Federal Reserve Independence: What Kevin Warsh’s First FOMC Reveals

Keith Lee is a Professor of AI/Finance at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). His work focuses on AI-driven finance, quantitative modeling, and data-centric approaches to economic and financial systems. He leads research and teaching initiatives that bridge machine learning, financial mathematics, and institutional decision-making.

He also serves as a Senior Research Fellow with the GIAI Council, advising on long-term research direction and global strategy, including SIAI’s academic and institutional initiatives across Europe, Asia, and the Middle East.

Authored On

Modified

Warsh’s first FOMC resisted the expected political script Fed independence is proven through decisions, not appointments The real test comes when policy and politics collide

A 12-0 vote can say more than many months of political debate. In Kevin Warsh's first convening as Fed chairman, all voting members supported a hold on rates at 3.5% to 3.75%. The outcome failed to deliver the rate cuts the White House had desired and left the door ajar for higher rates later in 2026. Nine policymakers set the year-end rate above the current median, while Warsh opted out of providing a personal rate outlook. The result matters. It is not a guarantee that the Fed will be independent for the duration of its term. One gathering can never make that determination. It does, however, erode the argument that the new chairman would merely obey the president's command. The more relevant indicator is not the president who put the chairman into office. It is whether the institution can shoulder an unpopular decision, clarify its remit and leave open options when political winds blow the other way.

Federal Reserve Independence Is Tested Through Policy, Not Appointment

Sometimes, the real evidence on central bank control is different from what the debate begins with: political commitments, previous speech and the preferences of the president who nominated him to be chair. While these indicators illuminate the context that might exert influence, they reveal nothing about how a chair will behave once in a committee with a statutory mandate, voting procedures, public statements and market discipline. Federal Reserve independence, then, is no moniker granted at the time of appointment. It is a pattern of behavior: when a chair defies analysts' forecasts, defies a veto-empowered committee and defies the constraints of new information, that is when the chair is independent. The bar is actually a standard of greater exactness than the one where chairs make overlapping promises at confirmation hearings and certainly a more just criterion than the pre-emptive assumption of capture. Warsh's experiment in chairmanship left the chairman out of line with the White House; his opening gambit surfaced no rate cut; it seems that the debate should not be abandoned but its assumptions reevaluated.

Recent evidence supports this emphasis on conduct. Legal protections help but they do not fully prevent political influence. An examination of 118 central banks showed that reported political pressure or government interference was at about a tenth of the institutions in any given year and at least once during the entire period for 39% of them. The majority of the pressure was toward a more accommodative policy. This is why the relevant question is not: Does pressure exist? The answer is that it almost always does; the relevant question is: Does policy bend? An analysis of 132 governor shifts in 28 countries for the period 2000 to 2024 showed that 38% of the transitions were politically motivated. These transitions were thrice as likely as routine transitions to result in the appointment of leaders with unorthodox policy views. The countries experiencing such transitions also had long-term inflation expectations more than two percentage points above target. Formal independence may quite easily survive on paper while actual independence erodes away.

Warsh's First FOMC Did Not Act as a Puppet

The June meeting was an early example of that distinction. Despite having spent months saying that borrowing costs were high, the committee chose to leave rates unchanged. There was a vote and it was unanimous. The statement noted that inflation remained above the Committee's 2 percent objective and offered no suggestion of a reduction in rates being imminent. The new projections were even more reluctant to allow an easing of policy. Median total PCE inflation for 2026 was increased to 3.6 percent (up from 2.7 percent in the March statement). Median core PCE inflation increased to 3.3 percent. The median year-end policy rate was increased to 3.8 percent (up from 3.4 percent in the last projection round). These numbers did not come from Warsh alone. They came from the Committee. That is the point. Were Warsh a puppet, it would be reasonable to expect him to tip the institution toward a political outcome. The first meeting, in fact, featured an institution leading its chair into a collegial process grounded in inflation data and collective judgment.

Warsh also declined to offer his personal dot in the Summary of Economic Projections. That may seem evasive but it was certainly not a subtle signal for lower rates. He was consistent with a long-established belief that forecasts are not commitments. Nor did he concur that the 2% monetary policy objective should be part of the process that the Fed has yet to prove itself capable of achieving. That stance exceeds the rule that a chair chosen by a president who favors easing might have expected. It leaves little room for political haggling. When a target exists in a finite action space, each move must be justifiable vis-à-vis a verifiable outcome; hence, the chair's argument over models, over data, or over reasonable responses. The bottom line that inflation should settle at 2% remains the ultimate expectation.

The broader reform blueprint was unveiled in late August. Warsh established task forces on inflation, communications, data, productivity, jobs and the balance sheet. At the same time, the plan could make the Fed more focused and more ready to act. The blueprint’s early approach suggests the opposite. It does not remove the committee’s independence by replacing its open-ended remit with a chair-driven rule. Instead, it asks how the Fed collects evidence, communicates as uncertainty rises and keeps its policies distinct from fiscal policy. Warsh’s vision was not to minimize the scope of the Fed’s interest. His vision was to broaden the scope of the economy but narrow the scope of policy. He also felt that monetary policy should retain its independence despite acquiescing to the Fed board during its run-in with the Speaker of the House. That is not a recipe for ending the Fed’s independence. It is a simple operational philosophy. It privileges the mandate over a standing promise to lend them cheaper money.

Federal Reserve Independence Permits Risk, but Not Secrecy

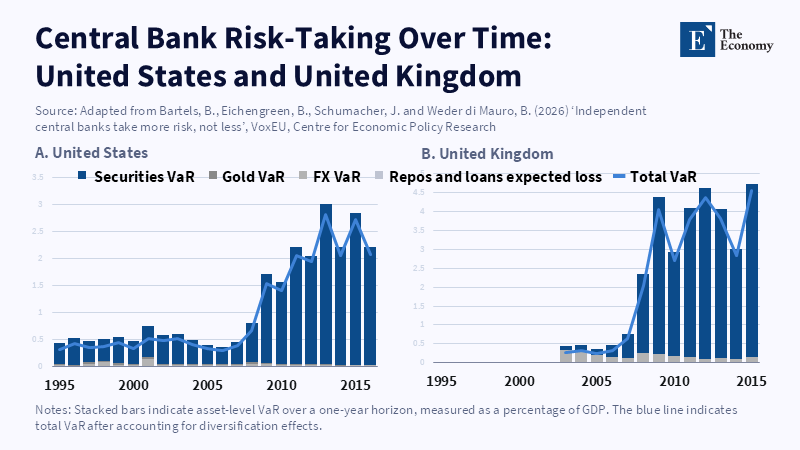

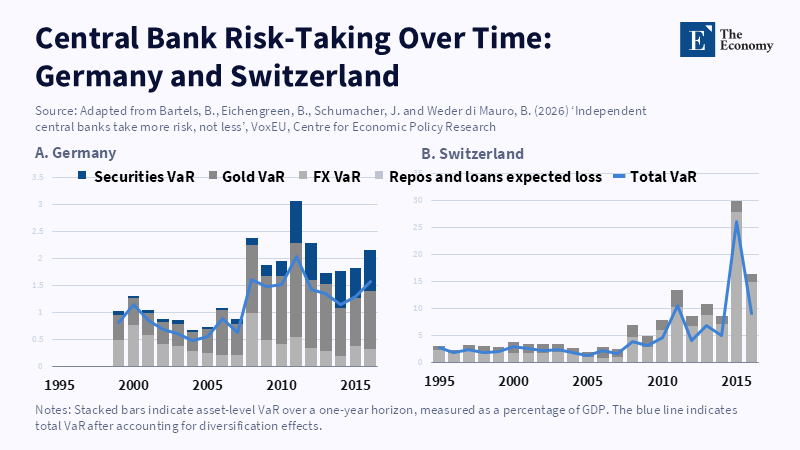

Research on central bank balance sheets adds another point. The more independent a central bank, the more likely it is to take financial risk; it does not always select the safest-looking policy. Indeed, it is the one with the added flexibility to go beyond the traditional policy role in pursuit of its mandate that often adopts riskier policies. A study of 18 advanced-economy central banks drew from more than 330 balance sheets over 22 years (from 1995 through 2016). It quantified portfolio risk using a one-year value-at-risk model. Mean balance-sheet risk increased from below 1% of GDP in the mid-1990s to around 3% at the end of the sample. When policy rates declined from 5% toward zero, the estimated risk more than doubled, from roughly 0.8% of GDP to 2%. Banks with greater independence assumed riskier positions, particularly when fiscal authorities adopted stricter austerity policies. The point is not that risky actions are always effective. The point is that independence broadens the choice of actions when the usual rate changes prove insufficient.

This helps explain why the Warsh debate should not be framed mainly as: is he hawkish or dovish? A truly independent Fed could cut the funds rate while a president called for restrained policy. It could raise the rate in a time of high growth, while a president held demand down. It could run a leaner balance sheet for years, then, when a crisis hit, temporarily expand it significantly. Independence does not mean a single, defined policy course that is permanent. It is the freedom to choose between expensive alternatives without having to subordinate the short-term needs of the state to the dictates of the longer-term cycle. That freedom also allows Warsh to reject forward guidance, even if it entails rigid and perhaps overconscious decisions, which makes his views on transparency so difficult to understand; unqualified promises, after all, can come back to limit the options future policymakers face.

The same reform could carry a real danger: less guidance can mean less accountability, higher risk premiums and more uncertainty over borrowing costs for households and firms. A silent central bank can still have to explain the rationale for what it does. The Fed need not be forced to publish a false map of the future. The Fed needs clearer evidence about current conditions. Each statement could provide the inflation measure, labor indicator and financial condition that affected the vote. Minutes can report the range of views without using the session for personal theater.

The chair can explain what would alter the committee’s judgment, even without showing a rate path. Congress can evaluate results based on the statutory task, not the implicit demand for a path. Rules like these could allow greater flexibility while constraining secrecy. Independence cannot be based on mystery or personal assurance. It must rest upon a transparent process. Warsh's brief statement and missing dot can only be justified if the Fed substitutes explanations of how it reacts to current data for its guidance based on forecasts.

The Hard Test Is Whether the Fed Can Disappoint Anyone

That barely passed the first test of each meeting. The rate decision was defensible because inflation was high, growth was solid and the committee had time to wait. Harder decisions come when the mandate points in opposite directions. A sharp slowdown in labor markets might argue for cuts even if inflation remains above target. A new energy shock might push up prices while reducing real income. A break in the market might call for rapid balance sheet adjustment, from a chair who seeks a leaner Fed. Independence, then, will require more than resistance to the president. It will require resistance to the chair's own long-standing view. That is why committee process matters. Warsh's refusal to sign on to a dot should not allow him to stand aloof from the forecast battle. His task forces should not give way to a back door for governors and Reserve Bank presidents. Reform should enhance shared judgment, not supplant it with a personal credo.

On the basis of cross-national data from 1972 to 2023, a study of 155 countries estimated that a developed country, transforming from the lowest to the highest quartile of legal central bank independence, would experience an incremental annual inflation rate decline of 3.7 percentage points over time. The projected benefit for emerging economies has been just over 10.3 points. These calculations are all model-driven effects, not automatic outcomes and the authors point out that trust needs to be established gradually. Central bank independence matters since it influences expectations well ahead of when a policy step takes effect. As soon as participants expect a political broker to be in a position to take precedence over the target, each inflationary jolt turns more costly to kill. Costs show up in wage negotiations, bond yields, contractual relations and the pace at which transient price spikes diffuse. There is therefore nothing charitable about upholding Federal Reserve independence. It is an effective way of cutting down the costs of raising inflation payback to levels consistent with economic efficiency.

That protection needs the support of both sides. The White House should stop using rate cuts to signal intent. Congress should uphold the Fed's control of the tools of money policy while requiring them to come forth periodically with testimony, clear ethics standards and objective performance reviews. The Committee should continue to cite votes, projections, minutes and data-based rationale as its own reason for action even if it is reformatted. Warsh should encourage dissent today and preannounce that no single theory has precedence over the committee's terms of reference. Repeatedly, election eve decisions by no choice of the hour are the test of independence, not the partisan hopes for who sits in the chair.

The first 12-0 vote should therefore be taken as confirmation, not pardon. It demonstrated a Fed committed to maintaining policy when the man who appointed it sought easing. It demonstrated a Chair prioritizing the 2 percent target over a speedy political triumph and leaving actions potentially upsetting to the markets and to the President still available. Now, the first 12-0 votes can become the start of a lasting standard. A decision should always be made in an industry marathon mandate; everyone should be able to challenge it in committee.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Bartels, B., Eichengreen, B., Schumacher, J. and Weder di Mauro, B. (2026a) ‘Central bank independence and risk-taking at the zero lower bound’, CEPR Discussion Paper, No. 21570 and ECB Working Paper Series, No. 3079.

Bartels, B., Eichengreen, B., Schumacher, J. and Weder di Mauro, B. (2026b) ‘Independent central banks take more risk, not less’, VoxEU, 22 June.

Binder, C.C. (2021) ‘Political pressure on central banks’, Journal of Money, Credit and Banking, 53(4), pp. 715–744.

Board of Governors of the Federal Reserve System (2026a) ‘Federal Reserve issues FOMC statement’, 17 June.

Board of Governors of the Federal Reserve System (2026b) Summary of Economic Projections, 17 June.

Board of Governors of the Federal Reserve System (2026c) Transcript of Chairman Warsh’s Press Conference, 17 June.

Bolhuis, M.A., Mano, R.C. and Thorell, H. (2026) ‘The macroeconomic consequences of undermining central bank independence: Evidence from governor transitions’, IMF Working Paper, No. 2026/040.

Canepa, F. (2025) ‘Mantra of central bank independence shaken by Trump moves on Fed’, Reuters, 26 August.

Delaney, S. (2026a) ‘From a predictable Fed to a market-responsive Fed: A price stability doctrine unshaken by short-term shocks’, The Economy, 19 June.

Delaney, S. (2026b) ‘Chair Warsh removes the “turn signal,” adopting the playbook of the Greenspan Fed’, The Economy, 22 June.

Eijffinger, S.C.W. and de Haan, J. (2026) ‘Central bank independence: An update’, VoxEU, 22 April.

Keith Lee is a Professor of AI/Finance at the Gordon School of Business, part of the Swiss Institute of Artificial Intelligence (SIAI). His work focuses on AI-driven finance, quantitative modeling, and data-centric approaches to economic and financial systems. He leads research and teaching initiatives that bridge machine learning, financial mathematics, and institutional decision-making.

He also serves as a Senior Research Fellow with the GIAI Council, advising on long-term research direction and global strategy, including SIAI’s academic and institutional initiatives across Europe, Asia, and the Middle East.