.6% year-over-year. The figure came in below both April’s reading of 0.2% and the market consensus forecast of 0%. More notably, monthly retail sales entered contraction territory for the first time since December 2022, when sales declined 1.8% during the height of the COVID-19 pandemic, marking the first such decline in three years and five months.

Fu Linghui, spokesperson for the National Bureau of Statistics, attributed the decline to base effects, noting that consumer promotion measures implemented in May last year had significantly boosted sales. He also cited unusually hot weather and frequent rainfall in some regions, which dampened offline consumption. Fu nevertheless emphasized that the consumer market remained stable overall and that the trend toward higher-quality consumption remained intact. However, many analysts argue that the decline—despite the presence of the May Day holiday period from May 1 to May 5—indicates that household spending continues to be constrained by uncertainty in the labor market.

Investment indicators also deteriorated. China’s fixed-asset investment for January through May declined 4.1% from a year earlier, according to data released the same day. The contraction widened from the 1.6% decline recorded during the January-April period. The property market also remained under pressure. Real estate development investment fell 16.2% year-over-year during the first five months of the year, worsening from a 13.7% decline in the January-April period. New home sales area declined 10.8%, compared with a 10.2% drop in the first four months. New home prices in China’s tier-one cities fell 1.7% year-over-year in May. By city, prices declined 2.1% in Beijing, 3.3% in Guangzhou, and 4.5% in Shenzhen. New home prices in tier-two and tier-three cities fell 3.2% and 4.2%, respectively.

In contrast, industrial production expanded 4.5% year-over-year in May, exceeding both April’s 4.1% growth rate and the market forecast of 4.3%. Exports also surged 19.4% from a year earlier, extending a strong rally for a second consecutive month. The result is a clear imbalance: supply remains robust while demand remains weak. This reflects a classic K-shaped growth pattern. Manufacturing and exports, supported by demand linked to renewable energy and artificial intelligence (AI), continue to post strong double-digit growth, while the property sector and private consumption remain mired in chronic stagnation.

Limits of Domestic Demand Stimulus Exposed

Since last year, China has made the construction of a strong domestic consumer market its top economic priority and has rolled out large-scale stimulus programs. Yet consumer sentiment has shown little sign of sustained improvement. Beijing’s consumption support campaign gained momentum through its trade-in subsidy program for consumer goods introduced last year. In the government work report, authorities allocated approximately $41.8 billion in ultra-long special sovereign bonds to support consumer goods replacement programs. The funding was equivalent to twice the related budget for 2024 and was designed to support demand for automobiles, home appliances, and digital devices through fiscal spending.

The scope of the policy expanded rapidly. The National Development and Reform Commission (NDRC) broadened subsidy eligibility beyond automobiles and household appliances to include microwaves, rice cookers, dishwashers, water purifiers, smartphones, and tablets. Consumers replacing older products became eligible for subsidies covering 15% to 20% of purchase costs, while smartphones and tablets below designated price thresholds were also included in the program.

The Chinese Communist Party Central Committee and the State Council subsequently unveiled a Special Action Plan for Boosting Consumption in March last year, further broadening the policy agenda. The plan encompassed income growth initiatives, reductions in household financial burdens, minimum wage increases, employment support, childcare subsidies, expansion of service-sector consumption, and measures to stabilize stock and property markets. The objective was to support domestic demand through simultaneous improvements in income, assets, welfare, and employment rather than relying solely on short-term subsidies. The measures initially produced some results. Automobile and appliance sales rebounded alongside subsidy disbursements, while expectations for consumption recovery improved in several regions. Retail sales growth exceeded market forecasts during periods when policy support was most concentrated.

The momentum, however, proved short-lived. Consumption gains remained concentrated in subsidy-supported categories. Automobile and appliance sales increased, but spending on restaurants, retail services, and housing-related sectors failed to show meaningful recovery. The consumption rebound remained narrowly focused and did not spread across the broader economy. Signs of diminishing policy effectiveness have become increasingly apparent this year. Generous subsidies introduced last year pulled forward a significant portion of demand for automobiles and appliances, while some local governments exhausted their budgets earlier than expected, forcing support programs to be scaled back or suspended. In many regions, sales growth slowed sharply once subsidies expired.

Property Slump Continues to Undermine Consumer Confidence

The fundamental constraint on household consumption remains the property market downturn. Despite extensive support measures from Chinese authorities, the housing market has failed to emerge from its slump. Home prices have been falling continuously since peaking in August 2021. According to National Bureau of Statistics data, existing home prices had fallen 22.5% from their peak as of April this year, while new home prices were down 13.2%. Housing transaction volumes have also declined 53.8% over the past five years. The property market has therefore remained in contraction for more than four years.

Against this backdrop, Beijing’s efforts to rescue the property sector are steadily losing momentum. Since 2022, authorities have implemented a range of measures including mortgage rate cuts, easing of purchase restrictions, acquisition of unsold housing inventory, and support for developers. Since last year, however, policy priorities have shifted. Rather than deploying large-scale fiscal stimulus as in the past, policymakers have focused on localized measures such as regional deregulation, urban redevelopment projects, and support for larger families. Authorities have refrained from establishing additional property funds or providing large-scale liquidity injections. Even following the collapse of China Evergrande Group, the government has prioritized financial risk management over broad-based developer bailouts. Concerns over potential defaults involving Country Garden and Vanke persist, yet the scale of support has declined significantly compared with previous years.

The reasons are clear. Real estate’s share of China’s gross domestic product fell from 8.3% in 2020 to 5.9% this year. Revenue from land-use rights sales, once a critical source of income for local governments, declined from approximately $1.21 trillion in 2021 to about $583 billion last year, effectively being cut in half. Policy priorities have also evolved. Major investment banks estimate that China’s leadership is increasingly concentrating policy resources on advanced manufacturing, artificial intelligence, semiconductors, and renewable energy industries rather than real estate. Property market stabilization remains a policy objective, but it is steadily losing its position at the center of China’s growth strategy.

Yet a meaningful recovery in domestic consumption remains unlikely unless the property market recovers. Falling home prices reduce household wealth, and declining asset values suppress spending. Amid persistent deflationary pressure, Chinese households continue to favor savings over consumption. As a result, even if Beijing introduces additional stimulus measures, the pace of domestic demand recovery is likely to remain limited. With the prospect of large-scale fiscal support for the property sector fading, the combination of falling asset prices and weak consumption appears set to persist for the foreseeable future.

Similar Post