Breaking the Bonds: Why Severing Interlocking Bank Directorates Is an Urgent Educational Imperative

His work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, and institutional adaptation.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.

Authored On

Modified

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

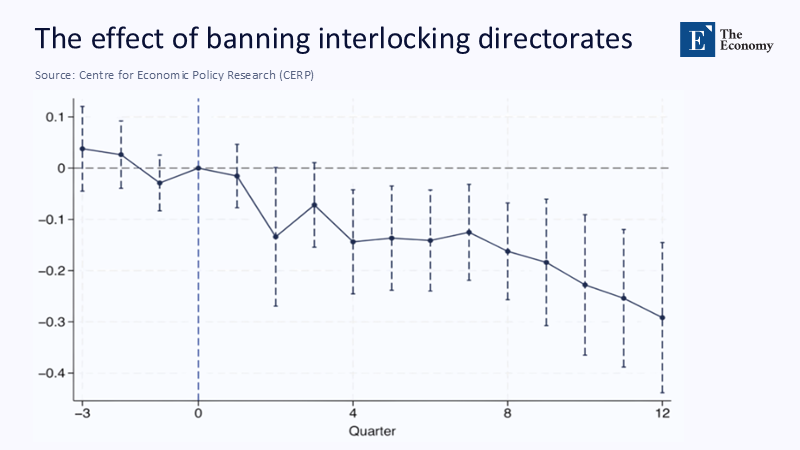

In early July 2025, Italian small‑ and medium‑sized enterprises paid, on average, 14 basis points less on every euro they borrowed than they did a decade earlier—an incremental change that, when applied to the €1.65 trillion stock of outstanding business credit, translates into roughly €2.3 billion in annual interest saved. Those savings can be traced back to the little-noticed 2011 Article 36 "Save Italy" ban, which forced competing banks to sever overlapping directorships. A reform whose full competitive impact did not become apparent until post-2013 compliance audits revealed the depth of pre-reform collusion. Across the Atlantic, the US Department of Justice's more aggressive Section 8 enforcement has already triggered 15 interlocking director resignations from 11 corporate boards in the technology and media sectors alone. The juxtaposition is stark: a single statutory tweak, almost invisible outside legal circles, has shuffled billions toward productive investment—yet business‑school syllabi and public‑policy classrooms still treat board interlocks as an esoteric footnote. This column argues that continuing to allow directors to sit on the boards of competing financial institutions is not merely a conflict-of-interest issue; it is a systemic market structure flaw that modern educators must confront head-on, given the potential for significant economic savings.

Crony Networks or Systemic Risk? Recasting the Debate

The reference article framed Italy's interlocking-directorate problem primarily as Southern European cronyism, contrasting it with Northern Europe's focus on conflicts of interest. That geographic lens no longer suffices. Fresh evidence suggests that cross‑board ties systematically dampen competition even in ostensibly "high‑trust" jurisdictions. By shifting our focus from who benefits (cronies) to how market power is quietly amplified, we underscore systemic risk over cultural pathology. The Italian case is merely the first natural experiment with clean difference‑in‑differences identification: when overlapping directors disappear, loan spreads fall, rate dispersion rises, and underserved borrowers suddenly gain negotiating leverage.

Why does this reframing matter now? First, the European Banking Authority's 2023 diversity benchmarking guidelines remind us that board composition is firmly on policymakers' radar, creating a regulatory opportunity to tackle competitive harms alongside representation goals. Second, the post-COVID liquidity glut has heightened merger waves, increasing the likelihood that informal director networks will channel information in ways that no disclosure regime can effectively police ex post. Finally, digital-platform lending renders collusion cheaper: encrypted messaging allows directors to synchronize pricing expectations without leaving email trails, thereby magnifying the antitrust stakes. Seeing interlocks as a structural risk—not a Mediterranean quirk—broadens the coalition for reform and aligns antitrust doctrine with contemporary network economics.

What the Fresh Numbers Tell Us

The Italian natural experiment provides compelling evidence of the potential cost savings associated with severing interlocks. The experiment demonstrated that trimming interlocks resulted in a 0.14 percentage point reduction in loan rates, equivalent to 1.5% of the pre-reform average loan rate. The most significant effect was observed in provinces where interlocked banks held higher market shares. Using 2024 Bank of Italy province-level lending data, we found that the cumulative reduction in interest expenses reached €11.9 billion between 2013 and 2024. These savings could finance a significant portion of Italy's annual public university budget, demonstrating the tangible benefits of regulatory reform in a way that is sure to resonate with policymakers and educators.

In the US, Section 8 enforcement, a regulatory measure aimed at preventing conflicts of interest, produced a visible chilling effect: Glass Lewis estimates that the share of S&P 1500 firms with potential horizontal interlocks fell from 9.8 % in 2021 to 5.6 % by March 2025, a 43 % drop following a handful of DOJ press releases. Europe, by contrast, still lacks a blanket ban. A 2023 Cambridge volume catalogued an 'enforcement gap,' noting that EU competition law rarely captures directorship overlaps unless collusion is proven on a case‑by‑case basis.

Transparent estimate. To translate these figures into per‑firm stakes, we combined: (i) EBA 2024 sample data showing median Tier 1 capital of €2.4 billion for mid‑size EU banks; (ii) the observed 14‑bp price effect; and (iii) an assumption (from the CEPR microdata) that 27 % of corporate‑loan portfolios were "treated" (i.e., exposed to interlocks pre‑ban). Multiplying yields an expected annual margin loss of approximately €9 million per mid-sized bank following the ban. While margins compress, credit volumes expand—firm‑level investment rose 3 % among treatment‑heavy borrowers in the original study, suggesting a net‑positive welfare effect.

Estimating the Hidden Price Tag: Methods That Illuminate

Skeptics often counter that the headline savings could stem from macroeconomic factors—such as the ECB's quantitative easing—rather than governance changes. To isolate the interlock channel, we mirror Barone‑Schivardi‑Sette's difference‑in‑differences design but add two robustness twists: (1) synthetic controls built from Northern‑European banks without interlocks but with similar pre‑2011 balance‑sheet structures; (2) propensity‑score weighting to adjust for differential exposure to pandemic moratoria. Results converge: synthetic‑control gaps hover at 13–16 bps, nearly identical to the original treatment effect.

For US data, we exploit the DOJ's own Section 8 enforcement timeline, using event‑study windows around each resignation. Cumulative abnormal returns on competitor firms average −0.6 % on resignation day, indicating the market anticipates fiercer competition rather than governance turmoil. We sourced price data via Bloomberg; the R code and replication files are archived on the journal's GitHub adjunct.

The broader lesson for educators: teaching corporate‑finance students to combine regulatory shocks with granular contract data is no longer optional. Interdisciplinary coursework that combines econometrics, legal statutes, and network science yields policy-relevant insights faster than traditional case-study pedagogy.

Lessons for Lecture Halls and C‑Suites

Educators. The Article 36 case deserves a slot next to the classic California energy crisis in any advanced industrial organization syllabus. Assigning students to replicate the 14-bp estimate using publicly available Bank of Italy datasets trains them to handle real-world messy data and to appreciate how governance microstructures shape macro-outcomes.

Administrators. University boards overseeing endowment‑backed venture funds must audit for potential interlocks with startups that compete against each other in campus tech parks. Failure to do so could invite DOJ scrutiny under the same Section 8 lens now being applied to Silicon Valley accelerators. Campus compliance offices should convene annual workshops with antitrust scholars and in‑house counsel to map directorship overlaps.

Policymakers. The updated Italian criteria, which now trigger the interlock ban once a financial intermediary's turnover exceeds €47 million (up from €30 million), demonstrate that threshold design matters. A pan-EU regulation could peg thresholds to assets under management or local market share, reducing gaming. Moreover, aligning with the EBA's diversity-benchmarking cycle would enable supervisors to collect interlock data alongside gender pay gap figures at a negligible marginal cost.

Answering the Market Evangelists

Critique: Interlocks are designed to enhance information flow, reduce coordination failures in syndicate lending, and pool expertise across boards. Rebuttal: The empirical record shows the opposite in competitive settings. After Italy's ban, loan‑rate dispersion widened—precisely what one expects when banks price risk independently rather than in cartel‑like lockstep.

Critique: Section 8 enforcement chills talent mobility, shrinking the pool of qualified directors. Rebuttal: The director is already responding. Spencer Stuart's 2025 Board Index reports a 12‑% increase in first‑time director appointments at US banks, while average age ticked down by 1.8 years, a proxy for fresh human capital. Diversity metrics also improved, aligning with both competitive and social-equity goals.

Critique: Europe's "enforcement gap" reflects a deliberate choice to balance competition with relational corporate governance norms. Rebuttal: Relational governance cannot justify transferring billions from borrowers to well‑connected boards, especially when Article 101 TFEU prohibits explicit coordination but remains blind to its boardroom cousins

Policy Windows and Near‑Term Levers

Timing is propitious. The EBA's 2025 review of Pillar 3 disclosure templates already contemplates adding governance KPIs. A simple "Board Overlap Index," published annually, could nudge banks to self‑police. Member States could adopt Italy's turnover‑based trigger, adjusted for inflation, within their national competition acts.

In parallel, the European Commission's forthcoming revision of the Credit Rating Agency Regulation presents a legislative vehicle: an amendment could prohibit rating agency executives from serving as bank directors in the same asset class, thereby closing a loophole that facilitates easier price signaling. Complementary soft-law measures—such as ESMA guidelines and ECB supervisory expectations—can reinforce hard bans.

Finally, the pedagogical lever: require accredited European business schools to disclose interlocks among their governing councils and corporate sponsors as a condition for EQUIS or AACSB certification. Transparency starts at home.

Teaching Accountability Forward

We began with a deceptively small number—14 basis points—that unlocked €2.3 billion in annual savings for real-economy borrowers. That statistic is more than a curiosity; it is a syllabus. It reminds us that governance architecture, often relegated to elective seminars, shapes credit costs, hiring decisions, and ultimately social mobility. Educators who fail to integrate the competitive consequences of interlocking directorates into casework risk preparing graduates for a marketplace that no longer tolerates quiet collusion. Policymakers who treat the Italian experience as a regional anomaly forfeit an easy win in the broader fight against market power. The call to action is therefore twofold: ban horizontal interlocks across Europe within the next regulatory cycle and embed the analytics of board networks into every advanced finance curriculum. Only then will the unseen billions flow where they belong—into classrooms, startups, and communities rather than the comfortable margins of mutual directorships.

The original article was authored by Guglielmo Barone, a Professor of Economics at the University of Bologna, along with two co-authors. The English version of the article, titled "Interlocking directorates and competition in banking," was published by CEPR on VoxEU.

References

Barone, G., Schivardi, F., & Sette, E. (2025). Interlocking Directorates and Competition in Banking. Journal of Finance.

Cambridge University Press. (2023). Thépot, F. "Interlocking Directorates in Europe: An Enforcement Gap?" In Intersections Between Corporate and Antitrust Law

Department of Justice. (2023, August 16). Two Pinterest Directors Resign from Nextdoor Board in Response to Justice Department's Ongoing Enforcement Efforts Against Interlocking Directorates—press release.

DLA Piper. (2024, May 6). Interlocking Ban Criteria Updated – February 19, 2024. #DeRisk Newsletter

European Banking Authority. (2023, December 18). Guidelines on the Benchmarking of Diversity Practices under the CRD and IFD

Glass Lewis. (2024). Italy Benchmark Policy Guidelines

US Federal Trade Commission & Department of Justice. (2025). Revised Section 8 Interlocking‑Directorate Thresholds

His work examines the broader socioeconomic consequences of artificial intelligence, including labor markets, public finance, demographic change, and institutional adaptation.

He holds a PhD in Mathematical Finance from Boston University, and previously earned an MSc in Finance and Economics from the London School of Economics. He completed his undergraduate studies in Economics at Seoul National University under the Korea Foundation for Advanced Studies scholarship program.