Foreign Exchange Reserve Quality: Why the Source Matters

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Reserve quality matters more than headline size Borrowed reserves can hide future repayment risks Governments should disclose how reserves are financed

The household comparison makes the logic airtight. A salaried worker saving part of each month’s income is both accumulating cash and increasing net wealth. A second individual can simultaneously put exactly the same amount into a bank account by borrowing against an inherited property. Thus, the two individuals may report the same cash balance. Only the first individual has increased his or her net wealth. Meanwhile, the second individual might still be acting as a rational borrower. The loan can cover a temporary income loss or prevent a forced asset sale. Still, the increase in cash should be recognized as savings only alongside the debt, interest rate and date of repayment. It should also be recognized when looking at central banks’ balance sheets.

A reserve increase of up to 1 percent of GDP may look reassuring on a central bank balance sheet. Nevertheless, its significance alters markedly depending on its source. A study covering 44 emerging countries associated privately financed reserve increases with sovereign spreads about 1.35 percent lower. Public borrowing showed little reliable benefit. That gap should change how reserve buffers are judged. A country can earn foreign currency through exports, services, remittances or receive durable private investment. Its buffers and net position rise both in tandem. Alternatively, a country can raise the same headline number through external borrowing. It receives cash, but it also creates a further claim against that cash. The two reserve stocks may look alike in a table, but they differ in risk. The quality of foreign-exchange reserves, not their aggregate size, must then form the core test for resilience. Without that distinction, governments can declare borrowed resources as aggregate national savings. Investors may then reward a buffer likely to disappear when needed most

Foreign Exchange Reserve Quality Is the Missing Metric

Reserve policy is still framed mainly as a question of adequacy. Analysts compare reserves against imports, short-term foreign debt, the size of broad money, or the threat of a large, sudden flow of capital. Those measures are still relevant. They identify whether an economy has enough liquid foreign assets to cope. But they overlook how reserve buffers have been created. That oversight is significant because a gross asset may increase without a net transfer of foreign savings to the public sector. External borrowing puts dollars on the asset side and creates a matching foreign-currency liability. The central bank gains foreign exchange, but the public sector may not become safer.

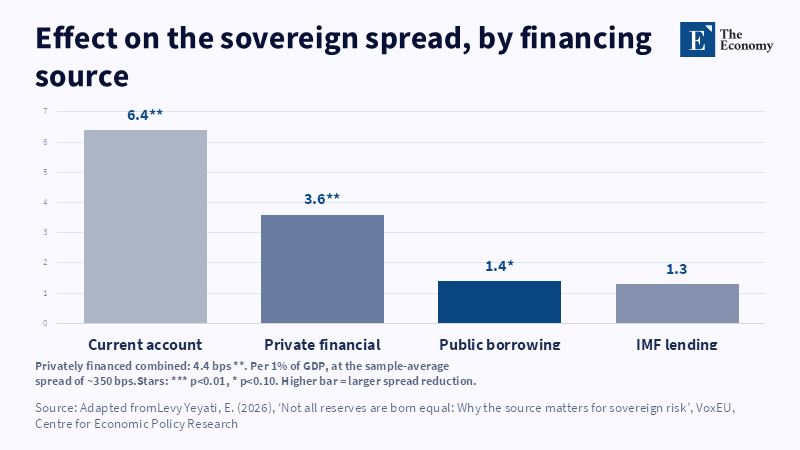

Reserves that have accumulated in the course of a current account surplus are different in ways that matter. So too are reserves acquired from durable private inflows. Both strategies raise the ability to meet external claims without adding matching public debt. A source-based measure of reserve quality reveals what simple measures of adequacy overlook. They show whether the national buffer reflects income and capital formation or an increased burden of liabilities. The distinction has always been simple, but recent evidence gives it practical weight. A 2025 working paper examined around 7,000 monthly observations from 44 emerging countries between 2000 and 2024. It isolates reserve movements coming from private foreign-currency acquisition against reserve movements coming through public borrowing as well as official financing.

When the source is private acquisition of foreign currency, a 1% of GDP reserve increase was associated with lower sovereign spreads. The estimate was 4.4 basis points on an average spread of 350 basis points. Current-account-based reserve increase was associated with about 6.4 basis point tightening. Financial-account-based reserve increase was associated with about 3.6 basis point tightenings. Public borrowing was associated with a weaker, less significant effect. These are not purely causal estimates. The paper used lagged flows, country controls and global financial variables. It omitted the global financial crisis, 2020 and episodes in which spreads exceeded 1,000 basis points. Reverse causality could still be relevant. Nevertheless, this pattern is clear across spread and crisis tests. It also confirms some earlier peer-reviewed research. This pattern shifts the focus of reserve accumulation away from a race for larger headline figures and towards the underlying balance sheet.

How many months of imports can a country’s reserves cover? How much of that cover comes with future repayment. This is relevant nowadays because many emerging economies have entered this decade with already high debt-service ratios and constrained access to international financial markets. Total external debt stood at roughly US$8.9 trillion for low- and middle-income countries in 2024. In 2023, they paid a record US$1.4 trillion in external debt-service payments (including US$406 billion in debt interest). In such environments, accelerating the reserve ratio may just transfer the burden of refinancing from the government now to the government later. Gross liquidity can stabilize markets temporarily but will not eliminate the currency, maturity and rollover risks associated with the debt used to finance it.

Gross Liquidity Can Hide a Weak Balance Sheet

When reserve growth is financed through external bond sales, syndicated loans or central-bank swaps, the resulting increase in liquidity is not equivalent to inward replenishments from exports, tourists, migrants’ remittances, services, or more permanent investments. This does not imply that borrowed reserves are not useful. During a sudden stop, access to emergency liquidity can prevent a temporary crunch from becoming a crisis. Official provision of liquidity can also buy time for adjustment when private markets shut down. The error occurs in confusing bridge finance with long-term sustainability.

Borrowed reserves often arrive when risk is already rising. They can carry short maturities, high interest costs or strict conditions, or create false confidence in the headline reserve figure if near-term repayments rise in tandem. A buffer must be judged against the claims that can drain it. That is why reserve adequacy needs a source test, a maturity test and a net position test. The quality of foreign exchange reserves is high if the stock is liquid, unencumbered and supported by sustainable external income flows. It is low if it is supported by short-term debt, expensive refinancing, or transitory official support.

One could argue that dollars are fungible. Once a dollar is sitting at a central bank, any dollar could fund the intervention. One might come from an export, another from a bond. This is true at the time of payment. It is false across the life of the balance sheet. The borrowed dollar is associated with a future outflow. It can lead to a decline in confidence if investors anticipate repayment pressure, particularly when international rates increase or market access shrinks. The 2025 panel results show that this difference matters. Privately sourced reserve gains are associated with a 1.1 percentage point lower chance of crossing a 1,000-basis-point crisis threshold. Public flows were not statistically significant in the crisis model. The impact of private flows persisted across various alternative distress thresholds. This does not indicate that every private inflow is risk-free. Instead, it indicates that the liability structure supporting the stock of reserves affects the market's valuation of protection.

Kenya Shows Why Reserve Size Is Not Currency Policy

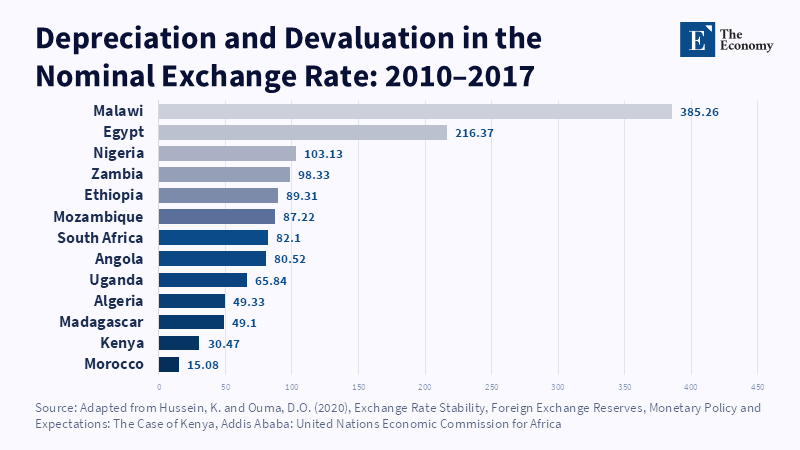

Kenya's lesson shows why a reserve stock cannot bear the entire burden of exchange-rate policy. A United Nations report used monthly data covering the period 2000–2017. It developed a model to analyze how measures of reserves, exchange rates, monetary policy and market expectations interact. It found no statistically significant effect of reserve levels on either the nominal or real exchange rate. Market expectations and speculation mattered more, as the current account, output and the nominal exchange rate determined long-run changes in reserve levels. This should not be interpreted as an indication that reserves do not matter, because countries still have a need for a liquid buffer in order to meet external obligations and prevent volatile movements in the market. Forex holdings are no replacement for fixing the underlying factors determining the demand for them.

The regional comparison in that study underlines the point. Between 20010 and 2017, the Kenyan shilling depreciated by approximately 30.47 percent, compared to sharp declines in numerous other African currencies. It took place despite the reserves buildup and active policy management. By 2016, Kenya held close to US$7.6 billion in reserves, modest relative to the stock held by Algeria or Libya, but not unimportant for Kenya. Its exchange rate still reflected trade imbalances, capital flows and future market consensus about inflation.

A central bank may use reserves in order to slow a decline, but it cannot sustain a price that is at odds with the external balance, nor can it generate export revenues through intervention alone. The quality of foreign exchange reserves improves when the state broadens the set of sustainable, ongoing sources of foreign currency; when it reduces import dependence and strengthens fiscal and monetary credibility. Then, the reserve account itself is an indication of resilience not its one and only obvious symbol.

Make Reserve Provenance a Policy Rule

The first reform is to demand more disclosure. Reserve reports could take a step toward transparency by putting out a bridge from opening to closing balances. This bridge could reveal gains in reserves from the current account and private capital, as well as identify sovereign borrowing, central-bank borrowing, official lending and valuation effects. It could even set gross reserves beside short-term public foreign-currency liabilities, scheduled debt payments and the net public foreign asset position. This would not necessitate a new economic theory; it would simply see the application of reasonable balance-sheet discipline to sovereigns and their holdings. According to the International Monetary Fund, reserves are most efficiently accumulated via sound fiscal and external posture: stable private inflows should be preferred to short-term foreign borrowing. A standard reporting template would provide the measure.

The second reform would shift the incentives facing governments and markets. Credit rating reviews, debt sustainability reports and parliamentary budget documents should show foreign exchange reserve quality and not just gross adequacy. A long-term, concessional loan should not be treated the same as a volatile commercial bond. Both raise reserves, but one carries different risks. Neither should be hidden. The first could provide cheap insurance and time to reform. The second could raise rollover risk even as it lifts the headline reserve stock. Market analysts could apply a simple adjustment. They could net near-term public foreign-currency liabilities against short-term foreign-currency debt. They could weigh out- and in-flows by implementation lag and maturity and net them against gross reserves. They could complement, not replace, existing adequacy ratios. Then what was genuinely self-financed would be clearer. Governments would be less prone to borrow just to boost a visible ratio.

The third reform is structural: reserve policy should be directly associated with export capacity, energy security, tax credibility and the quality of capital inflows. Excessive current-account surpluses are not always desirable: forcing them through weak domestic demand or an undervalued exchange rate can impose substantial economic costs but persistent foreign-currency inflows do count; so does the mix of finance. Foreign direct investment with an eventual link to productive assets is generally more persistent than very short-term portfolio debt. Remittances may be resilient, but should not mask a lack of employment or inward trading. Commodity windfalls can produce strong cushions, which a prudent fiscal rule would allow to be partly preserved or disappear through procyclical spending. The quality of FX reserves is one piece of a broader policy question: can the economy produce a foreign currency surplus through a permanent change in global prices, rates or confidence?

No step will eliminate unknowns. Source data will be re-checked. Private flows will be reversed. Export earnings may decline. Borrowed reserves may still put out fires. But the fault in today’s approach is one step bigger: it recognizes reserve dollars as equally claimable on tomorrow. They are not. The opening figure shows why that assumption fails. A reserve gain equal to 1 percent of GDP was linked to a lower likelihood of distress, but only when its financing improved, rather than merely enlarged, the sovereign’s balance sheet. The policy response is clear: central banks should disclose where reserves came from, finance ministries should report the liabilities created beside them and markets should assess buffers by net strength, maturity and source. Foreign exchange reserve quality should become a standard measure of resilience. Cash in hand matters during a shock, but the safest cash has no repayment date.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Aizenman, J. and Lee, J. (2007) ‘International reserves: Precautionary versus mercantilist views, theory and evidence’, Open Economies Review, 18(2), pp. 191–214.

Gómez, J.F., Levy Yeyati, E. and Temperley, P. (2025) The Source Matters: How Reserve Financing Affects Sovereign Credit Risk. RedNIE Working Paper No. 370. Córdoba: Red Nacional de Investigadores en Economía.

Gourinchas, P.-O. (2026) ‘Adequate reserves shield economies from shocks and strengthen resilience’, IMF Blog, 5 March.

Hussein, K. and Ouma, D.O. (2020) Exchange Rate Stability, Foreign Exchange Reserves, Monetary Policy and Expectations: The Case of Kenya. Addis Ababa: United Nations Economic Commission for Africa.

Levy Yeyati, E. (2026) ‘Not all reserves are born equal: Why the source matters for sovereign risk’, VoxEU, 14 June. London: Centre for Economic Policy Research.

Levy Yeyati, E. and Gómez, J.F. (2022) ‘Leaning-against-the-wind intervention and the “carry-trade” view of the cost of reserves’, Open Economies Review, 33(5), pp. 853–877.

Obstfeld, M., Shambaugh, J.C. and Taylor, A.M. (2010) ‘Financial stability, the trilemma, and international reserves’, American Economic Journal: Macroeconomics, 2(2), pp. 57–94.

Sosa-Padilla, C. and Sturzenegger, F. (2023) ‘Does it matter how central banks accumulate reserves? Evidence from sovereign spreads’, Journal of International Economics, 140, article 103711.

World Bank (2025) International Debt Report 2025. Washington, DC: World Bank.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.