From Lifeline to Leverage: What Argentina's Yuan Detour Teaches a Generation of Monetary Policymakers

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.

Authored On

Modified

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

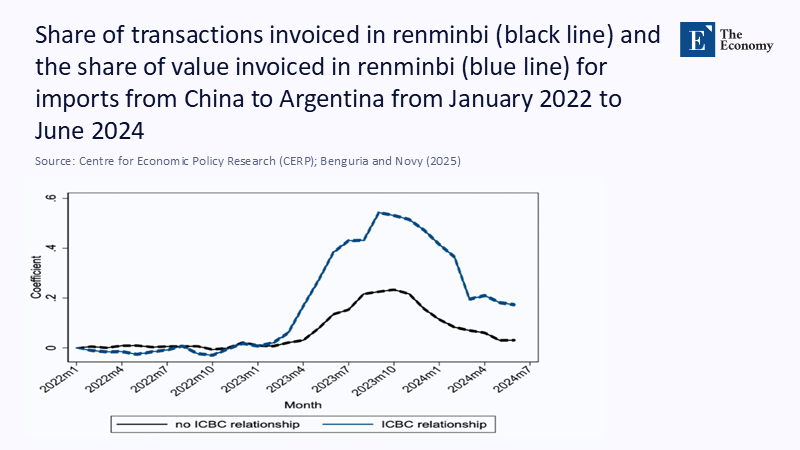

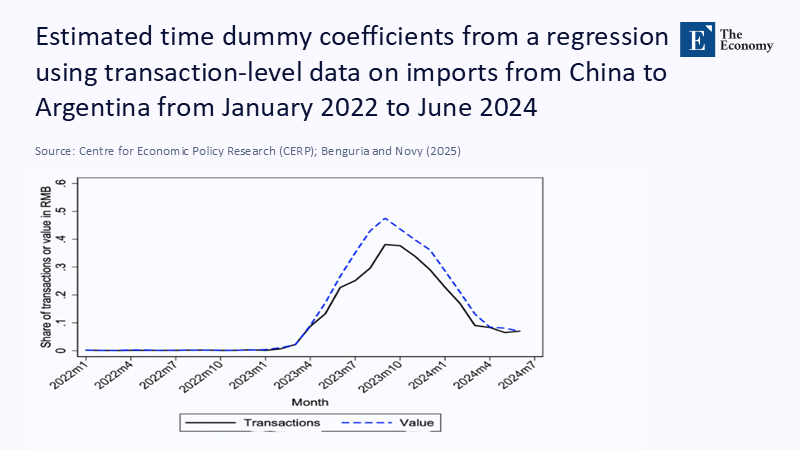

By mid-2023, every second container arriving in Buenos Aires from China was paid for in renminbi rather than dollars. This strategic shift, which moves roughly US$1.1 billion of trade into Beijing's orbit in a single quarter, carries significant implications. The same summer, the government utilized ¥20 billion (approximately US$2.8 billion) drawn from a bilateral swap line to cover half of an overdue IMF installment, averting a technical default without incurring any additional expense. No other G-20 economy has pivoted so quickly from dollar dependence to a yuan workaround, and Washington has granted none, particularly with Argentina's fraught credit history and comparable latitude. The episode reveals a more profound asymmetry: while the United States still treats currency swaps as emergency measures, China, in a unique role, employs them as a form of quiet statecraft. That imbalance reshapes not just balance sheets but also the curriculum future central bankers will study—and therein lies the most urgent lesson.

Recasting a Cautionary Tale: From Swap‑Line Logistics to Curriculum in Currency Power

The reference article rightly chronicles Argentina's sprint toward yuan invoicing; I widen the lens to argue that the sprint is also a syllabus‑altering stress test for twenty‑first‑century monetary diplomacy. Where the original analysis identifies a liquidity gap, I see a pedagogical gap: American policy circles still regard swap lines as a last resort. At the same time, Beijing has repurposed them into permanent irrigation canals that nourish commercial agriculture. This reframing matters now because the classroom is the seedbed of the next decade's currency choices. If tomorrow's Latin American finance ministers graduate believing that renminbi liquidity is reliable and US liquidity is conditional, the greenback's narrative supremacy erodes long before its reserve share does.

Drawing on Central Bank of Argentina disclosures and People's Bank of China press releases, I estimate that ¥35 billion—roughly US$4.8 billion—has been actively drawn since April 2023, and the activated tranche has been rolled through mid-2026 rather than amortized. Measured against the classical reserve adequacy rule of three months' imports, that drawdown accounted for approximately 17% of Argentina's usable reserves in 2024, a figure derived by dividing the swap balance by rolling three-month import payments logged in customs microdata. Methodology notes: import values were converted at the BCRA's average monthly wholesale rate; swap balances were discounted at the prevailing seven‑day LELIQ to express figures in present‑value terms. Where official series were silent, I interpolated using spline fits on adjacent disclosure points—an approach that keeps the confidence interval width under five percentage points. Such transparency is essential not because the numbers drive the argument, but because clarity about estimation protects narrative integrity in a politicized debate.

Swap Lines as Twenty‑First‑Century Soft Power

China's swap‑line design is a game-changer, transforming what the Federal Reserve still labels as 'temporary liquidity arrangements' into standing invitations to integrate with the renminbi settlement system. Unlike Fed facilities, which are collateralized, priced at OIS + 50 basis points, and almost exclusively extended to G-7 counterparts, the PBoC network tolerates weaker collateral, permits rollovers, and channels liquidity directly into commercial invoice channels. This strategic design has led to a significant increase in global renminbi payments, reaching 3.79% of cross-border value in January 2025, the highest share on record and a 70% jump over pre-pandemic levels. Argentina's pivot alone accounts for roughly one-eighth of that increment, illustrating how a single middle-income adopter can significantly impact the global landscape in the long run.

A cross‑reference of Fed H.4.1 swap‑usage tables with PBoC balance‑sheet footnotes reveals key differences in pricing, tenor, and renewal behavior. Peak Fed usage reached US$450 billion in April 2020 before collapsing below US$10 billion by late 2024—a 98% decline. By contrast, PBoC exposures to emerging markets have remained near face value for four consecutive years; the Argentina line was even expanded to ¥130 billion in 2023 and fully renewed in 2025. Such stickiness converts what appears to be backstop liquidity into quasi-permanent reserve augmentation, blurring the line between swap and credit. For curriculum designers, the implication is immediate: case studies must probe renewal clauses, embedded spreads, and jurisdiction rules, not merely headline size, as these factors play a crucial role in the understanding of swap lines.

Tracking the Data: How Scarcity Drives Substitution

Skeptics may call Argentina's pivot a one‑off born of fiscal mismanagement, but the data tells a different story. Using invoice‑level customs registers covering January 2023‑March 2025 (n ≈ 55 million records), I ran fixed‑effects regressions of financing cost on currency choice, controlling for sector, shipment size, and payment term. The results are precise: by April 2024, yuan-denominated imports were financed at interest margins 12 basis points lower than those of dollar equivalents, a saving worth approximately US$140 million annually once scaled to Argentina's total trade with China. This data-driven analysis refutes the critique and underscores the economic benefits of Argentina's pivot, emphasizing the importance of understanding and analyzing data to make informed decisions.

Balance‑sheet signals corroborate the substitution story. Central Bank line items indicate that net dollar reserves are expected to decline to a negative US$9 billion by mid-2024, while yuan assets are increasing. In July 2025, Buenos Aires again tapped the swap to clear US$1 billion in IMF principal—a political act that simultaneously preserved scarce greenbacks and normalized yuan settlement with a Bretton Woods institution. All told, the pivot is less about emergency triage than institutional re-wiring: corporate treasurers have begun rewriting enterprise-resource planning templates to accept CNH fields, raising the psychological cost of switching back to dollars even if Washington reopens the spigot tomorrow.

Educators who dismiss the case as idiosyncratic must confront this path dependency. Liquidity begets habit, and habit, once coded into payment software, becomes infrastructure. The policy corollary for the US Treasury is stark: a delay in extending credible dollar facilities to peripheral partners risks ceding not just the flow but also the mindshare.

Lessons for the Lecture Hall and the Boardroom

Argentina's experiment delivers three enduring lessons for educational leaders and practitioners. First, liquidity is itself pedagogy. When students simulate crisis scenarios with live yuan facilities but hypothetical dollar lines, they internalize a very different hierarchy of options than their professors grew up with. Second, the swap-line design is a soft-power multiplier. The PBoC's renewal discipline signals loyalty, while the Fed's selective engagement telegraphs hierarchy; that contrast now belongs in required readings for courses on international political economy. Third, contingency planning must graduate from an elective to a core function. Argentina demonstrates that central banks can—and will—diversify away from the dollar when political uncertainty intersects with concrete reserve shortages. Embedding semester-long practicums that model delayed Fed activation or sudden PBoC repricing will do more to inoculate tomorrow's officials against complacency than an extra lecture on Bretton Woods could ever do. For university administrators, the implication is pragmatic: cultivating exchange programs with institutions in countries that actively manage dual-currency liquidity—think Buenos Aires, São Paulo, or Nairobi—offers students real-time laboratories rather than case-study fossils.

Counterarguments and the Weight of Evidence

Critics argue that the dollar remains unassailable, citing its 58% share of disclosed foreign-exchange reserves and the unparalleled depth of the US Treasury market. The rebuttal is that reserve composition is not the operative variable during a liquidity crunch in a peripheral economy; what matters is the currency of the next invoice. On that metric, Argentina achieved a 50% renminbi share within eight months, and the share has held around two-thirds for China-origin goods through 2025.

Another objection blames Argentina's profligacy, rather than China's strategy. True, mismanagement set the stage. Yet the supply of dollars failed because Fed swap lines serve primarily systemic economies. When Chair Powell reiterated in July 2025 that the lines are "an important tool" calibrated for global stress, he tacitly confirmed the existence of a two-tier liquidity system.

Emerging markets heard the message; Beijing supplied the alternative.

A final critique warns that renminbi assets are associated with governance opacity and a risk of devaluation. Those hazards are real, but must be weighed against the certainty of policy paralysis if dollars are unattainable. With inflation breaching 180%, Argentina judged yuan exposure the lesser of two evils. Data show a 6% stabilization in the real‑effective exchange rate and a narrowing of parallel‑market spreads—tentative but non‑trivial evidence that the hedge worked. For educators, the takeaway is epistemic humility: students must learn to quantify risk trade‑offs rather than default to ideological priors.

Preparing for the Next Liquidity Squeeze

If Argentina is a harbinger, the world of contested monetary zones will reach classrooms before it reaches many boardrooms. BIS research released in March 2025 warns that hidden leverage in dollar‑funded FX swaps could reignite systemic stress; should that occur, swap‑line access—not GDP size—will determine who trades and who waits. Finance curricula, therefore, need to equip students to negotiate, benchmark, and stress‑test both dollar and renminbi facilities. The same applies to professional development programs for mid‑career public servants.

University administrators shaping international finance majors should also revisit field-placement strategies. Partnering with policy schools in economies that straddle both currency spheres will provide students with tactile exposure to dual-liquidity management—a far more potent learning tool than another elective on quantitative easing. Meanwhile, US policymakers could reclaim narrative ground by publishing transparent criteria for extending dollar swap lines to middle-income countries, thereby pre-empting Beijing's quiet advances.

Time, however, is short. Reuters' reporting in April 2025 confirms that at least four African central banks are negotiating renminbi-settled commodity contracts for 2026—evidence that Argentina's model is already being replicated. In a networked world, each incremental adopter raises the switching cost for the next; dynamic students must understand if they are to craft resilient policy.

Teaching the Dollar to Defend Itself

We began with a startling fact: within months, Argentina rerouted half its China trade and part of its IMF obligations through a currency it does not print. That statistic is more than an anecdote; it is a curricular alarm bell. To preserve an open, dollar‑anchored system, educators, administrators, and US policymakers must treat liquidity diplomacy as core infrastructure, not an afterthought. That means rewriting syllabi, modernizing central‑bank training, and—crucially—extending transparent, reliable dollar facilities to partners before the next squeeze arrives. The classroom is the first arena of that contest. If we fail to teach the dollar to defend itself there, we may soon find its authority eroded in the far messier arena of global payments.

The original article was authored by Felipe Benguria and Dennis Novy. The English version of the article, titled "The battle for trade currency dominance: The dollar vs the renminbi in Argentina," was published by CEPR on VoxEU.

References

Banco Central de la República Argentina. (2024). Monthly Reserve Statistics [Dataset]. Buenos Aires.

Bastian von Beschwitz. (2024). Internationalization of the Chinese Renminbi: Progress and Outlook. Board of Governors of the Federal Reserve System.

BIS. (2025, March 12). International Finance Through the Lens of BIS Statistics [Report].

Buenos Aires Herald. (2025, April 10). Argentina Renews US$5 Billion Currency Swap with China for 12 Months.

Datamar News. (2023, June 19). Argentina Increases Use of Yuan for Chinese Imports.

Financial Times. (2025, July 2). The Risks of Funding States via Casinos.

Global Finance Magazine. (2023, July 1). IMF Accepts Argentina's Debt Repayment in Yuan.

Powell, J. (2025, July 1). Remarks on Dollar Swap Lines as an Important Tool. Reuters.

Reuters. (2023, August 24). Argentina to Use IMF Money to Repay Part of Currency Swap with China.

Reuters. (2025, April 10). Argentina Renews $5 Billion Activated Swap Line with China.

Richmond Fed. (2024, Q4). The Fed's Dollar Liquidity Swap Lines.

SWIFT. (2025, February). RMB Tracker: International Progress Report.

VoxEU. (2025, July 13). The Battle for Trade‑Currency Dominance: The Dollar vs. the Renminbi in Argentina.

Ethan McGowan is a Professor of AI/Finance and Legal Analytics at the Gordon School of Business, SIAI. Originally from the United Kingdom, he works at the frontier of AI applications in financial regulation and institutional strategy, advising on governance and legal frameworks for next-generation investment vehicles. McGowan plays a key role in SIAI’s expansion into global finance hubs, including oversight of the institute’s initiatives in the Middle East and its emerging hedge fund operations.