Why China’s Green Energy Strategy Needs Global Competition

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.

Authored On

Modified

China’s clean-energy scale has lowered costs while concentrating industrial power Rare-earth controls show how market dominance can become geopolitical leverage Managed rivalry can preserve low prices without accepting strategic dependence

In 2025, China rolled out 440.1 gigawatts of renewable-generating capacity; a little more than 692 gigawatts was added worldwide. One nation contributed nearly two-thirds of all global growth that year. That is more than a climate statistic. It is also a reflection of industrial might. China's clean energy strategy now encompasses its factories, electrical grids, mineral processing, banking sector, technical standards and export markets at an unprecedented scale of integration. Such a systematized framework could make clean power cheaper and more accessible worldwide, while giving Beijing greater geopolitical leverage over dependent nations. The advisable measure is thus not to block that system or force an expensive global technological split. It is to prevent any nation from exploiting its zero-emission resource dominance into geopolitical pressure. The world needs China's continued push towards renewable expansion and several capable competitors to limit the coercive use of that dominance.

China's Green Energy Strategy Is Becoming Industrial Power

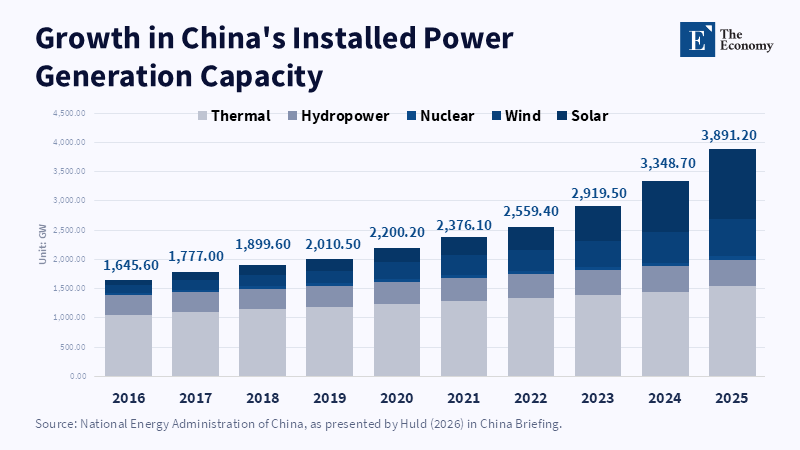

China's edge was not a one-off subsidy or some single breakthrough technology. It emerged from twenty years of consistent policies, a huge domestic market, nimble competition at home, cheap capital and rapid construction. And the next phase would seem set to bring those factors still more into line. China's 15th Five-Year Plan sets a new course for more direct green supply, greater carbon accounting, new storage technologies, cleaner manufacturing processes and some one hundred nationally designated zero-carbon industrial parks. It also seeks to increase the contribution of non-fossil fuels from 21.7 percent in 2025 to 25 percent by 2030 and to extend the world's most extensive network of western-to-eastern power interconnections. This is important because a green energy development pathway based on integrated Chinese production, power, transport and finance will produce synergies that stand-alone sectoral strategies could not match. Factory-scale photovoltaics could cluster near cheap new renewable power supplies, while grid extensions could track industrial demand. Battery storage could both accelerate electric vehicle adoption and provide grid balancing, while common technical standards would significantly reduce transaction costs. This could eliminate waste and turn every new project into a demand for the next. The end result would not merely be a bigger green economy: it would be a nationally integrated manufacturing system driven by lower-carbon energy.

That system already determines prices in world markets. In 2024, China held more than 80 percent of global capacity across the major stages of solar-panel manufacturing; 70 percent of electric cars were produced there (it supplied 40 percent of electric car exports); and it accounts for a large share of the manufacturing capacity for wind turbines, solar panels, batteries and their components. Costs are no less important than output. The International Energy Agency has compared the costs of manufacturing solar cells, wind turbines and batteries. Even before considering explicit state supports or subsidies,the cost of manufacturing these technologies in the United States was estimated to be around 40 percent higher, in the European Union, 45 percent higher and in India, 25 percent higher than in China. These differentials correspond to the advantages of scale, concentration of supply networks, skills, trucking routes, ports and intense domestic competition. One success fuels another and tariffs cannot provide the same effects. An effective response needs to establish complete ecosystems in the areas where they are weakest.

Cheap Green Technology Is a Global Public Good

The strongest argument for a more unified China green energy approach is simplicity: bigger is cheaper. Solar costs have dropped 90 percent since 2010. In 2024, 91 percent of new utility-scale renewable projects delivered electricity more cheaply than new fossil fuel alternatives. China-based firms were not responsible for all parts of that downward curve, but their scale helped accelerate learning, broaden supply chains and drive down equipment prices. That is good for the world, especially in places where capital is scarce and governments’ wallets are often empty. Last year, Africa managed just 11.3 gigawatts of renewable capacity, compared to 440.1 gigawatts in China. Cheap hardware cannot solve weak grids or high financing costs, but it can determine whether a project proceeds at all. If a policy pushes up hardware costs everywhere, it will discourage far more projects, in far more places, than it will help.

The conventional talk of the Chinese "overcapacity" problem is therefore too limited. Surplus supply can undercut margins, force the closure of rival plants and increase buyers’ dependence after rival producers exit. But it can also reduce power, transport and storage costs. Both effects are occurring. The policy goal should not be to keep every single domestic producer alive at any cost. Rather, it should be to keep a competitive market structure. Some import duties in the event of apparent subsidy, dumping, or opaque state guarantees might be right, temporarily, provided consumers are compensated. Blanket tariffs are ineffective: they penalize consumers, delay projects, protect firms that may never become competitive, while doing little to improve resilience. Better policies should award higher scores in public tenders for low emissions, reliable service, respect for labor standards, local sourcing, component recycling and greater supply diversity. They might have kept plants temporarily subsidized if they demonstrated good potential at a reasonable scale. Such policies maintain market structure, rather than "support" one set of players in the absence of a defined contest.

Rare Earths Show Why Scale Needs Limits

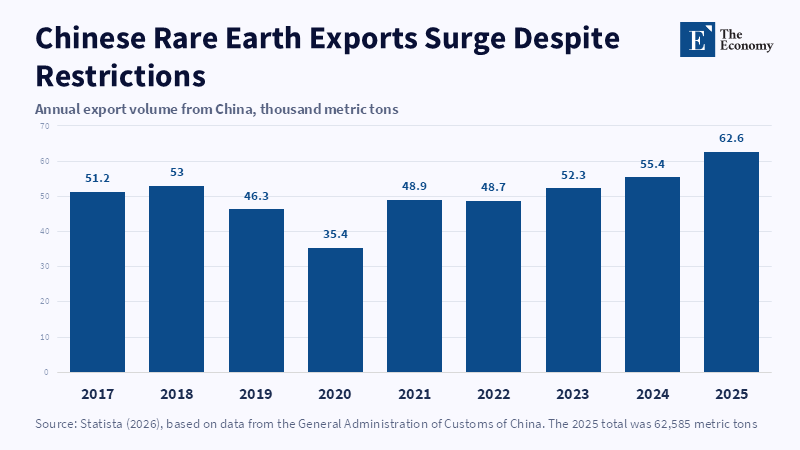

The fear of green dependence is not hypothetical. Critical minerals illustrate how concentrated industry can become a strategic power. China is the dominant refiner of 19 of the 20 energy-related strategic minerals tracked by the International Energy Agency, with an average market share of about 70 percent. In magnet rare earths, China accounts for about 60 percent of mining and more than 90 percent of refining. Its share of permanent magnet production is almost 95 percent. Export controls introduced in 2025 required firms outside China to go for licenses. The physical materials are deep inside cars, electronics, wind turbines and defense systems. The disputed 2010 episode involving Japan may not have been a planned act of economic coercion. That, though, does not eliminate the hazards. Strategic leverage does not require an absolute embargo; delay and uncertainty can be enough. A delayed license can hold up an entire factory.

Nonetheless, clean-energy technology is not quite the same as rare earths. Solar modules and wind turbines are finished products and their factories can be built in more places than rare-earth separation plants. Wind equipment, batteries, inverters and electric vehicles feature different supply chains with varying degrees of concentration. Still, the pattern is the same. Low prices undermine investment in other technologies. Diminishing skills keep re-entry slow. Upstream factories and processed raw materials remain tied to the dominant Chinese supplier. The reliance only appears when there is a crisis. But China, too, has limits. It still depends on imports of a handful of raw materials, needs foreign markets and would lose from a wide-ranging trade break. Interdependence diminishes the probability of truly drastic moves, but not the possibility of selective pressure. China’s green energy strategy should combine industrial scale with credible restraint. Clear export rules, published licensing tests, notice periods, emergency supply routes and reliable dispute mechanisms could make Chinese actions more predictable to the world.

Managed Rivalry Can Protect China's Green Energy Strategy

The answer is managed rivalry, not green decoupling. The EU has already adopted a bold target for 2030. No single third country should supply more than 65 percent of the EU’s annual needs for any strategic raw material at any relevant processing stage. It also seeks 10 percent domestic capacity equal to the needs for extraction, 40 percent for processing and 25 percent for recycling. In June 2026, the G7 went beyond the EU on rare earths and permanent magnets. Its members are committed to reducing dependence on any one outside supplier to below 60 percent by 2030 and to 50 percent "as soon as possible". These targets represent a rapid transition from a vague "worry" about supply chains to a concrete attempt at "diversification". But they are still confined to minerals. The same thinking should also be applied to key clean technologies. Every critical step should be underpinned by two or three suppliers able to grow significantly in a shock. No country needs to produce every component domestically. There is no point in becoming entirely self-sufficient and it is also certainly not feasible.

That sort of redundancy would cost money. Cheaper Chinese output and perhaps under-utilized duplicate capacity in normal years may appear inefficient, but would not necessarily be wasteful. Buffer stocks, spare capacity and alternative sources of supply are forms of supply-chain insurance. The problem is to buy that insurance without creating a subsidy race without discipline. Governments need to take advantage of collective procurement, long-term purchase agreements and price-gap support if the market price falls below the level at which a non-Chinese plant will be viable. Development banks should focus on processing and manufacturing in countries with plenty of resources but limited industrial capacity. Harmonizing standards should promote inter-market trade by alleviating barriers. Recycling regimes should not impose heavy demands on new mines by treating every mineral as equally strategic. Stockpiling should focus first on materials that do not have a quick replacement cycle. Governmental support should stop if firms fail to reduce costs sufficiently, reach targets for output, or compete successfully for private capital.

The same framework must remain open to Chinese companies, under clear guidelines. Local manufacturing, joint ventures, licensing arrangements and technology collaborations are, unlike a barrier, likely to accelerate and expand knowledge faster. Access should be controlled by understandable criteria relating to ownership transparency, data security, work practices, environmental performance and a genuine contribution to local value creation. This would allow China to pursue the global market without every overseas plant being seen as an extension of state control. Moreover, host countries would not be simply rubber-stamping assembly projects. Do not expect to contain China's green competition strategy; do expect to keep it in a marketplace where customers have alternatives. China would, of course, benefit from this discipline. A system perceived as useful but not threatening would face fewer import bans, fewer punitive tariffs and reduced political hostility. Enduring influence rests on creating the impression that engagement in no way equates with submission.

Critics will claim that this is protectionism under another name and poorly designed policies could become exactly that. Local-content rules can raise costs, price floors can protect weak firms and exclusive clubs can shut developing economies out of needed investment. These risks demand tighter safeguards, not inaction. Support should address genuine weaknesses and its costs should be public. Host countries should receive finance, infrastructure, skills and a share of processing value rather than serving only as extraction sites. Trade remedies should require evidence of harm and expire after review. The central test is simple: does the policy create another capable supplier, or does it merely block a cheaper one? Only the former improves resilience.

The 440.1 gigawatts of renewables China added in 2025 is evidence of what is possible at scale. They are a reminder of how isolated the rest of the world has permitted one national economy to become. That lead must be addressed, but not with a barrier. This would raise costs, slow deployment and fracture the technologies that are necessary for a safe climate. A better pathway would be a field of forceful competitors. While building a coherent green production system, China would need to accept some rules-based restrictions on coercive use. The G7, EU, Japan, India and other partners would need to fund enough competing capacity to keep markets open under stress, so that markets remain free. Still,developing nations should gain factories, grids and technical knowledge,not just mines and import bills. Green energy creates shared welfare when scale lowers costs and competition disperses power. That will be more costly than a global diversification at the lowest prices, but much less costly than a rushed reconstruction after a major supply shock. That work must begin now.

The views expressed in this article are those of the author(s) and do not necessarily reflect the official position of The Economy or its affiliates.

References

Donway, W. (2026) ‘China’s Rare Earth “Monopoly” — and Why Markets Will Break It’, The Daily Economy, 14 January.

European Commission (2024) European Critical Raw Materials Act. Brussels: European Commission.

G7 (2026) G7 Leaders’ Declaration on Securing Supply Chains for Critical Minerals. Évian: Group of Seven.

Gaudiaut, T. (2026) ‘Chinese Rare Earth Exports Surge Despite Restrictions’, Statista, 8 April.

Huld, A. (2026) ‘The Path to Peak Emissions: Climate and Environmental Policy in China’s 15th Five-Year Plan’, China Briefing, 23 April.

International Energy Agency (2024) Energy Technology Perspectives 2024. Paris: International Energy Agency.

International Energy Agency (2025a) Global Critical Minerals Outlook 2025. Paris: International Energy Agency.

International Energy Agency (2025b) Global EV Outlook 2025. Paris: International Energy Agency.

International Energy Agency (2025c) ‘With New Export Controls on Critical Minerals, Supply Concentration Risks Become Reality’, International Energy Agency, 23 October.

International Energy Agency (2026) ‘New Projects, Partnerships and Policies Are Needed to Address Supply Chain Risks for Rare Earth Elements’, International Energy Agency, 8 April.

International Renewable Energy Agency (2025) Renewable Power Generation Costs in 2024. Abu Dhabi: International Renewable Energy Agency.

International Renewable Energy Agency (2026) Renewable Capacity Statistics 2026. Abu Dhabi: International Renewable Energy Agency.

Policy Circle Bureau (2026) ‘China’s Green Energy Strategy Is Becoming a Theory of Power’, Policy Circle, 21 March.

Saptakee, S. (2026) ‘Can the G7 Challenge China’s Rare Earth Monopoly with Its 60% Import Rule?’, Carbon Credits, 18 June.

Xue, P. (2026) ‘China’s Climate Toolkit in Search of a Strategy’, East Asia Forum, 15 June.

Working across research, policy, and data-driven analysis, the Editorial Board ensures that published pieces reflect a consistent institutional perspective grounded in quantitative reasoning and long-term structural assessment.