Tariffs Outlive the Price Shock: Why Europe Must Look Beyond Short-Term Welfare

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

Small tariffs can permanently redirect trade Large retaliation can damage domestic supply chains Europe must protect capacity without protecting failure

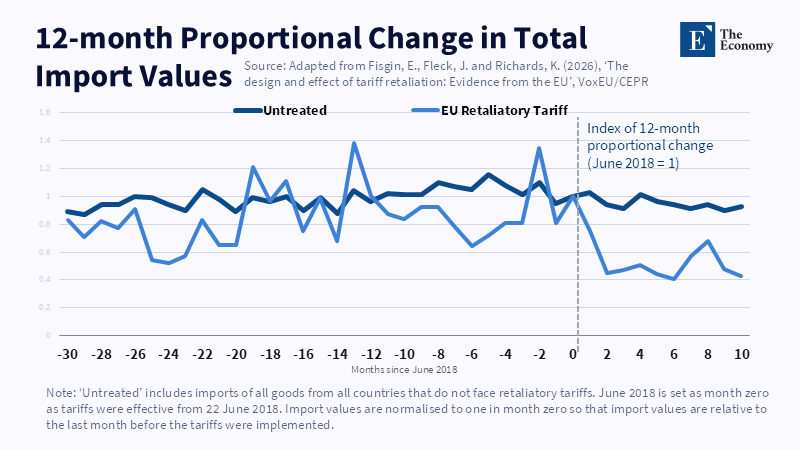

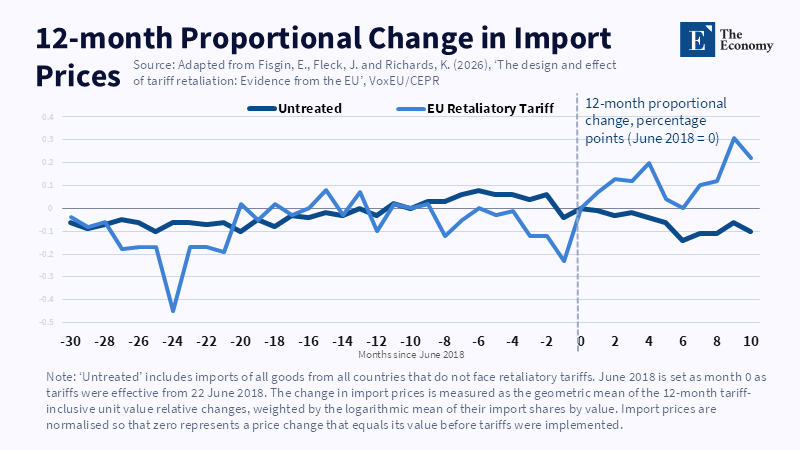

A tariff imposed in June 2018 slashed the value of targeted United States exports to the European Union by 50% within two months. The more significant impact occurred subsequently. Even after the EU suspended its retaliatory tariffs in January 2022, the lost trade had failed to return. Supplier relationships had been reconfigured. Contracts had moved to alternative suppliers. Buyers had realized they could depend on someone else. This track record demonstrates the limits of using a single welfare snapshot of trade measures. A tariff involves more than a transitory price disruption, but also a reshuffling of production, investment, expertise and the availability of competition. Durable tariff policy must thus weigh other things besides the short-term consumer cost; it should price the capabilities, sources of market power and the future bargaining power of governments that vanish when a sector is permitted to contract beyond the threshold of revival.

Long-Term Tariff Policy Begins Where Static Welfare Ends

The familiar test of tariff retaliation is simple: a government finds the goods that are easiest to replace, avoids critical inputs and restores the original trade injury ratio; the EU 2018 response to the US aluminum and steel levies followed this formula. It applied duties of 10 or 25 percent to roughly $3.3 billion worth of US products; most products targeted had a broad basis of supply; only 34 of 180 traded product groups had a high degree of supplier concentration. This design minimized the potential for a large domestic price shock and exploited the EU's open consumer structure to discourage US suppliers from entering in the future without inducing inflation throughout the economy. As a piece of short-run policy engineering, it succeeded. But its own success provides a reminder that the static test is insufficient: trade diversion persisted, even once the tariffs expired. A narrowly designed intervention can still leave a lasting echo.

That's important because comparative advantage is not a fixed feature of an economy. It is contingent on size, research, investment, capital, skills, norms and state support. Losing market share today can mean losing battery investment tomorrow; suppliers lose orders in the intermediate, engineers move, banks increase the cost of capital, the domestic chain gets smaller and the next model gets harder. A lower import price will enable some intermediate consumption today at the cost of a weaker system to produce future income. Static welfare analysis prices today's consumption basket; long-term policy must also price the loss of tomorrow's productive options. Tariff policy must be sensible over this sequence. The question is not just whether consumers can move to another product in-kind terms. It is also whether the economy can go back to domestic or allied production even after a shock, a price hike, or export restriction.

The scale of retaliation changes the problem. Small measures can be targeted at products with many substitutes and of small industrial significance; large measures cannot. When a tariff list spreads to machinery, chemicals, cars, batteries, food and services, with nearly every final product being an input somewhere, the distinction between punishing a foreign producer and taxing one’s own supply chain disappears. Macroeconomic analysis of a ten percentage point tariff hike illustrates why. Unless there is retaliation, the tariff will cut output and boost inflation by raising the costs of intermediate imports. With one-for-one retaliation, the output and consumption declines are larger: at this point, precise compensation leads to a trade war. Tariff policy in the long run must acknowledge a threshold beyond which measured retaliation is no longer possible to design precisely.

Europe's EV Problem Is About Capacity, Not Only Price

The European car market makes this long-term perspective urgent. Electric-car sales topped 17 million globally in 2024 and over 11 million of these were sold in China. Electric models made up almost half of China's market. Europe's market was significantly weaker. EU battery-electric sales declined 5.6 percent (year on year) between 2023 and 2024, while their market share narrowed from 14.6 to 13.6 percent. Chinese-produced electric-car sales in Europe then increased to approximately 940,000 in 2025, over 50 percent above the previous year. While this data does not suggest that European manufacturers are doomed, it does illustrate that the center of scale, learning and supplier growth is shifting rapidly. A policy that views each imported car as one simple consumption bargain simply misses the industrial change underneath its price tag.

In 2025, China supplied nearly 70 percent of electric-car production worldwide, commanded a stake of more than 80 percent in battery-cell manufacturing, roughly 85 percent in cathode material manufacturing and exceeded 90 percent in anode material production. These are not narrow positions of assembly; these are deep manufacturing networks. According to the European Commission, Europe is also entirely dependent on China for its entire supply of heavy rare earth elements. China's 2025 export controls on seven heavy rare earth elements showed how concentrated supply can quickly become industrial leverage. Such manufacturing concentration can generate a type of market power that might not show up in today's retail price. The danger is not China definitively raising the prices of electric vehicles; the danger is that Europe could lose the capacity to respond if prices increase, if exports are limited, or if access becomes conditioned on political demands. Long-term tariff policy should price in that loss of options before it manifests as a crisis.

The employment stakes are high, but they must be stated carefully. According to Eurostat, there were 2.47 million people working in Europe's automotive industry in 2023. Of these, some 851,000 were working for demand outside the Union. A broader OECD figure puts direct and indirect automotive employment nearer to 12.9 million. Additionally, Europe maintained a recorded 89.3 billion trade surplus in the automotive sector in 2024. This is not an industry that has already evaporated. It is an industry with sizeable and powerful resources under severe competitive pressure. The earliest warning of this trend is visible in the direction of travel. After adjusting for inflation, EU car exports to China declined by 22.3% in value (between 2019 and 2024), while the value-added of Chinese cars supported by EU demand has increased dramatically more than tenfold over the last decade. The market is still one of mutual dependency but the preponderance of capability is shifting.

Tariffs cannot undo this alone. The EU's countervailing duties on Chinese battery-electric cars sit on top of the normal import tariff. They may restrain subsidized import growth, but do not make energy cheaper, permits faster, software smarter, charging networks denser, or battery supply chains stronger. They may boost prices and push out the end of dirty motoring if used without support for buyers. That critique is right. The solution is not to accept subsidized concentration, but to bring trade defense in from the cold and link it to a credible industrial transition. Every year of protection should produce measurable gains in cost, capacity and technology. Long-term tariff policy should buy time for change and not reward delay.

Tariff Retaliation Can Protect—or Destroy—Future Options

Tariff retaliation is not about revenge but about preserving policy options. A challenger with multiple suppliers can endure conflict, while a market dominated by one production system cannot. This explains why the 2018 EU design was reasonable in its original framing, focusing on visible goods, avoiding excessive exposure to hard-to-replace inputs and building political momentum. But that project cannot simply be scaled up to encompass the strategic rivalry with China. Europe exports to China cars, machinery, chemicals, luxuries and high-tech equipment; it imports batteries, electronics, raw materials and low-cost consumer goods. Tariff escalation would batter both directions in that supply chain. The blow would not end at the border. It would ripple outwards through factories, shops, finance arrangements and family budgets.

An improved standard for evaluating each measure would involve four related tests, even if no formal score is awarded: one based on the instantaneous price and income effects; one based on how concentrated supply is and how long it takes to find an alternative; one based on its effects on domestic capital formation, skills and innovation; and one based on its risks of coercion or stockpiling of supply. The first of these four tests amounts to what the home country would traditionally regard as welfare analysis. The other three capture time, dependence and resilience. A low-cost imported product may pass the first test, while a tariff increases visible costs today but holds open competition tomorrow. And those two policies can be reversed, with the tariff reducing competition, by raising the price of some crucial home inputs, by making home manufacturing a less viable option, or simply by another unexpected means of increasing the home country's opportunity costs. Those long-term policy errors, of all tariff policies, are the ones to watch out for most.

This discussion also explains the defense that fears of dependence are just a way for weak firms to get help. Unconditional protection can encourage poor management. Europe already faces the costs of inefficient product life cycles, failed software and high expenses that tariffs cannot disguise. Any trade shield should end unless firms agree on responsibilities for investment, prices, technology and production. Public assistance should promote cooperative charging networks, worker training, battery recycling, network upgrades and research platforms that many firms can use. Supporting one firm's past market share is unlikely to be cost-effective. Supporting new production capacity can enhance competition. The goal is not to preserve the existing automobile sector. It is to retain enough capabilities in Europe to produce the next.

The converse objection is that diversification itself is prohibitively expensive. This is also in part correct. The OECD research demonstrates that there is a profound two-way dependence in trade between high-tech and major emerging markets. A complete decoupling would not only wipe out surpluses and choices and damage innovation incentives in the process, but also, at the same time, split climate technology along an arc between rival camps when time for deployment is limited. Hence, long-term tariff policy must reject autarky. There is no need for Europe to produce every single mineral, cell, chip, or vehicle at exactly the same locations. Europe does need at least one additional credible supplier, enough domestic know-how to absorb a shock and trade partners that are not exposed to the same political risk. Autarky is not the answer.

A Long-Term Tariff Policy for an Open but Defensible Market

Europe should follow this with a much broader industrial-capacity program. Countervailing duties should remain tied to clear evidence of subsidy and injury. Reviews should be based on evidence and market outcomes. Access to public procurement should depend on clear standards for emissions, data security, repair, emergency readiness and production in Europe or trusted partner countries. Any rules must be simple, calculable and open to any firm that qualifies. Chinese investment is positive, with assets, employment and costs to the local economy. Large capacity installation should occur on the basis of showing that employment, added value, supplier development, research and skilled workers come in the course of the project and that it cannot operate as a manufacturing base for imports. Ownership matters less than the durable local capacity the investment leaves behind.

Demand policy also plays a role. European producers can't compensate for the lack of scale if households cannot afford to buy and charge electric cars at home. Continuity of purchase incentives for relatively inexpensive models, continuity of infrastructure roll-out, cheaper power and international harmonization of battery design would do far more for competitiveness than tariffs. Future trade policy has to also look at intermediate inputs during the transition. Cars are potentially justified in cases where subsidies skew the playing field. Cells, magnets, or manufacturing equipment are more complicated when there are no European substitutes. A comprehensive tariff that inflates the price of local production can doom the very activity it seeks to preserve. Tariffs should be sequenced over time according to actual supply-side alternatives and systematically announced with the benchmarks for their expiration at each formal review.

The same discipline should apply to retaliation. The EU should constantly have a list of measures ready for buildup or rollback, but the list should be subjected to a screening for hidden supply-chain repercussions. Commerce, procurement and regulatory access may, under certain circumstances, wield greater pressure than duties to physical inputs. Collective action with other markets would also lessen the strain on any single economy. A large enough group could demand fair subsidy practices, transparent licensing and dependable access to strategic materials in exchange for wider market access. This would be more powerful than a stand-alone response since it alters the choice available to the exporting nation. It would also reduce the likelihood that trade is merely relocated from one European nation to another while the initial vulnerability remains.

The lesson from the 2018 tariff episode is not that tariff retaliation is painless. It is that even a small, carefully chosen measure can shape trade for years to come. That lesson should put an end to leaving the assessment of tariffs solely to the price paid the next quarter. Europe must realize the cost of lost factories, lost supply networks, lost engineering skills and lost negotiation leverage before those losses become permanent. It must realize the costs of protection—the higher prices, slower climate action and less extensive export access-before they do. Long-term tariff policy is the exercise of restraint, keeping both risks in view and acting before either becomes unmanageable. The objective is neither to secure a closed market nor to be helplessly dependent. It is an open market that can still say no, can still switch suppliers, can still gain bargaining leverage and can still manufacture what it cannot afford to lose. Europe needs that test before the next round of tariffs, not after the markets have marked the winners.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Arriola, C., Cai, M., Kowalski, P., Miroudot, S. and van Tongeren, F. (2024) ‘Towards demystifying trade dependencies: At what point do trade linkages become a concern?’, OECD Trade Policy Papers, No. 280. Paris: OECD Publishing.

Auray, S., Devereux, M.B. and Eyquem, A. (2025) ‘Tariffs and retaliation: A macroeconomic analysis’, ENSAI, 27 May.

Brennan, A. (2026) ‘“From EVs to Hybrids”: EU raises trade barriers against China, risking retaliation and erosion of industrial competitiveness’, The Economy, 22 June.

Delaney, S. (2026) ‘Chinese EVs unstoppable despite tariffs; EU moves to raise trade barriers further’, The Economy, 18 June.

European Commission (2024) Commission Implementing Regulation (EU) 2024/2754 of 29 October 2024 Imposing a Definitive Countervailing Duty on Imports of New Battery Electric Vehicles Designed for the Transport of Persons Originating in the People’s Republic of China. Brussels: European Commission.

European Commission (2025a) Industrial Action Plan for the European Automotive Sector. COM(2025) 95 final. Brussels: European Commission.

European Commission (2025b) ‘Export restrictions on raw materials and rare earth elements’, Access2Markets Trade Barrier Database. Brussels: European Commission.

Eurostat (2025a) ‘Employment and value added using FIGARO data: View into the automotive industry’, Statistics Explained, 16 July.

Eurostat (2025b) ‘EU car trade surplus: €89.3 billion in 2024’, Eurostat News, 1 April.

Fisgin, E., Fleck, J. and Richards, K. (2026a) The Design and Effect of Tariff Retaliation: Evidence from the European Union. International Finance Discussion Papers, No. 1436. Washington, DC: Board of Governors of the Federal Reserve System.

Fisgin, E., Fleck, J. and Richards, K. (2026b) ‘The design and effect of tariff retaliation: Evidence from the EU’, VoxEU, 17 June.

Grohol, M. and Veeh, C. (2023) Study on the Critical Raw Materials for the EU 2023: Final Report. Luxembourg: Publications Office of the European Union.

International Energy Agency (2025a) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

International Energy Agency (2025b) Global EV Outlook 2025: Expanding Sales in Diverse Markets. Paris: International Energy Agency.

International Energy Agency (2026) Global EV Outlook 2026. Paris: International Energy Agency.

Organisation for Economic Co-operation and Development (2024) The Future of the Automotive Value Chain: Implications for FDI–SME Linkages. Paris: OECD Publishing.

Organisation for Economic Co-operation and Development (2025) OECD Supply Chain Resilience Review: Navigating Risks. Paris: OECD Publishing.

Reuter, M. (2026) ‘Volkswagen’s own board concedes “collapse of the import model”, as Germany risks becoming a contract manufacturing base for Chinese automakers’, The Economy, 19 June.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.