Supply Chain Inflation and the Risk Premium of Delay

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Supply chain inflation begins before costs fully appear Firms price delay as a margin risk Competitor reactions can turn disruption into persistent inflation

Global supply chains experience a one-month-or-longer disruption every 3.7 years, on average. This should transform the inflation debate. It shows that supply problems are not special; they are endemic conditions applying to pricing decisions. Supply chain inflation begins where delivery delay is seen as part of the margin calculation. A delayed container, a missing microchip or a blocked road does not merely raise today's freight bill; it alters firms’ conception of tomorrow’s uncertainty. Producers start to safeguard cash flow, wholesalers to lengthen buffers and retailers to reduce discounts. Competitors observe scarcity and act accordingly. By the time the product hits the shelf, the original shock has been marked up, insured against and multiplied across the market. The policy mistake is in assuming a short cost shock. The more acute truth is that delay takes on a risk premium and that premium can become self-reinforcing.

Supply Chain Inflation Begins Before Costs Appear

The key policy question now is no longer whether supply shocks can push prices; the answer to that is clear. It is just how far the impact extends beyond the initial bill. The better way to think about the impact is as a propagating channel. Inflation in supply chains transmits in three interconnected steps. First, a business experiences a delay or loss that threatens sales, margins or inventories. Second, the business minimizes margin loss by raising margins, eliminating discounts, modifying pack rates or product features, or whatever is necessary to hold service commitments. Third, competitors that observe the same signal of scarcity pursue simultaneous action, even if the corresponding direct shock is smaller. That is the moment when a narrow supply price shock morphs into an all-encompassing price shock. It is not just pass-through. It is risk-through. Firms price for not just the actual cost they recently bought, but the one they think they might soon face.

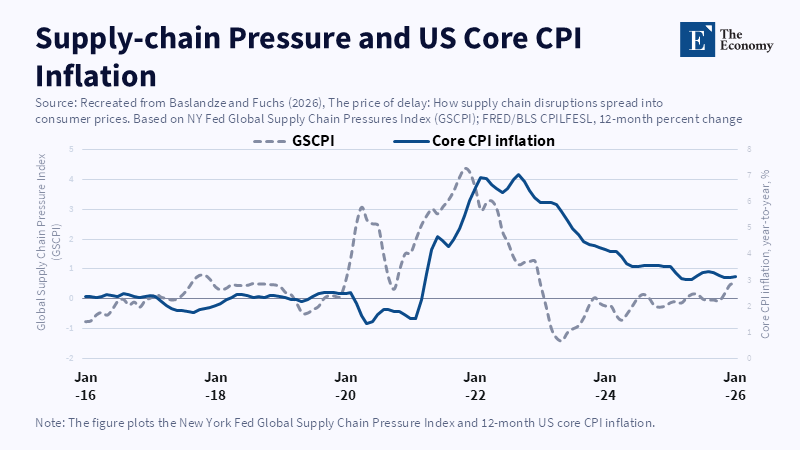

Recent data confirm why this channel still matters. Global pressure on supply chains fell away from the peak of the pandemic but did not settle into a new normal of subdued flows. Disruptions in the Red Sea and Panama Canal have shown that new stresses can happen before the memory of the last has faded. Transit along the Suez and Panama corridors more than halved in 2023, nearly doubling transit times, increasing operating costs and changing route choices. By mid-2024, the Shanghai Containerized Freight Index had more than doubled its value from late 2023. UN trade analysts suggested that persistently higher costs might push world consumer prices up by 0.6% by 2025, with more pronounced effects felt in small island economies. These are not large effects on their own. Their scale is enough to matter when inflation expectations are nervous and companies are sensitive to cost risk.

Timing is the key issue. A supply chain shock doesn't have to hit every firm at the same time in order to influence market prices; it has only to destabilize future stocks of supply. Many firms operate with no or modest buffers because storing inventory is costly. Once the term of delivery becomes less predictable, the value of inventories rises. A shopkeeper with inventory on the shelf faces little temptation to discount it; a manufacturer with uncertain inputs may quote higher prices for future orders; a distributor will add a risk buffer, since buying the same good next month may, again, cost more. This is how supply chain inflation begins before the cost data is available. Prices move first; accounting data comes late.

The Margin Channel Converts Delay Into Price Risk

The margin channel is the hidden link between logistics and inflation. Standard cost pass-through is too neat: it assumes a business gets a larger input bill, adds some fraction of that bill onto its final price, and moves on. No business works that way. Real firms face slower, messier choices. They face working capital constraints, supply delays, overtime, late penalties, rush fees, stock-out costs, and the risk of a tarnished reputation in the eyes of their customers. Firms may then choose to absorb some cost increments, raising prices to a point in excess of what a simple, last-invoiced price change might warrant. This need not be price gouging, not so long as it remains the strategy of many individual businesses.

The evidence from the pandemic period affirms this history. A study using aggregate monthly data concluded that supply chain disruptions represented the largest contributor to unanticipated U.S. Core PCE inflation during the January 2020-December 2022 period. This does not imply demand was irrelevant. Another research body has established links between producer and consumer prices and the shift of shipping and delivery measures. It finds that delivery lag can be directly translated into the prices that consumers pay to a large extent. The lesson is clear: not that every delay is passed entirely to consumers, just that persistence matters. A delay of one week can be exhausted through stocks, contracts, or patience. Repeated shortfalls alter the technique of price-setting. They make every pricing list increasingly defensive.

That defensive pricing has a spiraling impact without a wage-price spiral in the middle. A supplier raises prices for fear of future shortages of inputs. Its customer accepts the increase because switching suppliers takes time. The customer then raises its prices because its margin narrows. The next player in turn does the same. All the time each wave of the initial shock combines with fear of losses, stress on cashflows and the squeeze of bargaining power. The total impact can more than double the original extra cost. This is why supply chain effects can seem so out of proportion. There are multiple layers of premium for risk. Each layer may be a justifiable cost for the company involved, but the cumulative effect is a more and more widely spread and more persistent level of prices. That is the spiral risk policymakers often notice too late.

Why Supply Chain Inflation Spills Across Competitors

The competitor response is what translates a firm-level disruption into a market-wide squeeze. When one brand can't replenish, others have a margin to price with. They don't necessarily have the same delay, but they do face less pressure to keep prices low. Rationing makes competition less fierce. It also alters the narrative customers tell themselves. A higher price can feel less like a firm decision and more like the "normal" price of a challenging market. This revised expectation can protect firms. In markets with centralized suppliers, tight inventories or powerful brands, this cover can be significant. Supply chain inflation then propagates via imitation as well as through enforced costs. The end result is a market that reprices around rationing, not merely around the checks that went out, and that this repricing can persist.

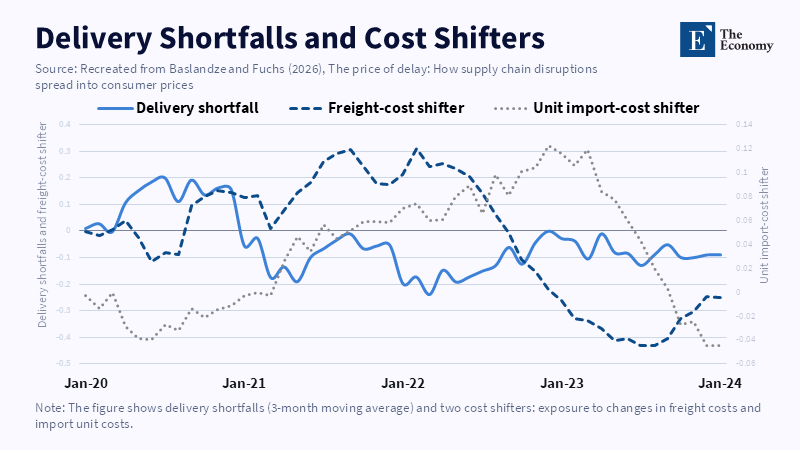

Micro evidence proves this in the concrete. Newer shipment-and-receipt evidence notes that a firm's own delivery shortfalls have a price pass-through near 0.25 to 0.27 in preferred estimates. But prices also respond to rivals' shortfalls. That is estimated to be around 0.11 to 0.13, about half of the direct one. That is the all-important insight: a firm can increase prices even when its competitors are struck. Even firms that do not directly import can respond to the disruptions of another importer in the same product market. Price pressure from flow disturbances can thus spread far beyond the firms that have a port, vessel or foreign source on the agenda. The supply chain does not stop at the border: it terminates inside the pricing decisions of every firm selling close (or sometimes distant) substitutes and there is no a direct import line involved.

This also sheds light on why headline freight rates may be misleading for policymakers. A shipping index could be declining while downward pricing pressure continues. Contracts are strung out. Stock is uneven. Companies may have restored inventories at higher costs. Some may keep prices high to seek to recover margins lost during the shock. Others may hold off on a price cut until their competitors have gone first. The net effect is a slow withdrawal from supply chain inflation, even after physical flows begin to normalize. In 2025, global container prices saw a temporary, dramatic drop through much of the year as capacity increased and trade timing shifted. The same period revealed how swiftly tariffs, early bookings and route risk could propel rates back up again. The bottom line is straightforward. Cheaper transport markets do not necessarily translate into cheaper shopping baskets.

Supply Chain Inflation Is A Risk-Management Problem

Sometimes dividing policy into narrow categories is unhelpful. Monetary policy focuses on demand. Industrial policy focuses on supply. Competition policy addresses market power. Supply chain inflation encompasses demand, supply, and market power. Central banks should do something if broad inflation persists. Interest rates can't heave a vessel, open a canal, or substitute for a missing input. Tight policy can bring down demand but also capital spending on warehouses, ports, digital tracking, and supplier diversification. This calls for a two-track approach. One track should prevent second-round inflation. The other should reduce the risk that the next delay triggers another price rise.

The first practical policy step is better diagnostics. Inflation dashboards should be capturing more than just energy, wages, and demand. They should incorporate delivery lags, port stress, inventory-to-sales ratios, failures to stock, import concentration, freight contracts and product-specific vulnerability to chokepoints. The World Bank's maritime stress work demonstrates that vessel delays can be computed in lost container space and correlated with freight rates. Yet such a diagnostic tool should not be parked outside the inflation policy. It should be parked alongside. If a country sees which goods are subject to concentrated supply risk, it can prepare before firms price a wide risk premium. A pre-emptive early warning is preferable to an accurate late report, after margins have already responded.

The second is targeted resilience. Wide reshoring is far too expensive and also far too blunt. It can lead to higher prices if it substitutes inefficient trade for costly duplication. The smarter solution is targeted redundancy. Governments should identify the network of vital inputs, promote dual sourcing wherever import concentration is high, streamline customs procedures, give priority to ports and inland terminals, and maintain strategic stocks of those products where supply disruption entails high social costs. Europe's single market can double up as a shock absorber for the same reason, if firms can bypass obstacles by selecting suppliers across its borders quite quickly. The idea for firms is similar. Resilience is not merely about logistics. It concerns pricing too. The ability to replenish stocks faster means a company has less scope to charge customers for caution and less incentive to copy rivals defensive price increases.

The Final Test Is Whether Margins Fall When Risk Fades

The critics will argue that this provides an excuse for firms to push up prices. There is a real risk of that. But the answer is not to overlook the supply channel; it is to measure it more accurately and to defend competition more vigorously. When shortages ease, watch margins as carefully as costs. Watch business conduct and costs together, and the trader's costs, like you do the trader's sets. Keep a close eye on the sectors where only a handful of firms dominate vital capacity, and where rebates track price parity. Keep a close eye on the sectors where prices, at the same time as freight prices fall, remain elevated. Transparency can help. So can more energetic merger control in warehousing, logistics, food processing, and other consumer-facing sectors. Supply chain inflation will be more damaging if it combines with market power. Resilience and competition policy must therefore work hand in hand, with speedier data and clearer indicators for intervention.

An important part of the conclusion is political. Households don't feel inflation as a model. They feel it is a broken promise that normal prices will return when the crisis is over. When prices remain high because each individual firm has built in a buffer, trust wears away. That trust is valued by monetary authorities, policymakers, and capital markets. A world having a one-month interruption every few years cannot operate on the premise that shocks will prove transitory. The challenge is to eliminate the lag between a supply shock and the passage of policy. None of this should be taken as normal. Thinking of delay as a one-off operation is how supply chain inflation turns into a spiral. Thinking of delay as a systemic issue and a risk to be managed is how that spiral can be countered.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Amiti, M., Itskhoki, O. and Konings, J. (2019) ‘International shocks, variable markups, and domestic prices’, The Review of Economic Studies, 86(6), pp. 2356–2402.

Baslandze, S. and Fuchs, S. (2026) ‘The price of delay: How supply chain disruptions spread into consumer prices’, VoxEU, Centre for Economic Policy Research.

Baslandze, S. and Fuchs, S. (2026) ‘The price of delay: Supply chain disruptions and pricing dynamics’, Journal of International Economics, forthcoming.

Benigno, G., di Giovanni, J., Groen, J.J.J. and Noble, A.I. (2022) ‘The GSCPI: A new barometer of global supply chain pressures’, Federal Reserve Bank of New York Staff Reports, No. 1017.

Bonham, D., Demmers, J., Goy, G., de Grip, J., Heerma van Voss, B., de Leeuw, D., Mehlbaum, C., Smadu, A. and Swierstra, R. (2026) ‘Global supply chains and European economic vulnerabilities’, De Nederlandsche Bank Analysis.

Gordon, M.V. and Clark, T.E. (2023) ‘The impacts of supply chain disruptions on inflation’, Federal Reserve Bank of Cleveland Economic Commentary, No. 2023-08.

Lund, S., Manyika, J., Woetzel, J., Barriball, E. and Krishnan, M. (2020) ‘Risk, resilience, and rebalancing in global value chains’, McKinsey Global Institute.

United Nations Trade and Development (2024) Review of Maritime Transport 2024: Navigating Maritime Chokepoints. Geneva: United Nations.

United Nations Trade and Development (2025) Review of Maritime Transport 2025: Staying the Course in Turbulent Waters. Geneva: United Nations.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.