When Negative Deposit Rates Break the Bank Habit

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Negative deposit rates do not just change returns; they change trust Denmark shows how households cut deposits when banks pass through negative rates Japan shows how low returns can push savers toward cash, caution, or global risk

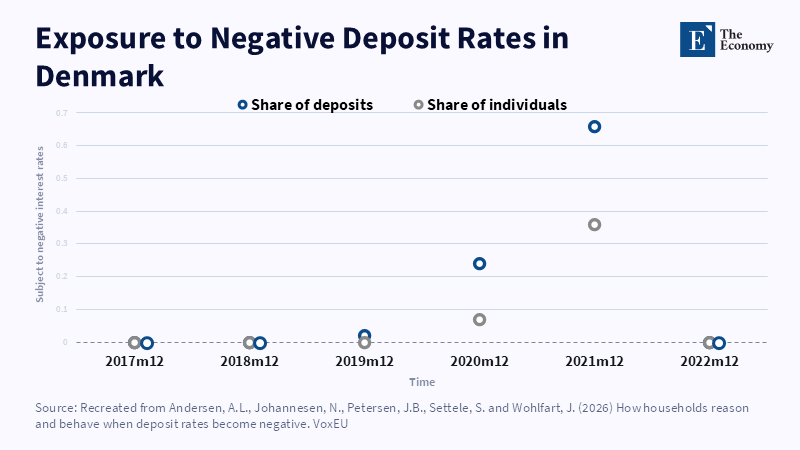

A bank deposit was supposed to be the quietest contract in capitalism. Money goes in. The saver gets a tiny bit of interest. The bank turns pooled depositor trust into credit. Negative deposit rates interfere with that classic bargain. Denmark demonstrated how quickly sentiment can shift. By the close of 2021, about one-third of Danish individuals and roughly two-thirds of personal deposits had negative deposit rates. The fee was frequently negligible; the message was enormous. It appears to be transmitted to households that their most secure depository had also become the place where their money would slowly shrink. That is the real economic problem. Negative deposit rates don't just reduce the income generated from savings; they demand from the population deep confidence in an agency that now appears nothing but a fee collector. If this confidence ebbs, capital will still circulate, but it may be circulating through accounts, not institutions.

Negative Deposit Rates Are More Than a Price Signal

The norm for negative deposit rates looks simple. If saving pays less, people should be happier to spend the money or move it into riskier assets. That should boost demand, hold up prices and help an economy escape weak growth. In the standard model, 0 has no special significance. Reducing a rate from 0% to -0.5% should be just as effective as reducing it from 5% to 4.5%. The saver compares the returns and adjusts their behavior. The policy rule consequently finds its way through the banking system and into the real economy. The difficulty is that the household deposit is not a normal asset. For many people, it is the foundation of their daily financial life. Money in wages flows into it. Money for bills flows out of it. Money for emergencies stays in it. A deposit account is both a financial instrument and a trust habit.

Negative deposit rates seem quite different from normal low ones: getting so little is irritating and paying the bank to hold savings seems unfair. It warps the meaning of the bank as safe. Saving starts to look like exposure and prudence begins to look like something to avoid. The policy debate must therefore be broader than just short-term consumption; the underlying issue is whether negative deposit rates erode the bank account, the prime repository of household savings, as the default and trusted repository of household wealth. Policy can divert cash and still undermine confidence; it can raise spending for a time, while conflating banks with last-resort status, which is a very high price to pay if economies still look to banks to translate deposits into credit.

Denmark Shows the Strength and Risk of Negative Deposit Rates

Denmark provides the case of a broad pass-through to households. By 2019, one Danish bank was charging -0.75% on all personal balances above DKK 750,000, about USD 114,500. Gradually, virtually all banks introduced negative rates and for many, the threshold values came down to DKK 100,000, about USD 15,300. This was no longer confined to the ultra-wealthy. It could impact a household selling a flat or receiving an inheritance, or saving for a down payment. The bank account was a thing to be managed, split up, or avoided. The loss was not just the charge. It was the mental burden added to the deposit, the mundane, reliable, boring rest of people's money.

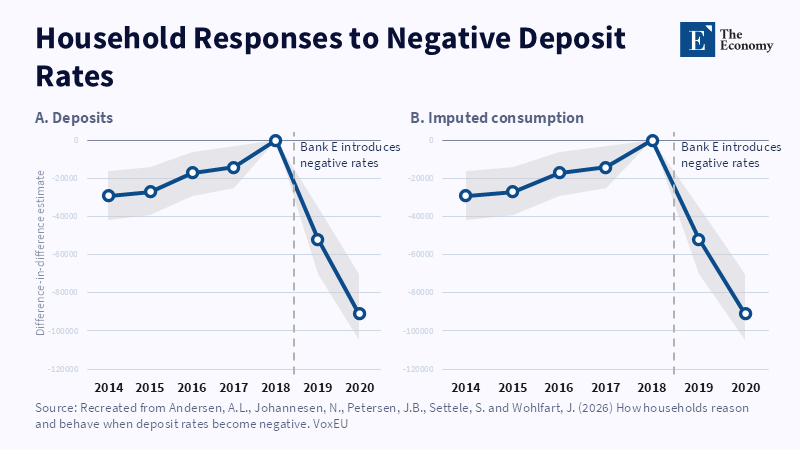

The response was large. Exposed households reduced deposit balances by about DKK 90,000, about USD 13,700, from a pre-stimulus level of about DKK 1.1 million, about USD 168,000. About one-third of this outflow was to assets other than deposits, such as stocks and pension accounts. Much of the remainder seems to have funded consumption. Estimated annual consumption increased by about DKK 40,000 for the exposed group. At the macroeconomic level, this would translate into a 0.5 percent to 1 percent increase in private consumption in 2020. That is the strongest case there is for this policy. Negative deposit rates did not just sit on banks' balance sheets. They moved money from deposit accounts into the economy.

Yet this success carries a warning. No stark upsurge in cash withdrawals means the classic story about cheap deposits being put under the mattress did not prove a dominant Danish pattern. The stronger pattern was discontent. According to survey evidence, people seemed to take the value further below zero more than above. Their explanations ranged from loss aversion and irritation with banks to perceived unfairness and better returns on other assets. Those were not inconsequential. They comprised what was transmitted to the household: in effect, the negative deposit policy partly worked because it was resented. Policies that banked on annoyance at banks are not run-of-the-mill rate reductions. They are stress tests of bank relationships.

Denmark's own monetary framework was important too. The krone was closely linked to the euro through the ERM II, making a clean escape by currency less attractive to Danish households. The transition to the euro did not mean a very different monetary context. As such, exits were mainly domestic: on spending, pensions, funds and bank balance splitting. This is important for policymaking. Negative deposit rates do not have exactly the same effect in every environment. Currency regime, financial culture, pension design and the structure of household balance sheets all matter in shaping the effect. In Denmark, the effect was to transfer money, but also to show something of the vulnerability of the deposit once the rate turns negative.

Japan Shows the Last-Resort Bank Account

Japan provides a different perspective. The Bank of Japan operated a negative interest rate policy from 2016 until March 2024. A typical household almost never faced directly negative rates on bank deposits in the Danish style. The squeeze was slower and more familiar. The rate offered on ordinary deposits languished near zero for many years. In 2023, it hovered at about 0.001%. Even when the policy shifted, ordinary deposit rates remained well below inflation. As consumer prices rose, the real return that cash deposits provided was negative. The account was safe in name only. It was not really safe in terms of households’ purchasing power.

This long period shaped household behavior. Japanese households held an enormous proportion of their wealth in cash and deposits. Cash and deposits amounted to just over 50.7% of households' financial assets at the end of fiscal 2024; stocks and other equities, 12.5%; investment trusts, 6.1%. This is often called conservatism. This is only half the story. The more accurate interpretation is that trust and return parted company. Households trusted banks to be repositories, not sources of growth. The bank was a vault, not a wealth machine. This is a poor basis for financial deepening. It protects savers from some risks, exposes them to inflation losses and leaves banks with just shallow and defensive loyalty.

The second Japanese answer was the search for yield offshore. Mrs. Watanabe is an imperfect expression, but it does reflect a real trend: ordinary Japanese retail investors searching for yields outside of their home country, outside of domestic deposits and bonds. Retail FX margin trading in Japan hit record levels in 2022, with notional volume topping JPY 10 quadrillion or roughly USD 62 trillion at recent exchange rates. This was not merely a small portfolio decision. It reflected how far domestic yields could drive Japanese households into the global currency risk space. The yen carry trade monetized the Japanese low-rate environment for the benefit of the world. It delivered risk from the banks to the households. That is not the same as creating a responsible investing culture.

Another difference between Japan and Denmark is the freedom for the yen to fluctuate. It becomes more attractive and riskier to invest abroad. A Danish saver switching from kroner to euros remains mostly in the same monetary world. A Japanese saver switching into dollar or Australian dollar investments or seeking higher returns takes real foreign-exchange risk. This risk can pay off when the yen falls but punish savers when it rises. That is the hidden risk of negative deposit rates and nearly-zero real-yield investments. Some households get more fearful and hoard more cash. Other households take more risks, expecting banks to support safe deposits with higher-yielding products. Both trends reach into the monetary middle ground where stable household savings bankroll uncertain productive credit in banks.

The Policy Lesson Is to Protect Trust, Not Punish Saving

The best argument is that negative deposit rates can work. Denmark shows that they can. Deposits fell; some money shifted to assets; and consumption increased. In a weak economy, those effects do count. Central banks may not be able to disregard demand just because they irritate savers and punish lenders. That defense is insufficient. It demonstrates only that negative deposit rates can shift money. It fails to demonstrate that they improve the banks themselves. A policy can be a one-off success and still erode the confidence banks need in the next downturn. The right test is not solely whether deposits decline, but whether the money is channeled into sound uses and whether households still regard banks as reliable intermediaries.

Initially, policy should safeguard basic liquidity. Transaction and emergency balances should have no negative nominal rate. Households require liquid, insured money for rent, taxes, illness, job loss and retirement. Larger balances will get market signals, but thresholds must be explicit, persistent and above normal life events to avoid discouragement. This is not a soft approach. It is a good system design. It protects the core of payments while introducing scope for incentives at the margin. It also sends the message that prudence is not being punished.

They also require more than the road of pain from depositors. A period of low rates should be the time to excel at advice, product design and provision. The saver needs straightforward, realistic information on real returns, inflation erosion and risk. The saver needs simple channels from idle balances into broadly diversified, low-cost instruments. Where there are risks of leverage or currency risk, they need to be clearly indicated. Moving a sum from a deposit into a pension fund is not similar to moving it into a foreign exchange account providing leverage. Both are about shifting portfolios in the broad national accounts view – but the risks for households are very different.

Negative deposit rates must therefore be kept as a ring-fenced emergency measure, rather than an ordinary supplement to monetary policy. They should be used with appropriate safeguards: protecting household liquidity, transparent limits, easy channels to safe assets and constant tracking of deposit flight destinations. Deposit flight is not always a sign of healthy risk appetite. It can mean extraction of spending power, foreign asset flight, balance splitting, or speculation. The experience of Denmark and Japan confirms the same principle: once banks no longer seem like the safe, natural home for safe money, the financial system loses more than deposits. It loses trust. The issue is not simply who has the incentive to deposit in a negative-rate environment, but how long banking can perform efficiently once depositors everywhere start asking why.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Abadi, J., Brunnermeier, M. and Koby, Y. (2023) ‘The reversal interest rate’, American Economic Review, 113(8), pp. 2084–2120.

Abildgren, K. and Kuchler, A. (2023) ‘Firm behaviour under negative deposit rates’, European Economic Review, 151, 104349.

Altavilla, C., Burlon, L., Giannetti, M. and Holton, S. (2022) ‘Is there a zero lower bound? The effects of negative policy rates on banks and firms’, Journal of Financial Economics, 144(3), pp. 885–907.

Andersen, A.L., Johannesen, N., Petersen, J.B., Settele, S. and Wohlfart, J. (2026) ‘How households reason and behave when deposit rates become negative’, VoxEU, Centre for Economic Policy Research, 7 July.

Andersen, A.L., Johannesen, N., Petersen, J.B., Settele, S. and Wohlfart, J. (2026) ‘Household behavior below the zero lower bound’, CEPR Working Paper No. 21623.

Bank of Japan (2024) ‘Changes in the monetary policy framework’, Monetary Policy Release, 19 March.

Chandak, V. (2023) ‘Mrs.Watanabe: How ordinary Japanese housewives shook the world of finance’, Medium, 17 October.

Danmarks Nationalbank (2021) ‘The response of household customers to negative deposit rates’, Danmarks Nationalbank Analysis, No. 9.

Eggertsson, G.B., Juelsrud, R.E., Summers, L.H. and Wold, E.G. (2024) ‘Negative nominal interest rates and the bank lending channel’, Review of Economic Studies, 91(4), pp. 2201–2275.

Felici, M., Kenny, G. and Friz, R. (2023) ‘Consumer savings behaviour at low and negative interest rates’, European Economic Review, 157, 104503.

Haaland, I., Roth, C., Stantcheva, S. and Wohlfart, J. (2025) ‘Understanding economic behavior using open-ended survey data’, Journal of Economic Literature, 63(4), pp. 1244–1280.

Holm, M.B., Paul, P. and Tischbirek, A. (2021) ‘The transmission of monetary policy under the microscope’, Journal of Political Economy, 129(10), pp. 2861–2904.

Japan Securities Dealers Association (2025) Annual Report 2025. Tokyo: Japan Securities Dealers Association.

Jensen, T.L. and Johannesen, N. (2017) ‘The consumption effects of the 2007–2008 financial crisis: Evidence from households in Denmark’, American Economic Review, 107(11), pp. 3386–3414.

Krogstrup, S., Kuchler, A. and Spange, M. (2020) ‘Negative interest rates: The Danish experience’, VoxEU, Centre for Economic Policy Research, 2 October.

Lilley, A. and Rogoff, K. (2020) ‘Negative interest rate policy in the post COVID-19 world’, VoxEU, Centre for Economic Policy Research, 17 April.

Matsuda, N., Oyama, J., Yamaoka, R. and Bessho, H. (2023) ‘Retail foreign exchange margin trading in Japan: An analysis from the developments in 2022’, Bank of Japan Review, 23-E-7.

Rogoff, K. (2017) ‘Dealing with monetary paralysis at the zero bound’, Journal of Economic Perspectives, 31(3), pp. 47–66.

Statistics Bureau of Japan (2026) ‘Consumer Price Index, 2025’. Ministry of Internal Affairs and Communications, 23 January.

Ulate, M. (2021) ‘Going negative at the zero lower bound: The effects of negative nominal interest rates’, American Economic Review, 111(1), pp. 1–40.

Wikipedia contributors (2026) ‘Mrs. Watanabe’, Wikipedia, The Free Encyclopedia, revised 12 February.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.